Table Of Contents

What Is Social Security Tax?

A social security tax is a mandatory contribution paid by employees and employers in the United States. The employer is responsible for withholding social security payments from the employee's salary.

It is one of the two taxes employers must withhold under the Federal Insurance Contribution Act (FICA). FICA comprises social security payments and Medicare tax. In 2023, employees and employers are mandated to pay 6.2% of wages towards social security. The collected revenue is used to support American citizens who are old, weak, and entitled to survivor benefits.

Key Takeaways

- Social security tax is a US government tax imposition on all working citizens and employers to contribute to the federal program.

- This tax comes under the purview of The Federal Old Age, Survivors, and Disability Insurance (OASDI) program. It is regulated by the Social Security Administration (SSA).

- Individuals must collect 40 credits to qualify for social security benefits; typically, the beneficiary must have paid social security for at least a decade.

- The collected funds are distributed among beneficiaries on a "pay-as-you-go" basis.

How To Calculate?

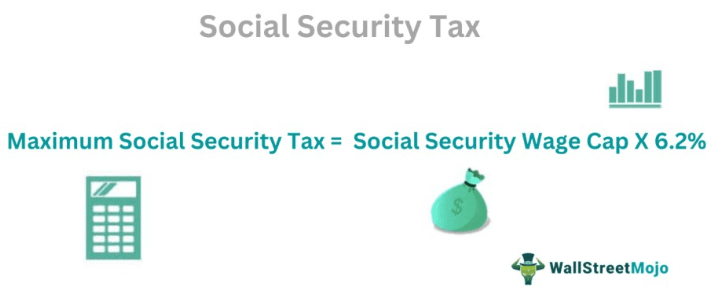

Social security payment is only taxed up to a certain income level. In 2022, the social security payment was capped at $147,000. In 2023, the tax is capped at $160,200. Therefore, an employee earning $180,000 will only be taxed for $160,200. Therefore, the maximum amount of employee social security payment that can be withheld from an employee's paycheck in 2023 will be $9,932, equivalent to 6.2% of $160,200.

According to the Social Security Administration, 66 million Americans will receive monthly social security benefits in 2022. On average, each recipient received $1,681. However, this number is expected to rise in 2023—close to $1,827 owing to an increased cost of living.

Examples

Now let us look at social security tax examples.

Example #1

Aubrey had just graduated from college; a private company hired her. She is 22 years old and pays 6.2% of her annual salary for social security. The employer pays another 6.2% tax.

The contributions are accumulated and used to support American citizens who are old, weak, and entitled to survivor benefits. Social security payment benefits are offered to a surviving spouse upon the spouse's death or to a dependent child in case of their parent's death. The Old Age administers the benefits, Survivors, and Disability Insurance (OASDI) Program.

Example #2

2023 brings with it major social security changes. But the income tax applied to social security benefits remains unchanged. If an individual's total income surpasses $25,000, they must pay a tax on 85% of social security benefits. There is a widespread call for the amendment of this law; it has not been adjusted for inflation.

Exemptions

Let us look at social security tax exemptions.

- People belonging to certain religious groups are exempt from social security payments—only if they claim this right.

- Foreign scholars, students, teachers, workers, and citizens working in the US are exempted from social security payments. It includes immigrants and non-resident aliens.

- Diplomats and government officials residing in the US but belonging to a foreign nation are exempt from social security payments.

- When an individual attains retirement age, they no longer have to pay for social security.

- US government employees applying for public retirement plans do not have to pay for social security.

Social Security Tax Explained

A social security tax is a mandatory contribution paid by employees and employers in the United States. The Federal Old Age, Survivors, and Disability Insurance (OASDI) program comes under the purview of the Social Security Administration (SSA).

Simply put, the US government collects a portion of employee income to support sections of society that need assistance. This tax is collected from all working employees and their employers. The employee and the employer contribute a fixed 6.2% each, comprising a 12.4% tax rate.

The social security administration amends tax regulations once a year. Social security payments do not have any age brackets. All employees pay the same rate till retirement age. When an employee quits a job, social security payments stop. But, the tax resumes as soon as the individual begins the next job role. Social security collection varies from state to state; some US states do not collect social security payments from citizens.

If the recipients of social security benefits have a substantial income from another source, the entire amount is considered taxable. For example, this additional income could be in salary, self-employment, interest from investments, bonds, dividends, etc.

The cap on social security payments receives a lot of criticism—it is considered a regressive tax. This is because employees cannot be taxed for amounts beyond the cap. The term regressive tax refers to a taxation system where taxes are levied irrespective of the income level of individuals. This means that people with higher and lower income groups are liable to pay an equal amount as tax, thereby making the poor pay higher taxes despite having limited earnings.

In addition to social security, employees and employers pay a Medicare tax, split into two halves—between the employee and employer (2.9% total, 1.45% each). The Federal Insurance Contributions Act (FICA) is a federal law. FICA payments are a combination of social security payments and Medicare taxes—together, they constitute 15.3% of employee earnings. Thus, employees are liable for one-half—7.65%, which includes a 6.2% Social Security tax and 1.45% Medicare tax on their earnings.