Table Of Contents

What Are Total Assets?

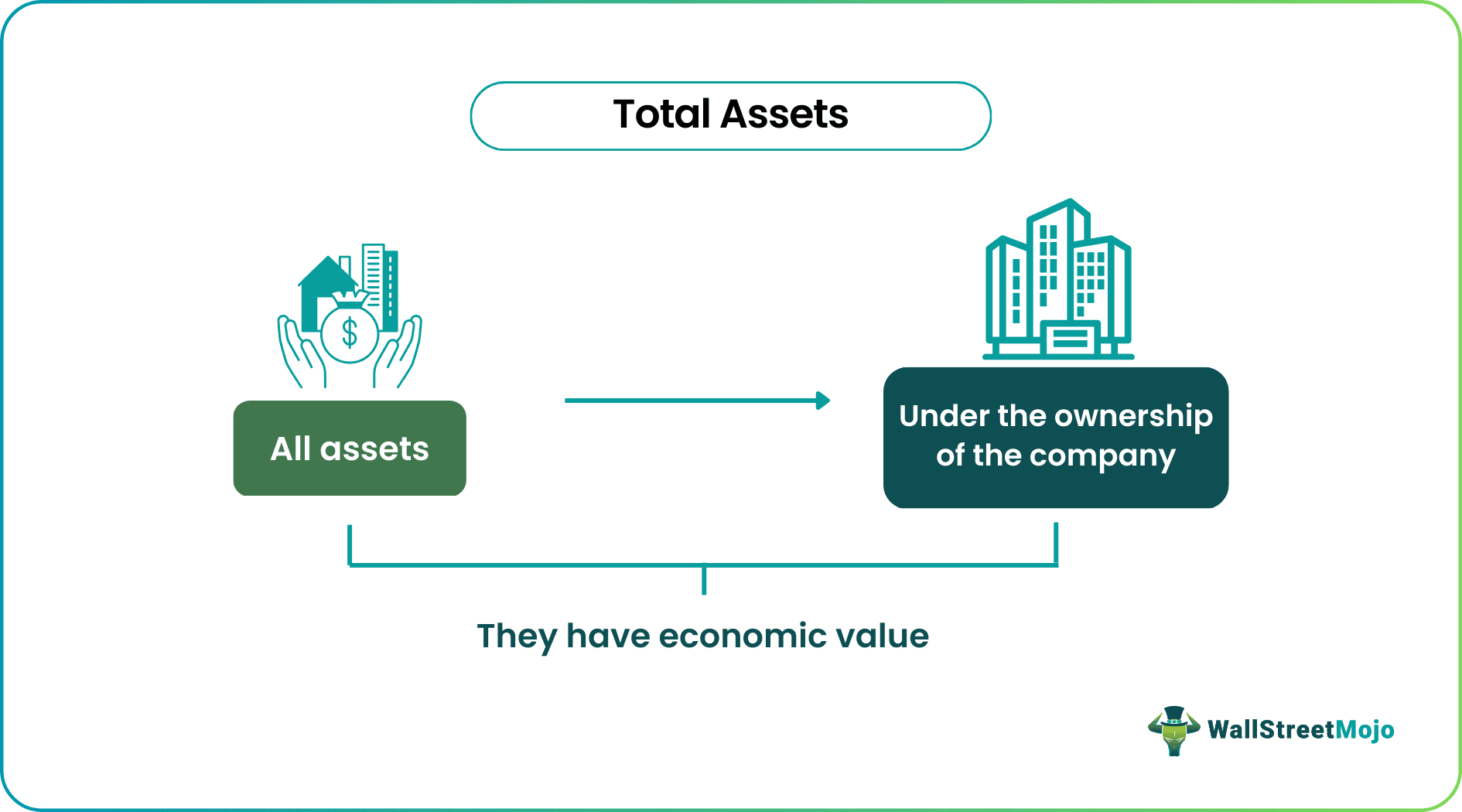

Total Assets, most commonly used in the context of a corporation, are defined as the assets owned by the entity that has an economic value whose benefits can be derived in the future. Assets are recorded in the balance sheet of the firm.

