Table Of Contents

What Is Tier 1 Capital Ratio?

Tier 1 Capital Ratio is the ratio of Tier 1 capital (capital available for banks on a going concern basis) as a proportion of the bank's risk-weighted assets. Tier 1 capital includes the bank’s shareholder’s equity, retained earnings, accumulated other comprehensive income, and the bank's continuously convertible and perpetual debt instruments.

Basel III norms resulted in the tightening of Tier 1 capital norms and the introduction of the Tier 1 leverage ratio to prevent excessive build-up of leverage and to increase the capacity of the banks' capital to cushion possible losses from its exposures. A more robust Tier 1 capital ratio indicates a better ability of the bank to be able to absorb losses. Therefore, as a general rule of thumb, the higher the ratio, particularly the CET1 capital ratio, the better.

Table of contents

Tier 1 Capital Ratio Explained

The concept of tier 1 capital ratio refers to the core capital that a bank will have to keep in its reserve so that its various activities and capital requirements in terms of servicing its clients can be met. The bank tier 1 capital ratio can include certain reserves that require disclosure, certain types of assets or common stock. It is a metric to measure the financial condition and strength of the bank.

- The Global Financial Crisis of 2008 highlighted the weak capital and loss absorption capacity of many financial institutions internationally. Discounts were observed in the computation of capital across geographies and jurisdictions, which reduced the comparability of capital ratios and shook confidence in the reported figures.

- To ensure that high-quality capital was reckoned and to bring about uniformity in the computation of capital ratios of financial institutions, the international committee of banking supervisors – the Basel Committee on Banking Supervision, issued the Basel III accord.

- Basel III norms emphasized increasing the loss-absorbing capacity of banks to be better prepared for financial crisis events by strengthening the banks' capital ratios. Basel III norms required a minimum Tier 1 capital ratio of 6% and the total capital ratio of 8%. The III accord also requires banks to maintain a capital buffer of 2.5% over and above the total capital requirement of 8% to provide additional comfort.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

