Table Of Contents

What Is Solvency II?

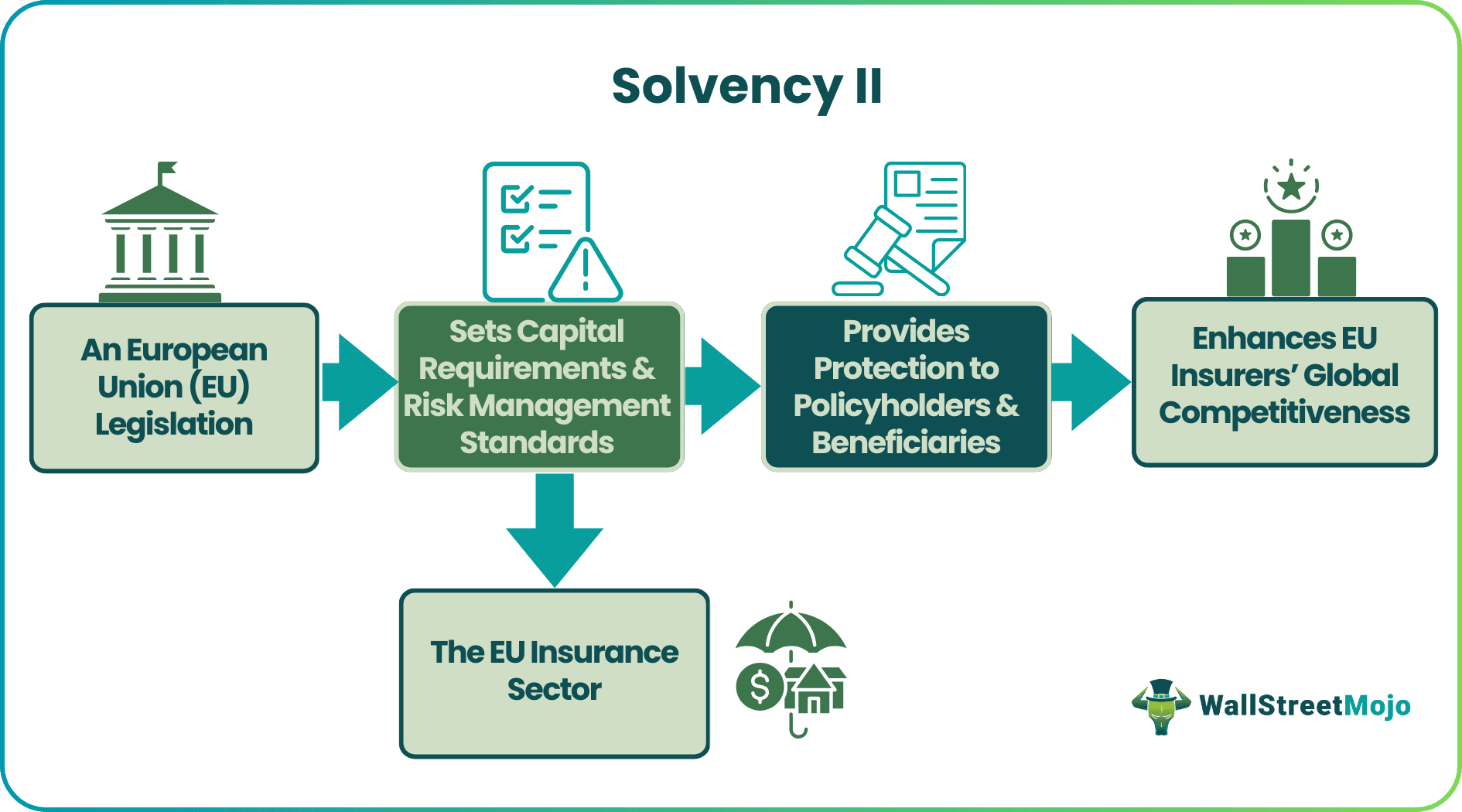

Solvency II refers to a risk-based capital regime that establishes a number of risk management standards and capital requirements for reinsurance and insurance companies in the European Union (EU). Its aim is to ensure sufficient protection for beneficiaries and policyholders.

The legislation, which came into effect on January 1, 2016, underpins the significance of adopting a risk-based approach for evaluating and reducing risks associated with insurance companies in Europe. It mandates roles like actuarial, independent audit, risk management, and compliance functions by imposing formal governance requirements. These prudential regulations vary based on the diversity and riskiness of an insurer’s operations.

Table of Contents

- What Is Solvency II?

- Solvency II refers to a prudential regulations program for reinsurance and insurance undertakings in the European Union. Two crucial objectives of this regime include increasing the harmonization levels concerning solvency regulation throughout Europe and protecting policyholders.

- A key difference between Solvency II and IFRS 17 is that the latter does not specify any liquidity premium, unlike the latter.

- Three Solvency II pillars form the structure of the regime’s framework. They are financial requirements, governance and supervision, and reporting and disclosure.

- This regime is not as exposed to pro-cyclical impact as Basel III.

Solvency II Explained

Solvency II refers to a legislative program introduced in the EU that establishes a prudential, robust, and harmonized framework for insurance and reinsurance companies. The program's key objectives include deepened European Union market integration, modernized supervision, and enhanced customer protection. Moreover, it aims to improve EU insurers’ international competitiveness.

This regime regulates the overall capital EU insurers must hold to minimize the insolvency risk. Moreover, it imposes requirements concerning risk management and governance, transparency, disclosure, and insurance companies’ effective supervision. That said, the requirements set by this prudential regime must be proportionate to an insurer’s scale, complexity, and nature.

To better understand this risk-based capital regime, let's examine the three Solvency II pillars that form the framework's structure.