Asset plays a significant role in the extensive study of the financial world. Individuals or Entities should hold more Assets and fewer liabilities to improve their market value and sustainability for the future. To get more projects in the future, the company should look healthy, and a firm's health will be decided on various parameters, among which "Asset" is the most crucial one, as it will help in predicting the range of profit a firm can earn on their current investment over the period.

Total Assets Explained

The concept of total asset falls under the category of financial statement and reporting. It is the value of all the resources that the company owns. They are clearly recorded in the financial statements so that the stakeholders of the company gets an idea about the actual value of assets in possession of the business.

Assets are classified into liquid assets illiquid assets, depending on their liquidity. A liquid asset is that asset that can be easily converted into cash or readily sold for cash; otherwise, it is called an Illiquid asset.

Assets are also classified on the balance sheet as either current assets or long-term assets. A current asset is an asset that can be liquidated within a year, whereas long-term assets are those assets that are liquidated in more than a year.

When we calculate total assets, the value show what is the asset position or how much resource it has to handle its financial obligation, or invest in new or existing projects for the purpose of growth and expansion. It is an important metric that helps investors, analysts and management to evaluate the financial health of the business and make investment decisions.

Types

Here is the list of total asset types

- Cash & cash equivalents

- Marketable securities

- Account Receivables

- Prepaid Expenses

- Inventory

- Fixed Assets

- Intangible Assets

- Goodwill

- Various other assets

Thus, the above total assets equation show the different categories of assets that come under the head of total assets in the balance sheet. All of them together contribute of generation of an economic benefit that will have a positive effect on the company and help it is meeting the various current and non-current financial obligations. These assets help the business to maintain liquidity and solvency and ensure its sustainance.

Formula

Basic Formula in accounting is expressed as:-

Total Assets = Liabilities + Owner's Equity

The equation must balance because everything the firm owns must be purchased from debt (liabilities) and capital (Owner or stockholders equity).

The expanded accounting equation, after considering sales revenue and expenses, is expressed as:-

Assets = Liabilities + Owner's Equity + (Revenue - Expenses) - Draws

In the above total assets equation, we add all the components to get the value of total assets. The liabilities are the financial obligations that the business should meet in its day to to operations, like payment to suppliers and creditors, payment of salary and wage to employees, interest payment on loans, annual dividend payout, etc. Then comes owner’s equity which is part of the total asset that the owners of the business have contributed on their own.

Then come the net revenue or the net expense which is calculated by deducting the total expense from total revenue. If it is positive, then the company’s is in a good financial condition having good free cash flow. Finally, the drawings made by any owners of the business from their equity is deducted to arrive at the figure of total value of assets.

Examples

The following are examples of total assets on balance sheet.

Example #1

If a business owns a piece of real estate where the owner's equity is worth $250,000, and they owe $180,000 on a loan for that real estate, what is the value of Assets?

Solution -

Given,

- Liabilities=$180,000

- Owner’s Equity=$250,000

Therefore, the calculation of total assets will be

Example #2

The summaries of the balance sheet and income statement data follow.

- Beginning of the Year - assets $ 85,000, Total liabilities $62,000, Total owner's equity?

- End of Year - assets $110,000, Total owner's equity $60,000, Total liabilities?

- Changes during the year in the owner's equity - Investments by owner? Drawings $18,000,Total revenues $175,000, Total expenses $140,000.

Solution

1) Beginning of Year

Therefore, the calculation of total owner's equity using below formula is

- = $85,000-$62,000

- Total Owner's Equity=$23,000

2) End of Year

Therefore, the calculation of total liabilities using the below formula is

- Total Liabilities=$110,000-$60,000

- Total Liabilities=$50,000

3) Changes during the Year in Owner's Equity

Opening Balance $23,000, Investments by owner?, Drawings -$18,000,Total revenues +$175,000, Total expenses -$140,000, Closing Balance $60,000.

