Table Of Contents

What Is Unitranche Debt?

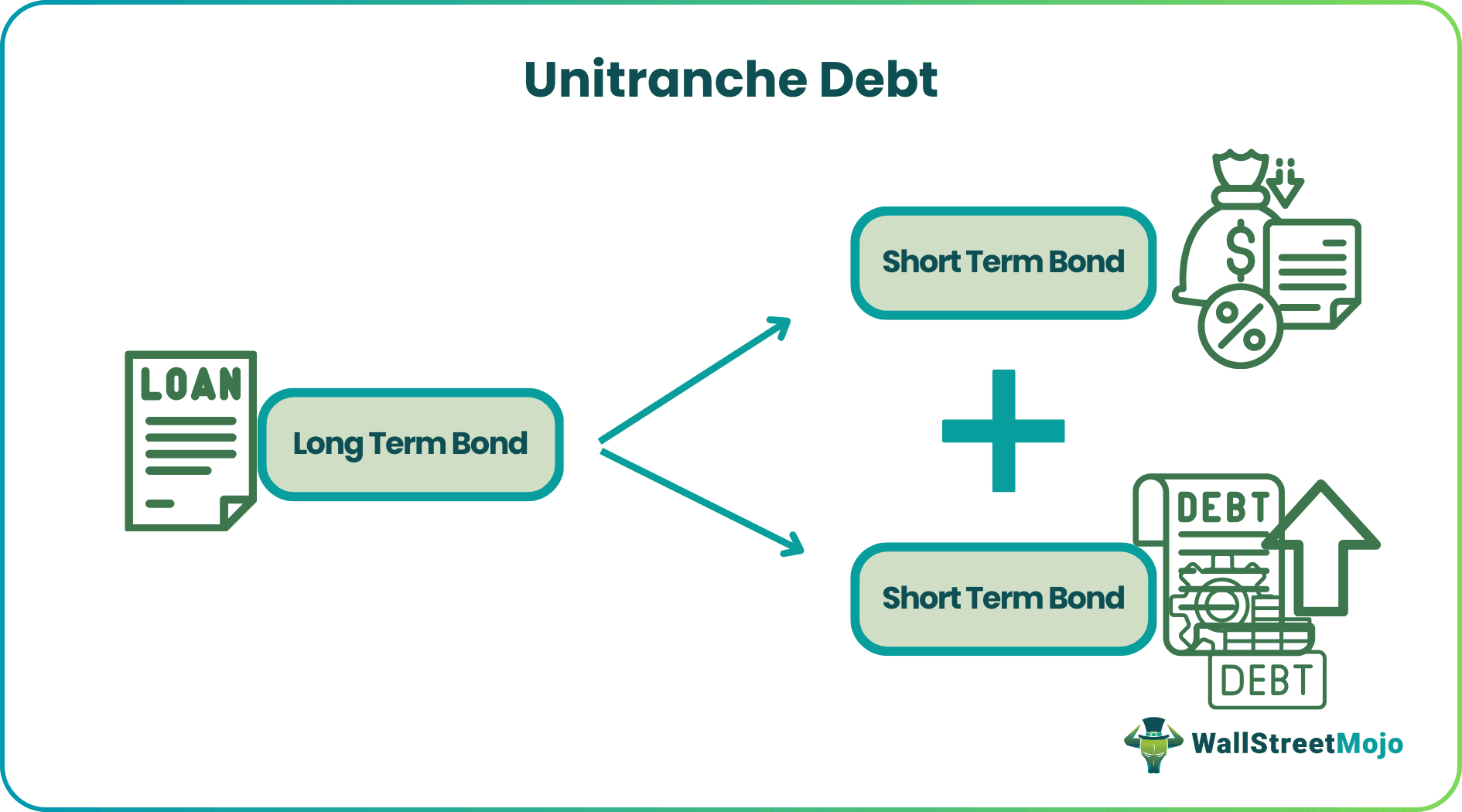

Unitranche debt is a type of financing that combines senior and subordinated debt into a single loan provided by a single lender or a group of lenders. It is a hybrid of traditional senior and subordinated debt, offering borrowers the benefits of both types of financing in a simplified and streamlined manner.

These loans simplify the loan administration process for borrowers. They only need to deal with one lender rather than multiple lenders with different terms and conditions. It can be more cost-effective for borrowers compared to traditional senior and subordinated debt. Since there is only one lender, borrowers can save on legal and administrative fees.

Key Takeaways

- Unitranche debt is a loan structure that blends senior and structured debt into a single instrument. It comprises both regular and riskier loans.

- Unitranche debt is often used by middle-market companies for financing acquisitions, refinancing debt, or funding growth initiatives.

- Senior debt is the most secure and lowest-cost type of debt financing, mezzanine debt provides more flexibility.

- Still, it has higher costs and more risk, and unitranche debt is a hybrid that combines the best features of both senior and mezzanine debt.

Unitranche Debt Explained

Unitranche debt is a type of financing that combines senior and subordinated debt into a single loan with a blended interest rate. The term "unitranche" is a combination of the words "unitary" and "tranche," reflecting the fact that the loan has a single set of terms and conditions.

