Table of Contents

What Are Trade Payables?

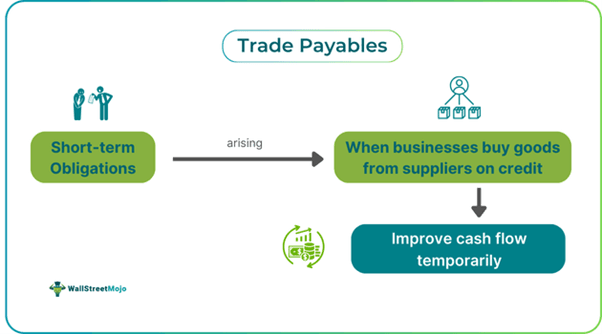

Trade payables or trade accounts payable refer to the money organizations owe other businesses for purchasing products and services on credit. By incurring these short-term liabilities, organizations can make purchases from suppliers without having cash on hand and thus improve their cash flow for a short period.

Accountants can record these expenses on the company’s balance sheet as non-current or current liabilities. The classification depends on the time of debt repayment. When using the cash basis accounting, businesses record a certain part of the short-term expenses that became due at the time of purchase. That said, under accrual accounting, businesses record these expenses at the full value.

Key Takeaways

- Trade payables meaning refers to short-term liabilities that arise when a firm buys goods related to its inventory from suppliers on credit.

- Recording these liabilities is necessary for organizations to figure out the cost incurred to do business.

- There are some key benefits of incurring these short-term liabilities.

- For example, it improves the cash flow position temporarily and improves financial reporting and planning.

- A key difference between trade receivables and trade payables is that the former comes under current assets while the latter is a part of current liabilities.

- Unlike accounts payables, trade payables do not include all short-term obligations.

Trade Payables Explained

Trade payables meaning refers to the liabilities that arise when a business buys goods and services from their vendors or suppliers on credit. If businesses do not incur these short-term expenses, they cannot buy goods for their inventory without cash on hand or cash reserves. Moreover, recording these expenses properly is crucial for businesses to know the bottom line and estimate the profit margin. One must also remember that accounting for such liabilities enables firms to determine the cost incurred to do business.

The terms of repaying the money owed to suppliers can be unique for each supplier. There is no specific rule concerning the repayment period. For example, a company may need to pay within 15 days, 30 days, or even 90 days. Some vendors may offer a custom payment schedule, allowing one to make payments at regular intervals for a predefined period that does not exceed 1 year.

The expenses owed for over a year are long-term liabilities, and thus, one cannot record them as trade accounts payable.

Examples

Let us look at a few trade payables examples to understand the concept better.

Example #1

Suppose ABC Company is an online t-shirt seller, which does the printing itself but purchases the t-shirts from its suppliers. Previously, the firm used to buy all goods in cash. As a result, it had limited funds to invest in other areas of the business. So, it approached one of its vendors, which has been supplying goods for over 3 years and asked for credit. The supplier agreed and allowed ABC to purchase goods on credit. So, from then on, whenever ABC made a purchase from the supplier, it incurred trade payables.

Per terms of the credit, ABC had to pay for the goods purchased within 60 days. Thus, ABC could maintain a better cash flow position as it did not need cash on hand to make the purchase. This, in turn, allowed it to put money into other areas of the business to make improvements.

Example #2

Vodafone India (Vi) is burdened with roughly Rs. 20,000 crore worth of overall payables. The amount includes trade payables encompassing $13,731 crore which reflect Vi’s dues to its vendors, for example, tower firms and gear suppliers.

In June 2024, the telecom company announced that it planned to raise funds worth Rs. 2,458 core via preferential share issuance to Ericsson and Nokia. The objective of this offering of additional shares is to clear a part of the company’s dues.

The company proposes to utilize the Rs. 24,000 crore worth of equity capital it raised in April to roll out 5G networks and expand its 4G coverage. Since the telecom company’s capital raise is designated for new capital expenditure, per JP Morgan, one would not want to rule out further dilution and equity swaps in the future for clearing operational dues.

Benefits

Let us look at some of the key benefits of trade payables in accounting.

#1 - Improves Liquidity And Cash Flow

There’s an inverse relationship between cash flow and trade accounts payable — if the latter increases, the former decreases. This means by incurring the short-term expenses, businesses can improve their cash flow temporarily. As companies pay the short-term liabilities down, their cash decreases. As a result, they are able to spend less in other areas of the business. Since businesses can make purchases from vendors without cash on hand, they can avoid raising additional funds or seeking financial assistance from a bank.

#2 - Streamlines Vendor Relationships

Monitoring the money owed to suppliers efficiently can help businesses streamline their relationship with them. If a company has an organized system, it can easily find out what amount of money it must pay the supplier against the purchases made. This, in turn, helps in making payments on time and maintaining a positive reputation. If businesses have an impressive reputation, they can get more favorable credit terms from existing suppliers and increase the chances of getting credit from other vendors

#3 - Enhances Financial Reporting and Planning

Closely tracking the trade accounts payable helps in estimating when specific bills might become payable. This, in turn, enables them to plan ahead for them and repay the amount owed on time.

Tracking these expenses also helps in the preparation of the balance sheet. This is because the financial statement consists of a breakdown of both current liabilities and current assets. Without proper categorization, businesses will fail to provide the company’s detailed financial overview via the balance sheet.

Risks

Let us look at some of the risks associated with trade payables.

- Failing to meet these short-term obligations can lead to strained relationships with suppliers. Moreover, businesses may have to pay interest or additional charges for making late payments, which cut into their porfits.

- Disreputable vendors can charge for stock that they never delivered. Also, fraud is a noteworthy risk for even large organizations. Vendors willing to sell goods on credit may have an ulterior motive. Hence, companies must proceed with caution when making purchases. Some common invoice fraud attempts may include duplication of invoices, inflated bill amounts, and non-delivery.

Trade Payables vs. Trade Receivables

The key differences between trade payables and trade receivables are as follows:

- Trade accounts payable is the amount businesses owe their vendors or suppliers for products or services bought on credit. On the other hand, trade receivables denote the money customers owe a company for the products or services sold by the latter on credit.

- Businesses need to record trade accounts payable as current liabilities on the balance sheet. On the contrary, companies must record trade receivables as current assets on the balance sheet.

Trade Payables vs. Accounts Payables

Individuals new to the world of finance often think that accounts and trade payables are the same thing. However, they are different in terms of meaning and treatment in accounting. Let us look at their differences in the table below to avoid confusion.

| Trade Payables | Accounts Payables |

|---|---|

| These expenses refer to the money owed to businesses for the purchase of inventory-related goods. | Accounts payables include all types of short-term liabilities or obligations of an organization. |

| Alterations in these expenses influence a business's supply chain. | Changes in these liabilities influence a company’s operational expenses. |

| An increase or decrease in these expenses over a period can help individuals evaluate a business’s financial health. | The increase or decrease in these liabilities over a period can help companies carry out an analysis of their supply chain functions. |

Trade Payables vs. Non-Trade Payables

Let us look at the key differences between trade and non-trade payables.

- Non-trade payables refer to those costs that have no direct effect on a business’s daily operations. Trade accounts payables directly impact organizations’ daily operations.

- Generally, businesses enter trade accounts payables in their accounting system via a module that generates accounting entries automatically. That said, organizations typically enter non-trade payables into their system utilizing a journal entry.