- Pillar 1 – Financial Requirements: It sets out the regime’s quantitative requirements, which include the rules organizations must follow to value liabilities and assets, compute capital requirements, and identify the eligible ‘own funds’ so that they can fulfill those requirements.

- Pillar 2 – Governance & Supervision: This pillar sets out all requirements concerning governance, risk management, and the supervisory process’s details with competent authorities. This helps ensure the regulatory framework includes every undertaking’s informed business decision and risk management system.

- Pillar 3 – Reporting And Disclosure: The third pillar addresses transparency as insurers in the EU need to send reports to send disclosures to the public and reports to the supervisory authorities. This improves market discipline and increases comparability, which, in turn, results in increased competition.

The introduction of this regime eliminated the capital-related restrictions that Member States were previously imposing on insurance companies’ investment portfolios. Insurers can now invest freely as the capital requirements will be dependent on the actual risk associated with the investments.

Many traders use Saxo Bank International to research and invest in stocks across different markets. Its features like SAXO Stocks offer access to a wide range of global equities for investors.

Features

The key characteristics of this regime are as follows:

- Proportionate: The regime’s requirements must be proportionate to the scale, complexity, and nature of the risks inherent to insurers and reinsurers. This promotes transparency, competitiveness, and comparability.

- Risk-Based: A vital aspect of this regime is risk-based capital requirements. This is because it involves determining the capital an insurer needs to have so that it can cover unforeseen losses. Simply put, the higher the level of risk, the higher the amount of capital required to cover potential losses.

- Group Supervision: Per this directive, supervisors need to increase the exchange of information and coordination to enhance cross-border supervision concerning reinsurance and insurance groups.

- Market Consistent: According to the regulations, the asset valuations should be such that their transfer, settlement, and exchange can take place easily.

Examples

Let us look at a few Solvency II examples to understand the concept better.

Example #1

J.P. Morgan analysts highlighted the positive effects Solvency II reforms could have on the United Kingdom life insurers, specifically those involved in annuity writing and Pension Risk Transfer or PRT. Per expectations, the proposed reforms could improve Solvency II ratios and reduce capital strain for the insurers. Moreover, a tapering mechanism might be introduced, which could decrease interest rate sensitivity, a major concern for long-term capital-intensive businesses like annuities.

Overall, the changes can boost the growth and stability of UK insurance companies, especially those operating in the Pension Risk Transfer (PRT) and annuity sectors.

Example #2

On December 13, 2023, the EU agreed to make amendments to the Solvency II directive, which would ease the capital rules for insurance companies. This step could free up substantial funds for investment in infrastructure and green technology to increase growth. In fact, the alterations enable the EU insurance sector to invest funds worth up to an additional $108.82 billion in the economy, which equals around 0.6% of the gross domestic product (GDP) of the EU.

The alterations include newly-created provisions necessitating insurance companies to better consider risks concerning sustainability. Moreover, the changes also will require insurers to report more regarding such risks to help policyholders understand a company’s green credentials.

Solvency II vs Basel III

An individual who is new to the concepts of Solvency II and Basel III may find them confusing. They can combat this issue and clearly understand their meaning and purpose by knowing the following key differences:

| Solvency II | Basel III |

|---|---|

| In general, the standard formula of Solvency II is risk-sensitive; it combines factor-based and scenario-based models. | The standard approach of Basel III involves utilizing a static risk factor-based model. |

| This regime imposes certain regulations on reinsurance and insurance companies in the EU. | Basel III includes certain measures developed for banking supervision following the 2007-09 financial crisis. |

| Key objectives of this program include safeguarding policyholders and beneficiaries. | The primary aim of Basel III is to strengthen the supervision, risk management, and regulation of banks. |

| In this case, the regulations and standards apply to the insurance sector in the European Union only. | The reform measures apply to the international banking sector. |

| It is less susceptible to pro-cyclical impact. | Basel III is more exposed to pro-cyclical impact. |

| The appreciation of funding risk and mismatch is more. | In this case, the appreciation is less. |

| Capital definitions are stricter. | Capital definitions are less strict in this case. |

Solvency II vs IFRS 17

There are some key differences between Solvency II and IFRS 17. Individuals hearing about such terms for the first time must know them to avoid any confusion. So, let us look at the table highlighting the distinct features below.

| Solvency II | IFRS 17 |

|---|---|

| It specifies the liquidity premium and risk-free rate. | No restriction concerning liquidity premium exists. |

| In this case, the measures are more comprehensive and prescriptive. | The measures are less comprehensive. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Under Solvency II, insurance companies need to compute their liabilities’ value utilizing a risk-free rate of interest. The matching adjustment refers to an upward adjustment made to that risk-free interest rate where the insurance providers hold specific long-term assets along with cash flows matching the liabilities.

This capital regime replaced Solvency I, which aimed to revise and update the EU solvency regime. The replacement took place as Solvency I showed structural weaknesses, had a relatively narrow scope, and did not reflect the actual risk that insurance providers generally face.

Solvency capital requirement or SCR refers to the overall funds reinsurance and insurance providers must hold under the EU’s directive to ensure 99.5% confidence that the companies could incur the highest possible expected losses over a year and still survive.

The Tier 1 ‘own funds’ consist of on-cumulative preference shares, relevant sub-ordinate liabilities, and ordinary share capital. In the case of a solvency capital requirement breach, all distributions concerning Tier 1 items need to be canceled. Moreover, principal repayment must be suspended.

Recommended Articles

This article has been a guide to what Is Solvency II. Here, we compare it with IFRS 17 and Basel III, and explain its examples and features. You may also find some useful articles here –