Table Of Contents

What is Step Cost?

Step cost refers to the cost that doesn't change to the changes in activity levels but instead changes after a certain threshold is crossed. The cost follows the pattern of "steps." As in, they remain stable for a specific level of output. However, once that level is breached, step cost graph increases or decreases in a step-like fashion.

Step cost refers to an expense that changes abruptly at certain activity levels or thresholds. Instead of gradually increasing with activity, the cost remains constant within a range but "steps up" to a higher level once a specific point is reached. This concept is crucial for budgeting, pricing, and decision-making, as it highlights the impact of reaching certain production or activity levels on overall costs.

Table of contents

Step Cost Explained

Step cost, also known as a step-variable cost or a step-fixed cost, is a type of cost that exhibits a sudden and discrete change in value at specific activity levels or production thresholds. Unlike variable costs that change proportionally with changes in activity, step costs remain constant within a certain range of activity and then "step up" to a higher level when that range is exceeded.

We are really well exposed to the concept of variable costs that change in the same proportion as the activity level increases. For example, if the activity level increases by 20%, the variable cost increases by 20%. On the contrary, the cost changes disproportionately in the case of step cost. This is because it follows a step pattern, which means it remains constant up to a certain activity level (e.g., production level). After the activity level reaches the next level, it increases. Similarly, if the activity level is reduced to a previous level, the cost decreases.

Step cost behaviors have significant implications for financial planning, budgeting, and decision-making. They require managers to be mindful of the activity levels at which cost changes occur, as these thresholds can impact pricing, profitability analysis, and capacity planning.

Ignoring step costs can lead to inaccurate budgeting and decision-making, potentially affecting a company's financial performance and competitiveness. Recognizing and understanding step costs is essential for effective cost management and strategic business planning.

Function

The function of a step cost is to represent the sudden and discrete changes in expenses that occur at specific levels of activity or production. Step costs play a crucial role in cost analysis, financial planning, and decision-making for businesses and organizations.

They help managers understand how costs change as production or activity levels vary, enabling more accurate budgeting and strategic decision-making.

By identifying the thresholds at which step cost behavior occurs, businesses can anticipate changes in their cost structure and adjust their strategies accordingly.

These costs also provide valuable insights into cost-volume-profit relationships. Understanding how costs behave as activity levels change helps managers assess the financial feasibility of different production levels and product lines.

Additionally, a step cost analysis can aid in optimizing production schedules, resource allocation, and capacity utilization to achieve operational efficiency.

Formula

Let us now discuss the formula to plot a step cost graph that shall act as a basis for our understanding of the concept and its related factors through the discussion below.

Step Cost = Base Cost + (Additional Cost per Step * Number of Steps Taken)

Where,

- Base Cost: The initial cost that remains constant up to a certain activity level.

- Additional Cost per Step: The increase in cost for each step beyond the threshold.

- Number of Steps Taken: The difference between the actual activity level and the threshold.

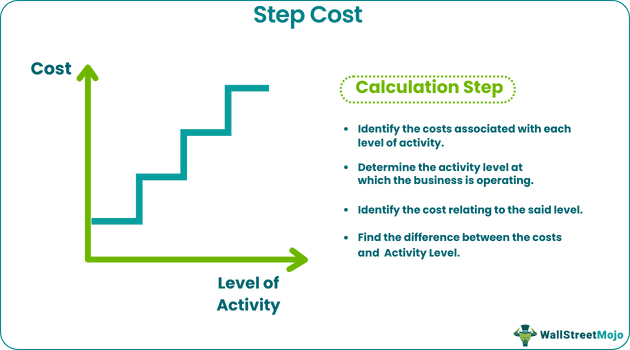

How to Calculate?

Step cost behavior is based on the level of activity that a business is operating in. Therefore, if you need to calculate relating to any business or a division, you need to follow the below steps:

- Identify the costs associated with each level of activity. For example, suppose the cost of electricity for producing up to 5,000 units is $10,000; the cost increases to $12,000 once the number of units goes above 5,000. Further, the cost increases to $15,000 once the units are produced to exceed the next activity level, 10,000. It would help if you properly defined the cost relating to different activity levels.

- Determine the activity level at which the business is operating based on the activities being carried out.

- Based on the activity level that the company is currently operating at, identify the cost relating to the said level.

- Suppose you need to check the incremental cost. In that case, you can find the difference between the business's costs at the current activity level and the previous activity level.

Examples

Now that we have a clear understanding of step cost behavior’s basics, formula, and how to calculate, let us understand the practical application of the concept and its intricacies through the examples below.

Example #1

Carrying on the above discussion, let us suppose the electricity expenses incurred by the company for various activity levels (i.e., production level) is as follows:

This example mentions the cost relating to various activity levels (i.e., units produced). Suppose the company is operating at a production capacity of 18,000 units.

As per the applicable threshold, the step cost for 18,000 units is $20,000 since the activity level lies in the last threshold of 15,001-20,000 units.

Further, the incremental step cost for each activity level is calculated as below:

Example #2

Chevron, the oil refinery company with a significant market share that sells various refined products such as gasoline, diesel, marine, and aviation fuels is headquartered in California.

In March 2023, they took significant steps towards carbon capture and storage (CCS). They intended to capture 25 million tons by 2030.

Their Vice president said that the players in the market have been conversing about the reduction of costs in this regard for as long as the technology has existed. However, since the smaller players in the market are struggling, it gives larger companies like themselves to take appropriate steps that can allow a step change to occur in the costs of succeeding at this technology.

Applications

Let us understand the applications of the data interpreted from a step cost graph through the points below.

- It is applicable mainly when the company is about to reach the next higher activity level.

- In such a case, the management has to carry out a cost analysis; they need to decide the additional cost that the business will incur if it takes its business activity level to the next stage.

- This incremental cost is then compared with the additional revenue that the company is expected to earn. Accordingly, a decision is taken as to whether it is feasible to move to the next activity level.

- If the incremental revenues are greater than the incremental cost, the management makes the necessary investment of incremental cost. However, if the returns fall below the incremental cost, the activity level is not increased.

Importance

Let us discuss the importance of understanding the points on a step cost graph through the explanation below.

- It is an important factor in deciding whether the business's activity level can be increased or not, based on the incremental benefit that the decision will bring.

- The company can decide whether it is profitable to move to the next activity level, considering the additional cost that the company will incur.

- It helps the company decide to increase or decrease the business activity level.

Recommended Articles

This has been a guide to what is Step Cost. Here we explain its examples, functions, formula, applications, how to calculate, and importance in detail. You may learn more about financing from the following articles –