The concept of unitranche debt originated in the United States in the mid-2000s, as private equity firms and other investors sought new ways to finance leveraged buyouts and other types of corporate transactions. Traditional leveraged finance structures, which typically involved multiple layers of senior and subordinated debt, were seen as complex and time-consuming to negotiate and document.

It was initially popularized by specialized debt funds, such as Golub Capital and Monroe Capital, which focused on providing flexible and streamlined financing solutions to middle-market companies. These funds typically used a "club deal" model, in which several investors would pool their capital to provide a larger loan facility.

Non-traditional lending entities such as debt funds, specialty finance companies, and other institutional lenders are the main providers of unitranche debt. These lenders typically focus on providing financing solutions for middle-market companies, which are typically defined as companies with annual revenues between $10 million and $1 billion.

These lenders are often more flexible than traditional banks and can offer customized loan structures to meet the specific needs of borrowers. They may also be able to move more quickly than traditional lenders and provide financing on a shorter timeline. This can be particularly important for borrowers who need to complete a transaction quickly, such as a leveraged buyout or a recapitalization.

In recent years, larger financial institutions such as banks and insurance companies have also started to offer unitranche debt as part of their product offerings.

Examples

Let us look at the examples of unitranche debt to understand the concept better :

Example #1

Suppose ABC Company is a middle-market manufacturing company that is looking to finance a strategic acquisition. The company needs to borrow $50 million to fund the acquisition and is considering different financing options.

After reviewing several proposals, ABC Company decided to pursue a unitranche debt facility provided by a non-traditional lender. The lender offers a single loan with a blended interest rate that combines senior and subordinated debt.

The loan has a term of five years and an interest rate of 8% and the lender requires a first lien on all of ABC Company's assets as security for the loan.

The loan also includes a series of financial covenants that ABC Company must maintain, including a minimum EBITDA requirement and a maximum leverage ratio.

The lender syndicates the loan with several other investors, and each investor receives a pro-rata share of the interest and principal payments. The loan is structured as a "bullet" repayment, meaning that ABC Company will pay back the entire principal amount at the end of the five-year term.

Overall, the unitranche debt facility provides ABC Company with a streamlined and flexible financing solution that allows them to fund its acquisition quickly and efficiently.

Example #2

In the US and Europe, middle market sponsors are increasingly seeking larger unitranche loans as this structure becomes more popular. Traditionally used for smaller deals, unitranche loans are gaining wider appeal due to challenging conditions for second-lien loans in the US and increased competition in Europe. GSO Capital Partners achieved a remarkable feat by completing a unitranche financing of an impressive €625m, marking the largest-ever such loan in Europe. In the US, middle market lenders are witnessing several unitranche loans ranging from $200m to $300m, and there are indications of a unitranche loan of approximately $400m in the pipeline.

The substantial €625 million unitranche loan supported the merger between Polynt, an Italian chemicals company owned by Investindustrial, and its American counterpart Reichhold. A source familiar with the transaction revealed that GSO's senior debt fund contributed around €300m-€400m, with the remaining funds sourced from limited partners and co-investors. The significant size of this unitranche loan, which was provided in both dollars and euros, demonstrates that larger direct lenders possess the capacity to operate at the higher end of the market.

Advantages And Disadvantages

The advantages and disadvantages of unitranche debt are as follows:

Advantages

- It is a single debt facility that combines senior and subordinated debt into one, which simplifies the borrowing process and eliminates the need for multiple lenders and agreements.

- It can be less expensive than traditional financing solutions because it often involves only one lender, which reduces transaction costs.

- This debt can be obtained more quickly than traditional financing solutions because it often involves only one lender, which reduces the time needed to negotiate and finalize the agreement.

Disadvantages

- Unitranche debt is typically provided by one lender or a group of lenders. Borrowers may have limited options for lenders and may not be able to negotiate favorable terms.

- The unitranche debt market is not as standardized as the traditional financing market, which can make it more difficult to compare terms and conditions across lenders.

- It is typically provided by one lender or a group of lenders. Borrowers may have limited options for lenders and may not be able to negotiate favorable terms.

Unitranche Debt Vs Mezzanine Debt Vs Senior Debt

The differences between unitranche debt, mezzanine debt, and senior debt are as follows:

| Basis | Unitranche debt | Mezzanine debt | Senior Debt |

|---|---|---|---|

| Meaning | Unitranche debt is a hybrid of senior and mezzanine debt that combines both types of financing into a single facility. | It is a type of financing that is subordinated to senior debt but ranks above equity in terms of repayment priority. | It is a type of financing that has the highest priority in terms of repayment in the event of bankruptcy or default |

| Service provider | This debt is typically provided by a single lender or a group of lenders and has a single interest rate and maturity date. | It is often used to finance leveraged buyouts or other high-growth opportunities. | It is usually provided by banks or institutional investors and is considered to be the least risky type of debt financing. |

| Risk tolerance | Unitranche debt is a hybrid that combines the best features of both senior and mezzanine debt. | It provides more flexibility but has higher costs and more risk. | It is the most secure and lowest cost type of debt financing, mezzanine debt |