Table Of Contents

Tax Liability Meaning

Tax liability refers to the outstanding amount to be paid by an individual or company to the government. At the end of every taxation period, taxes are imposed by the local, state, or central government.

Tax authorities like The Internal Revenue Services (IRS) are tasked with its collection. To curtail tax liabilities, taxpayers can claim deductions, exemptions, and tax credits. Also, taxes are a source of government revenue; they fund national amenities like defense, infrastructure, and healthcare.

Key Takeaways

- Tax liability is the amount that is to be paid to the government. Individuals and firms are taxed by the local, state, and federal governments.

- Taxation is a liability for taxpayers—salaried employees, business owners, professionals, and companies.

- The US has a progressive tax rate system—individuals are taxed at different rates based on income and tax brackets.

- If unpaid, the charges further get added to the current year's tax—will be paid in the next tax period.

Tax Liability Explained

The government charges an array of taxes on individuals and corporate taxpayers. This includes income tax, wealth tax, corporate tax, property tax, service tax, customs duty, gift tax, excise duty, and VAT. The amount yet to be paid to the government is referred to as a tax liability.

The local, state, and federal governments use collected revenue for economic development, defense, and maintenance of infrastructure. Every country levies taxes at different rates and these rates can be amended each year. The US has a progressive tax rate system—individuals are taxed at different rates based on income and tax brackets. There are separate tax slabs for single filers, married couples filing together, married couples filing separately, and head of households. Tax slabs are based on taxable income brackets.

A tax base is an income or asset that falls under the government's tax bar. In a current year, taxpayers are supposed to pay taxes for the previous year’s income. If unpaid, the amount further gets added to the current year's liability which will be paid in the next tax period. Such outstanding charges are known as back taxes.

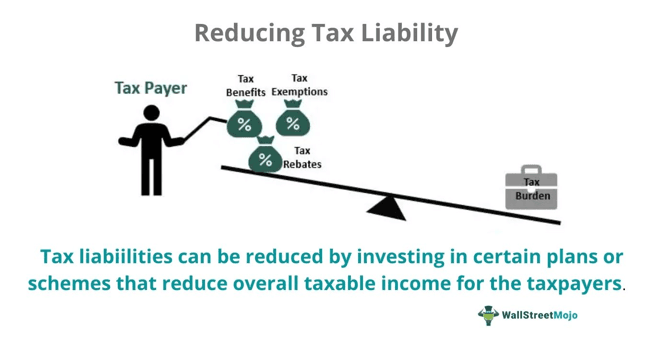

With tax planning, individual taxpayers can bring down income tax liability to as low as zero. Taxpayers can claim deductions for medical expenses (qualified) incurred during the relevant tax period. In addition, contributing to the various tax-benefit savings plans like Flexible Savings Account, 401 (k) plan, Individual Retirement Account (IRA), and Health Savings Account can increase tax deductions. Increased deductions mean lowered liability. One can even claim Earned Income Tax Credit (EITC)—if eligible.

Tax Liability Formula and Calculation

The calculation of liability for a business or an individual involves the following steps:

- First, gross income is computed by aggregating income from various sources—business, profession, salary, rent, capital gain, interest from fixed deposits, savings accounts, etc.

- Then various deductions and exemptions are subtracted from the gross income to acquire the net taxable income. Here deductions refer to all deductions the individual or firm is eligible for.

- If the taxpayer is a company, professionals evaluate the tax liability of employees. 50% of an employee's tax is allocated to social security tax. The remainder goes to Medicare tax and federal unemployment tax.

- Once the tax base is acquired, the tax rate is determined. Professionals refer to the tax bracket of the given period and compute liability. Also, they deduct tax credit from tax liability, if any.

- To calculate the final liability, the company needs to subtract employee taxes from the value derived in step 4.

The following formula is used to compute net taxable income:

Net Taxable Income = Gross Income – Deductions – Exemptions

The formula for calculating tax liability is given below:

For Individuals:

Tax Liability = – Tax Credit

For Companies:

Tax Liability = (Net Taxable Income × Tax Rates) – Employee Taxes – Tax Credit

Examples

Let us look at a few illustrations to understand the calculations:

Example #1

In 2021 Jacob earned a salary of $60,000. He was allowed a $2,000 deduction for qualified medical expenses. Also, he contributed $5,000 towards the 401 (k) plan. Based on income brackets, the tax slab for a single filer in 2021 is given below:

Now, Based on the given values, Find Jacob’s liability.

Solution:

Taxable Income = Gross Income – Deductions

Taxable Income = $60,000 - $2,000 - $5,000 = $53,000

According to the above tax slab, liability is calculated as:

- 10% of $9,950 = $995

- 12% of ($40,525 - $9,950) = $3,669

- 22% of ($53,000 - $40,525) = $27,44.5

- Total Tax Liability = $995 + $3,669 + $2,744.5 = $7,408.5

Thus, Jacob is liable to pay $7,408.5 as federal income tax.

Example #2

XYZ Ltd. made a profit of $217,000 in 2021. The company incurred a total expense of $115,000. The company overpaid the income tax by $9,000 in the previous period, and the corporate tax is applicable at 21%. What is its current liability?

Solution:

Net Profit = Gross Profit – Total Expenses

- Net Profit = $217,000 - $115,000 = $102,000

- Taxable Income = Net Profit = $102,000

- Liability = 21% of $102,000 = $21,420

Current Liability = Tax Liability – Tax Credit

- Current Liability = $21,420 - $9,000 = $12,420

Thus, the tax liability of XYZ Ltd. in 2021 is $12,420.