Table Of Contents

What Is Value At Risk (VaR)?

Value at risk is a statistical metric that forecasts the highest possible loss and the probability of it occurring over a particular period. It is a significant factor in risk management, financial reporting, financial control, etc. It measures the magnitude or potential of losses in a portfolio and is helpful for banks and large corporations to keep an eye on their portfolio value at risk.

It is the measurement of probability of the highest possible value that the portfolio is vulnerable to losing in a given period. It is a metric that is used universally, thereby, is an accepted standard in recommending, buying, or selling assets. Moreover, its applicability is relevant across asset classes such as shares, bonds, currencies, and derivatives.

Table of contents

- Value at risk is a statistical metric used to calculate the tremendous possible loss of an asset or a portfolio in a given period and with a particular confidence level.

- It is calculated to manage risk, aid financial reporting, and financial control.

- Monte Carlo simulation, parametric, and historical methods are widely used to calculate VaR.

- It is relevant across asset classes like bonds, shares, and currencies, which makes it a universally accepted metric while selling, buying, or recommending an asset or investment.

Value At Risk Explained

Value at Risk or VaR is a metric that forecasts the highest amount and possible probability of loss over a specified period, with a given confidence level. Traditionally, for an investor to measure or gauge the risk in an investment, one would look at volatility, the primary concern being the loss of money.

The three factors of VaR cover all these concerns efficiently; the three factors are:

- Time frame

- Confidence level

- Loss amount or percentage of loss.

Despite VaR being a negative figure, it is conventionally considered a positive number as a negative VaR implies that the portfolio stands a greater probability of making profits. For example, the one-day VaR of negative $100,000 would mean that the portfolio would gain greater than $100,000 the next day.

VaR Methods and Formulas

The variance-covariance method, the Monte Carlo simulation, and the historical method are the three methods of calculating VaR. But first, let us understand how to calculate the potential risk through each of the three ways:

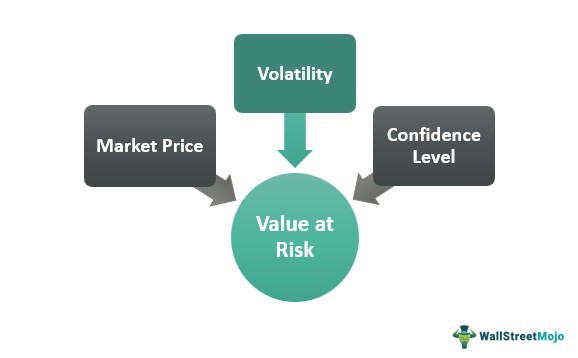

#1 - Variance-Covariance Method

Also known as the parametric method, this method assumes that the returns generated from a given portfolio are distributed normally and can be described by standard deviation and expected returns completely.

The Value at Risk formula:

VaR = Market Price * Volatility

Here, volatility is used to signify a multiple of standard deviation (SD) on a particular confidence level. Therefore, a 95% confidence will show volatility of 1.65 to the standard deviation.

#2 - Monte Carlo Simulation

This method uses a non-linear pricing model, and the quantum of risk is measured by forecasting different future scenarios in this method. This method is best suited in situations where many risk measurement problems are prevalent. It also provides a complete and detailed distribution of the portfolio's losses and gains, which might or might not be symmetrical. However, it is more time-consuming in comparison with other methods of calculation.

Since this method is calculated in a computed manner, it delivers random possibilities through a code. For example, if the monthly return for three scenarios ranged between -20% and 25% and two between -15% and -20%, then the chances of the highest possible loss would be -15%.

Hence, assuming a 95% confidence, the portfolio shall not lose more than 15% in any given month.

#3 - Historical Method

The investor or the analyst provides a start and an end date called, which elicits a variety of scenarios that show the historical value at risk. Here the variable is the security's price with the volatility in the market.

This method computes linear and non-linear possibilities accurately while also displaying the complete picture of the potential profits and losses in the portfolio.

The formula is as follows:

VaR Formula = vm (vi/ V(i-1))

Here,

M signifies the days in the historical data taken into consideration

Vi indicates the number of variables on the day in question (the day i)

Calculation Example

Let us understand the calculation of VaR through the Parametric method:

First, assuming an investor holds only one stock in their portfolio, that of MNO Corporations for $100,000. Then, taking the volatility daily at 1% and a confidence level of 95%.

Using the formula, the calculation for this scenario would be:

VaR = Market Price * Volatility

= $100,000 * .01 * 1.65

= $1,650

The calculation signifies a 5% chance that the maximum amount the investor might lose in one day is $1,650.