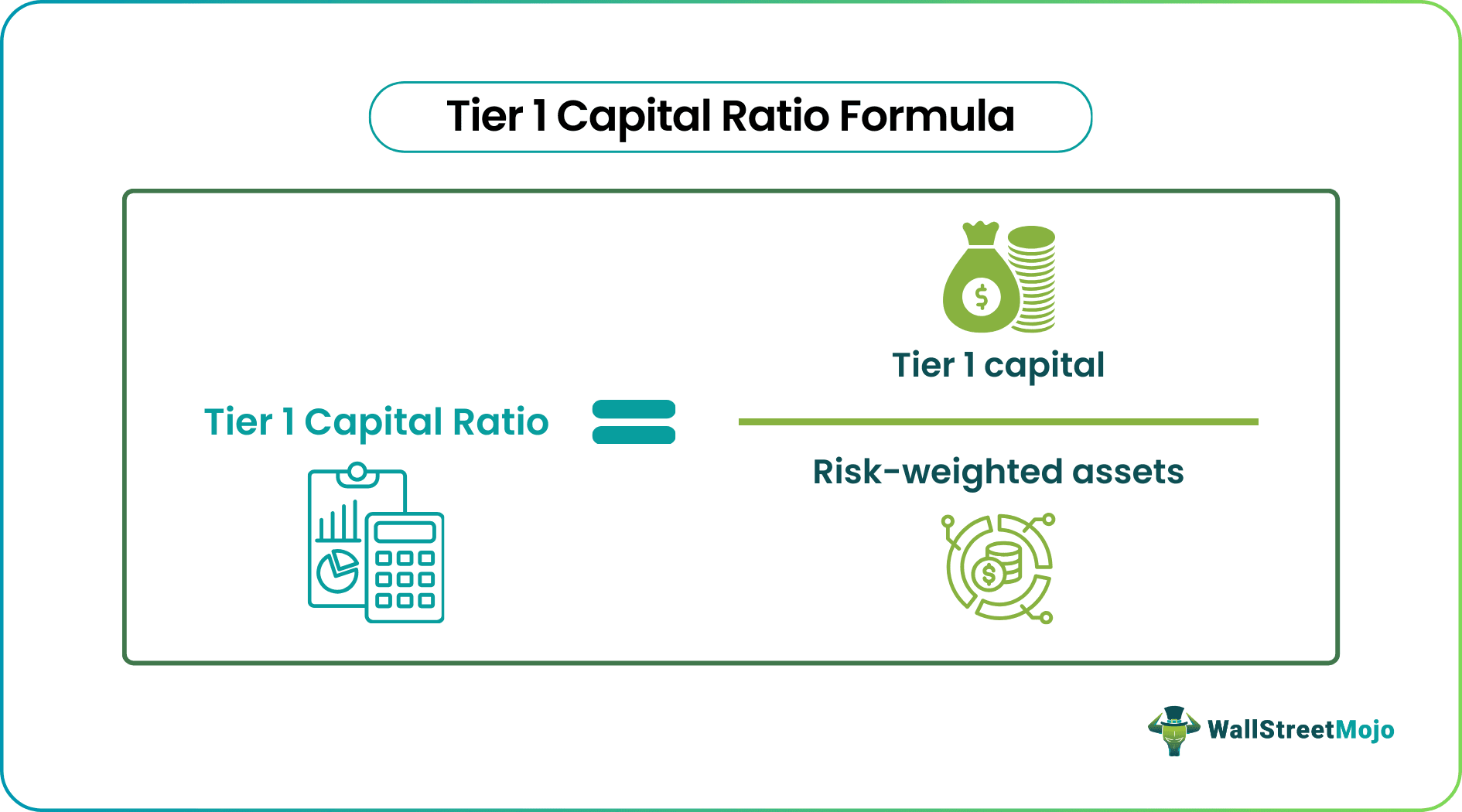

Formula

The bank tier 1 capital ratio can be calculated using the formula mentioned below.

- Risk-weighted assets are the bank’s assets and certain off-balance sheet exposures weighted by the risk weights assigned to the particular categories of the exposures as per regulatory norms. Riskier exposures are assigned higher weights indicating a higher capital requirement to cushion any losses and vice versa. The method in which the risk levels will be measured for such assets are decided by the Central Bank. Typically the assets like cash and securities issued by the government are considered risk free, while home loans or car loans have more risk. As per the risks levels, the weights are assigned while calculating tier 1 capital ratio of major banks.

- The higher the minimum tier 1 capital ratio, the higher its loss-absorbing capacity would be.

Components

Here are some of the components of the minimum tier 1 capital ratio calculation. Let us study them in details.

Tier 1 Capital = Common Equity Tier 1 Capital + Additional Tier 1 Capital

- Common Equity Tier 1 (CET1) Capital - CET1 capital is the core equity capital of the bank and includes shareholder's equity, retained earnings, and accumulated other comprehensive income of the bank.

- Additional Tier 1 (AT1) Capital - AT1 capital includes certain contingently convertible and perpetual debt of the bank since they provide going concern capital to the bank.

OR

Tier1 = CET1 + AT1

- = 4.5% + 1.5%

- = 6%

Basel III accord focused on tier 1 capital ratio requirement and building up the core capital of the banks. As a result, the norms capped the AT1 capital that can be considered Tier 1 capital at 1.5% of the bank's risk-weighted assets.

Example

A suitable example of tier 1 capital ratio requirement will help us understand the concept in detail.

Consider an example of a bank determining its risk-weighted assets at $150,000 million. The amount qualifies as Tier 1 capital after regulator adjustments add up to $10,500 million, with CET1 capital comprising $9,500 million and AT1 capital accounting for the balance of $1,000 million.

This can be calculated as follows:

Alternatively,

- = ($9,500 ÷ $150,000) + ($1,000 ÷ $150,000)

Ratio = CET1 Ratio + AT1 Ratio

- = 6.33% + 0.67%

- = 7%

From the above example, the calculation of tier 1 capital ratio of major banks is very clear and precise. We can easily understand the type of data that is taken into consideration and the steps followed to calculate the ratio.

Tier 1 Capital Vs Tier 1 Leverage Ratio

Both the above are important metrics commonly used in the financial industry. But there are some important difference between them as given below:

- Tier 1 Capital ratio measures the bank's Tier 1 capital proportion to its total assets, including certain off-balance sheet exposures, as opposed to risk-weighted assets considered in the Tier 1 capital ratio calculation. Total assets considered for the bank's leverage ratio are not risk-weighted.

Tier 1 Leverage Ratio = Tier 1 Capital / On and Off-Balance Sheet Exposures.

- The Basel III norms introduced Tier 1 leverage ratio to prevent banks from excessively leveraging their businesses. Basel III prescribes a minimum Tier 1 leverage ratio of 3%.

- Banks considered too big to fail, the failure expected to harm the global economy as a whole, are categorized as Global Systemically Important Banks (G-SIBs). The minimum Tier 1 capital and Tier 1 leverage requirement for G-SIBs is prescribed at a level higher than other banks. The exact regulatory minimum is fixed on a case-to-case basis for each G-SIB separately, taking into account factors such as the size of the bank and its relative importance, its interconnectedness with the economies across jurisdictions, and the level of infrastructure facilities of the bank, etc.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This has been a guide to what is Tier 1 Capital Ratio. We explain the formula with example, its various components & differences with tier 1 leverage ratio. You can learn more about it from the following articles –