Therefore, the calculation of owner's investment using below formula is

Closing Balance = Opening Balance + Owner’s Investments - Drawings + Revenues - Expenses

- $60,000=$23,000+ Owner’s Investments-$18,000+$175,000-$140,000

- =$60,000-$23,000+$18,000-$175,000+$140,000

- Owner’s Investments=$20,000

Example #3

A co. The owner's equity is 1/3 of its total assets. Its liabilities are $200,000.What are the total assets?

Given,

- Liabilities=$200,000

- Owner’s Equity = 1/3*Assets=1/3 *A

- Total Assets Formula = Owner’s Equity+ Liabilities

Solution

- A= 1/3 *A+$200,000

- A- 1/3*A = $200,000

- 2/3*A = $200,000

- A= $100,000*3

- A = $300,000

Example #4

Preparing a Balance Sheet

Advantages

Now, let us have a look at some of its advantages of total assets on balance sheet.

- It can be used at any time to repay liabilities.

- On the one hand, Current Assets can be easily converted for liquid cash whereas, on the other hand, Long Term Assets can be used as a mortgage to support working capital.

- Assets help in improving the valuation of the firm. More Assets and fewer liabilities mean a more valuable firm.

- Accounts Receivables are another important part of Assets, which helps build good relationships with various clients, allowing clients to purchase on credit and pay later.

- Various business deals like Mergers and Acquisitions, Tie-ups, etc. assets play a vital role, as every decision is taken by considering the firm’s assets.

- Leasing or renting assets such as machinery or office equipment can save you the initial costs of buying them outright.

Disadvantages

Now, let us have a look at some its disadvantages of value of total assets.

- Depreciation of Fixed Assets over the years.

- One can’t claim capital allowances on a leased asset if the lease period is less than five years.

- In the case of non-repayment of liabilities, the bank can auction the mortgaged asset to collect the loan amount.

- Sometimes assets become non- performing assets, and maintenance or written-off of such assets cost more to firms.

Applications

They are used in calculating Various ratios like Net assets, ROTA (Return on Total Assets), RONA (Return on Net Assets), Asset Turnover Ratio, DuPont Analysis, etc.

#1 - Net Assets - This is a difference between Total Assets and Total Liabilities.

#2 - ROTA - Return on Total Assets is calculated as the Net income ratio to the total value of its assets.

#3 - RONA - Return on Net Assets is calculated as

#4 - Asset Turnover Ratio - This is an activity ratio, which is calculated as:-

#5 - DuPont Analysis - Asset Turnover ratio is used to perform DuPont Analysis.

DuPont formula analysis is a useful method to decompose the various drivers of return on equity (ROE). Fragmentation of ROE allows investors to focus on the key metrics of financial performance individually to identify strengths and weaknesses. These metrics of financial performance are:-

- Operating Efficiency - Profit Margin represents it.

- Asset Use Efficiency -Asset Turnover Ratio represents it.

- Financial Leverage -It is represented as Equity Multiplier.

Total Assets Vs Current Assets

Both the above are two categories of assets that are clearly stated in the balance sheet of every company. However, it is important to know the differences between them, which are as follows:

- The former represents the total value of all the assets of the business which include the latter, whereas the latter is just the value of assets that can be converted to cash immediately or within one year.

- The former does not represent any particular time horizon but the latter shows only the assets that are meant for short term, which is primarily within one year.

- The former is the total value which represents the total resource of the company whereas the latter is a subset of the former, which shows only the current resource.

- The former depicts both short- and long-term assets but the latter shows only the short-term assets.

Thus, the above are some important differences between the two. However, both the concepts are equally crucial for analysts, investors and the company management for assessment regarding ability of the company to meet its financial obligations.