Pros And Cons

The statistical metric widely used to understand the risk and the maximum money they are probable to lose is proof that it has some factors that help them better understand their portfolios. However, a few demerits point toward the tool's updating or development prospects.

Let us understand the pros and cons of VaR through the points below:

Pros

#1 - Accessibility

Institutions or investors can understand the overall risk of the investment through a single numerical result, which makes assessing the risk a relatively easy task.

#2 - Standard Usage

It is a widely used tool to measure the risk factors of portfolios. As a result, it can be trusted and compared for cross-verification. Investors can also use it while buying, recommending, or selling an asset, as it is an accepted metric to signify the risks.

#3 - Relevance

The usage of the calculation is relevant across asset classes like bonds, derivatives, currencies, shares, etc. Therefore, large investment firms or financial institutions can gauge the risks of their investments across asset classes and allocate funds according to the VaR report.

#4 - Structured

The report produced a structured methodology to educate the investor or analyst on the risks across investments in an understandable and structured manner, which makes risk management and financial control a relatively more straightforward task.

Cons

#1 - Application

Some methods, like the Monte Carlo Simulation, are expensive and can be challenging to teach in the application. Moreover, the calculation only considers some of the worst possible scenarios. Therefore, organizations conduct stress tests to evaluate situations VaR tends to miss.

#2 - Different Results

The calculation carried out with different methods could show different results. Hence, the accuracy of such analysis is always under speculation.

#3 - Security

The fact that this calculation provides a probability of an event occurring in the future is a possibility of that event happening or not. The chance fills investors with a false sense of security and might turn out to be the other way around.

#4 - Portfolio Calculations

When calculating the risk of an extensive portfolio, each asset class has to be calculated separately. The more significant asset classes in the portfolio, the greater the difficulty of calculating VaR. The correlation between assets also has to be considered along with the risk-return equation.

Value At Risk vs Expected Shortfall

VaR and expected shortfall measure the risks of an investment or a portfolio. However, there are differences in the fundamentals and their interpretations. Let us understand them better through the points below:

VaR

- Value at Risk is a statistical metric to compute a portfolio's risk. It displays the highest possible loss and a given confidence level.

- It considers the market price and the volatility in a given time frame.

- Investors, analysts, and regulators widely use VaR to measure the risks in their portfolios.

Expected Shortfall (ES)

- Expected shortfall answers the value of losses that might occur in the event of a portfolio or a particular asset’s price drop.

- It is calculated based on the totality of returns by averaging the distributions worse than the VaR of a portfolio at a specific time, along with a particular confidence level.

- ES has various advantages over VaR because a number of institutions use it as an internal tool to measure or quantify risk.

Difference Between Value At Risk And Stress Testing

The risk element in the financial industry is a primary by-product that comes with almost every action in daily transactions. However, a standard methodology must be used to test or assess the risk element in such transactions.

VaR and stress testing are widely used in such cases; the stark differences between the two are as discussed below:

| Basis | Value at Risk | Stress Testing |

| Function | VaR assesses the maximum potential loss of an asset or a portfolio in a given time frame with a certain confidence level. | Stress testing analyses the impact of adverse situations that place a threat to the soundness of a portfolio. |

| Methods | Monte Carlo Simulation, Parametric method, Historical method. | Historical scenarios, stylized scenarios, and hypotheticals. |

| Analysis | Uses a statistical approach to analyze scenarios. | Uses a non-statistical approach to analyze scenarios. |

| Range | Calculates the loss range within the volatility and confidence level. | Calculates the scenarios that are usually missed by a VaR calculation. |

Frequently Asked Questions (FAQs)

The interpretation of the numbers that value at risk measures can be a metric that signifies the maximum possibility of a loss in a given period or as a measure of confidence where the investor has a sense of security that they will not lose over a certain amount in the given time.

First, to calculate a portfolio value at risk, one must calculate the periodic returns across asset classes and the mean and standard deviation. Then, post this, they can use any of the three methods of calculations to derive the figure that signifies the risks involved. Understanding the correlation between different assets and the risk-return equation is crucial.

Conditional value at risk or CVaR is an extended measure of risk that computes the average losses of scenarios beyond the confidence levels in a specified period.

The marginal value at risk or MVaR determines the additional risk in the portfolio arising due to the addition of a new asset. This calculation helps investors and portfolio managers understand the portfolio changes and helps diversify to manage the risks.

Recommended Articles

This article has been a guide to what is Value at Risk (VaR) and its meaning. We explain its methods, formula, calculation, example, and comparison with the expected shortfall. You may also find some useful articles here -