Table Of Contents

What is Volume Variance?

Volume Variance is an assessment tool that checks if there is a difference in actual quantity consumed or sold and its budgeted quantities. It is usually expressed in monetary terms by multiplying the difference between the two with the standard price per unit. The volume variance is considered favorable if the actual number of units consumed is lower than the standard number of units required as raw materials. On the other hand, if the actual number of units consumed is more than the standard number of units, it is considered unfavorable or adverse.

How to Calculate Volume Variance?

It can be calculated by using the following steps:

Step 1: Firstly, determine the actual number of units consumed in material yield variance or the actual number of units sold in case of sales volume variance.

Step 2: Next, determine the budgeted number of units planned for consumption in case of material yield variance or the budgeted number of units planned to be sold in case of sales volume variance.

Step 3: Next, calculate the Variance in the number of units consumed by the actual number of units (step 1) from deducting the budgeted number of units (step 2) for material yield variance. On the other hand, the Variance in the number of units sold by deducting the budgeted number of units (step 2) from the actual number of units (step 1) for sales volume variance.

Step 4: Next, determine the budgeted cost per unit and budgeted price per unit for material yield variance and sales volume variance, respectively.

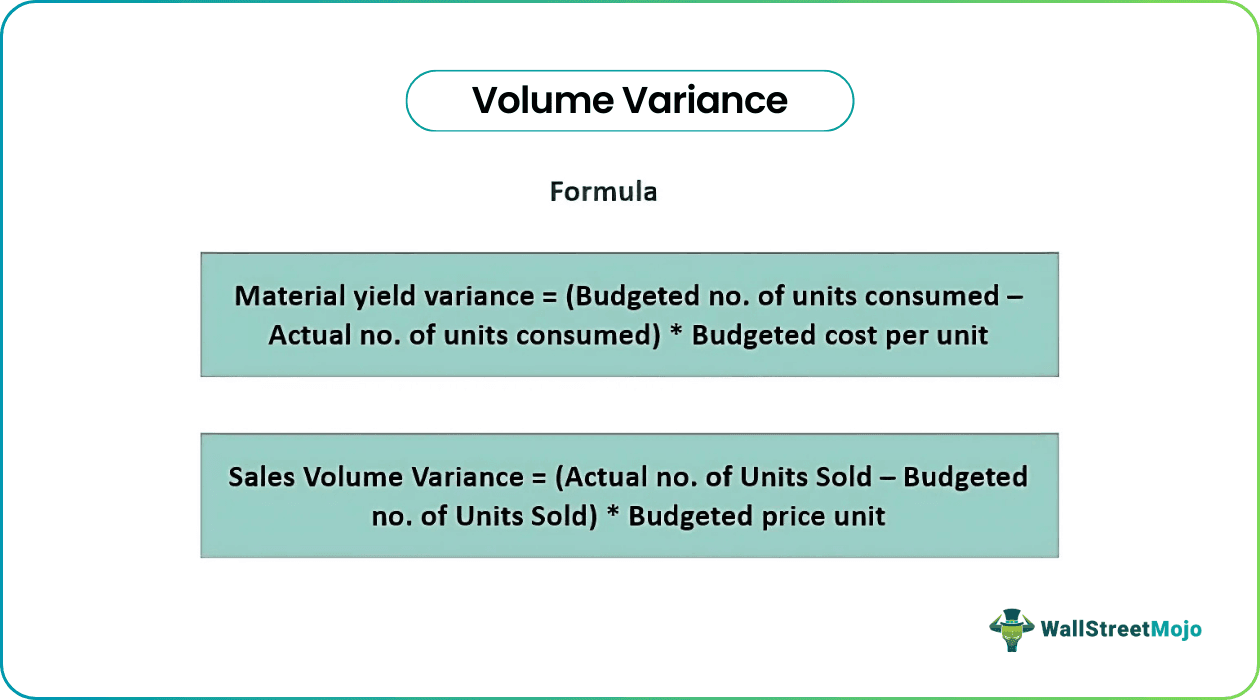

Step 5: Finally, the formula for material yield variance can be calculated by multiplying the Variance in the number of units consumed (step 3) and the budgeted cost per unit (step 4), as shown below,

Material yield variance = (Budgeted no. of units consumed - Actual no. of units consumed) x Budgeted cost per unit.

The formula for sales volume variance can be calculated by multiplying the variance in the number of units sold (step 3) and the budgeted price per unit (step 4) as shown below,

Sales Volume Variance = (Actual no. of Units Sold - Budgeted no. of Units Sold) * Budgeted price per unit.

Examples

Let us understand the examples.

Example #1

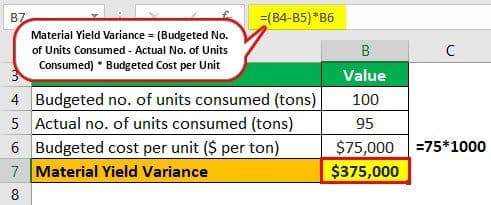

Let us take the example of a manufacturing unit to illustrate the concept of material yield variance. As per the industry benchmark, the unit estimated that it would require 100 tons of limestone at $75 per kg for the previous month. However, the unit used only 95 tons during the month. Therefore, determine the material yield variance in this case.

Given,

- Budgeted no. of units consumed = 100 tons

- Actual no. of units consumed = 95 tons

- Budgeted cost per unit = $75 * 1000 = $75,000 per ton

Therefore, the material yield variance for the previous month can be calculated as,

- = (100 – 95) * $75,000

- = $375,000

Therefore, the material yield variance was $375,000 favorable.

Example #2

Let us take the example of a departmental store to illustrate the concept of sales volume variance. The store estimated that it would be able to sell 4,000,000 bottles of mineral water during the Q2FY19 at an estimated price of $1.10 per bottle. The budget was based on the sales volumes achieved during the last few quarters. However, when the real results of the quarter unfolded, the store realized it would achieve sales of 3,500,000 bottles. Determine the sales volume variance in this case.

Given,

- Budgeted no. of units sold = 4,000,000

- Actual no. of units sold = 3,500,000

- Budgeted price per unit = $1.10

Therefore, the sales volume variance for Q2FY19 can be calculated as,

- = (3,500,000 – 4,000,000) * $1.10

- = -$550,000

When can it Arises?

A volume variance arises only when a business decides the budgeted plan based on theoretical standards, which are practically not achievable due to various operational shortcomings. However, It can be avoided by setting budgeted plans according to attainable standards, wherein all the operational challenges are accounted for with reasonable assumptions.

Advantages

Some of the major advantages are as follows:

- It can set standards for cost, price, and quantity.

- It facilitates management review of operational performance vis-à-vis budget.

- It helps investigate the root cause for variation in the contribution and profitability of a business.