Variable-Rate Mortgage Definition

Variable-rate mortgage refers to a mortgage loan with a variable interest rate. The interest rate positively correlates with the market interest rate or the underlying benchmark interest rate, such as the CIBC prime rate, LIBOR rate, or federal funds rate.

The lender can offer a standard variable rate linked with the underlying index to the customers, and the interest rate fluctuate with the benchmark interest rate (index). The term is common in countries like Canada, whereas in the United States, an adjustable-rate mortgage (ARM) is common.

- A variable-rate mortgage refers to a mortgage with a variable interest rate.

- The mortgage interest rate moves with the market or underlying benchmark interest rate.

- Examples of indexes are CIBC prime rate, LIBOR rate, or federal funds rate. For example, in Canada, the CIBC prime rate is 2.7% as of 8th April 2022, and the mortgage rate keeps pace with the prime rate.

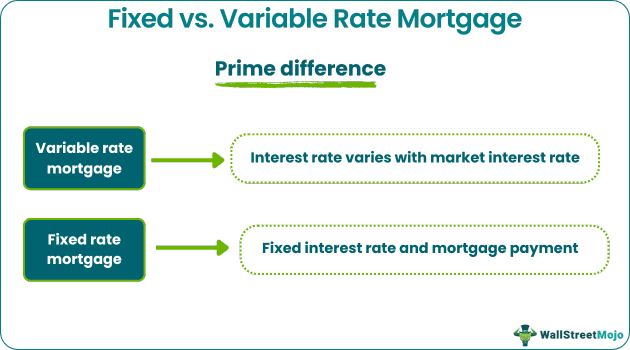

- It is different from the fixed-rate mortgage. For example, the interest rate varies with the market interest rate in a variable regime. In contrast, a fixed-rate mortgage features fixed interest rates and payments.

Variable-Rate Mortgage Explained

Variable-rate mortgages first appeared in the 1930s in the United Kingdom and Canada. The interest due is decided by currently prevailing rates or current market rates rather than the rates in effect at the time of issue. One of the historical events associated with the variable rate regime was the introduction of Floating rate corporate notes in 1974, when a total of $1.3 billion were sold.

It is attractive because if the market interest rate decreases over time, the mortgage interest rate also decreases. As a result, the variable interest rate regime benefits borrowers, so they don’t have to refinance their mortgages when the interest rates plummet. At the same time, the borrower experience loss if the interest rate increases. Furthermore, mortgages offer lower introductory rates than fixed-rate mortgages under the variable regime.

Let’s explain the scenario of variable-rate mortgages in Canada. The variable interest rate moves with the CIBC Prime rate throughout the length of the mortgage. However, the borrower’s monthly payment remains the same generally. Furthermore, when the interest rate on a mortgage fall, more of the monthly payment is allocated to the principle. Conversely, a larger portion of the payment will be devoted to interest if the interest rate rises.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Example

To combat the impacts of growing inflation in the United Kingdom, the Bank of England raised interest rates to 0.25% from the record low of 0.1%. People who have variable-rate mortgages will be affected by the interest rate change. It will impact tracker mortgages that follow a base rate or loans that use a lender’s standard variable rate. A tracker mortgage will track the base rate exactly. So, for example, if the base rate rises, the payment obligation of people with tracker mortgages will almost certainly rise, and the additional cost will completely reflect the base rate rise.

The scenario is different with a standard variable rate — the matching change occurs at the lender’s choice. The majority of banks and building societies will react to increased interest rates. If the lender so decided, they could raise interest rates even further. For example, HSBC’s standard variable rate is 3.54%; if it passes on the entire increase, borrowers will pay 3.69% (3.54% + 0.15%).

Fixed vs. Variable-Rate Mortgage

| Sections | Variable-Rate Mortgage | Fixed-Rate Mortgage |

|---|---|---|

| Interest rate | The interest rate may vary. | The interest rate remains the same for the whole term. |

| Payments | The interest rate is directly proportional to the market interest rate or prime rate. Therefore, changes to interest rates cause changes in the payment structure (principal and interest portion) against the mortgage. | Total payment against the mortgage remains the same, and the borrower is aware of the periodic payment requirements and can budget accordingly. |

| Market rate falls | If the interest rate drops, the periodic payment also reduces. As a result, the borrowers pay less interest and cover up more for the principle. | If the prime interest rate drops, there will be no change to fixed-rate interest, and it becomes more expensive when compared with the market rate. The lenders charge high fees if the borrower opts to sell their home or break the fixed-rate contract. |

| Market rate increases | Suppose if the interest rate increases, the borrower has no choice but to pay more interest on their home loan, and less portion of the installment goes to the principal part. | If the prime interest rate increases, there will be no change to fixed-rate interest, and it seems favorable. |

| Flexibility and stability | The variable rate is unstable. However, it is usually lower than the fixed rate by a small amount. Also, there is a choice for converting to a fixed-rate mortgage. | It reflects stability since the whole payment track is fixed and makes budgeting easier. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What is a variable-rate mortgage in Canada?

In Canada, it varies with the CIBC Prime rate throughout the length of the mortgage. CIBC’s current prime rate is 2.70% as of April 8, 2022. The borrower’s monthly payment remains the same even if the interest rate changes. More portions of the monthly payment will flow to the principle when the interest rate decreases. If the interest rate increases, a larger portion of the payment will account for the interest portion.

What is a 5-year variable-rate mortgage?

It specifies that the amount of time the borrower has committed to a variable interest rate with the lender is a 5-year term. It also points to the duration for which the mortgage contract remains in effect.

What is the variable-mortgage rate in the UK?

It varies in line with the UK economy and the Bank of England’s base interest rate. As of April 8, 2022, the Bank of England base rate is 0.5%.

Recommended Articles

This has been a Guide to Variable-Rate Mortgage. We explain its definition, 5-year variable-rate mortgage, CIBC rate in Canada, and vs. fixed-rate mortgage. You may also have a look at the following articles to learn more –