Table Of Contents

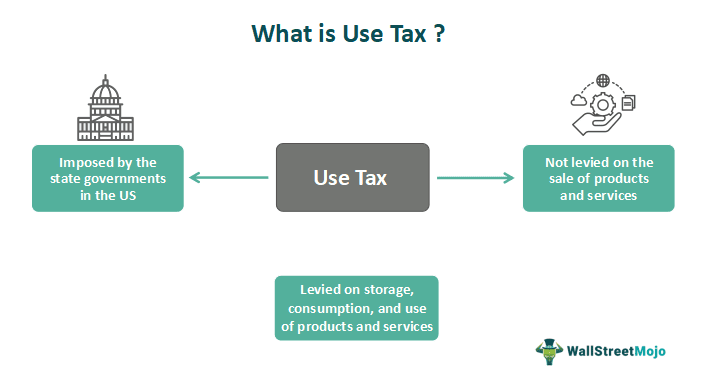

What Is Use Tax?

Use tax is typically a type of sales tax levied in the United States of America by various state governments on products or services not when they are sold, but for their storage, use, consumption etc.

The use tax is compensatory and complementary to the sales tax. It is charged where the sales tax is not charged on a particular product. Thus, the person needs to be clear on what tax is charged. E.g., when products are purchased online, no sales tax is charged by the seller; hence this tax is charged.

Use Tax Explained

Use tax is a kind of sales tax having various similar characteristics as that of sales tax. However, it is not exactly similar to it. Sales tax is levied when the goods or services are sold to the end customer. Use tax is typically imposed on the taxable goods or services bought for use, enjoyment, consumption, or storage mainly from outside that person's tax jurisdiction. So, the authorities or states do not levy such taxes on which sales tax is already applicable to avoid double taxation or cascading effect of tax on the item.

Typically, use tax for businesses apply to purchasers. The former is the tax charged on the purchaser and is self-assessed by him and paid to the respective state government while the latter is the tax charged on the sales made by the vendor to the buyer outside the state of the vendor, i.e., interstate sales.

Rules

Use tax is charged to the purchaser. In the case of the consumer use tax, at the time of purchase of goods or services, the purchaser is required to calculate it, and such tax is then self-assessed by the merchant itself as per the specified norms of the state government. In this case, the merchant itself pays the self-assessed tax to the respective state government.

However, in the case of a retailer or vendor, the tax charged is on sales made by a vendor to a buyer outside the vendor’s state, i.e., interstate. Sales Tax is paid to the Government if the vendor or retailer is registered in the state of delivery.

How to Calculate?

It is charged based on a certain percentage of goods purchased by the merchant.

The rate of such tax is the same as the rate charged on sales tax. Moreover, the rate of use and sales taxes differs from state to state. The specific percentage of tax is charged on various purchases and expenses incurred by the merchant, for example, the purchase of office equipment, materials goods, and services, etc. based upon the specific state law, which may be changed by various amendments in state law.

The rate is charged on the total amount of purchase, and such amount obtained is deducted from the full purchase amount. The remaining amount is charged as an expense in the merchant’s books of accounts while the use tax is remitted to the Government on predefined due dates.

Example

Let’s take the example of a US-based company to understand the use tax definition better:

Let us assume that a company P Q R incorporation purchases individual plants of 50 thousand dollars from the state outside the company’s tax jurisdiction. If the seller doesn’t collect and pays the sales tax, use tax is charged.

Suppose tax is charged @ 10 %, hence the total use tax will be $ 5 ($50 * 10%). Thus the purchaser company pays $5 to the Government, and the remaining $45 is booked as an expense in the books of P Q R inc.

Use Tax Vs Sales Tax

The basic points of differences are as below:

- Sales tax, as the name suggests, is levied on sales, transfer, barter, exchange, etc. of goods and services covered under the sales tax. Hence, the end-user or consumer of products or services bears the tax and is paid by the merchant of goods to the state government of the US. Whereas, use tax is levied on certain goods and services when those are bought by the merchant itself for various reasons. E.g., like use, enjoyment, consumption, or storage, mainly from outside of tax jurisdiction where the sales tax is not levied.

- There are types; the customer uses tax and the retailer or vendor use tax. In the case of customers, these taxes are firstly self-assessed by the purchaser, and where the sales tax is not deducted. While in the case of the vendor, the tax deduction is by the vendor. Hence, one can say that the tax is a compensatory or complementary tax where the sales tax is not charged.

- In sales tax, the burden of tax is on the customer as it is charged to the customer, but the seller collects the same. However, in the case of use tax, the primary buyer is liable to assess and pay taxes to the Government of a particular state.

- In short, sales tax is the responsibility of the seller, while the use tax is the responsibility of the buyer.