Table Of Contents

What Is Shadow Banking?

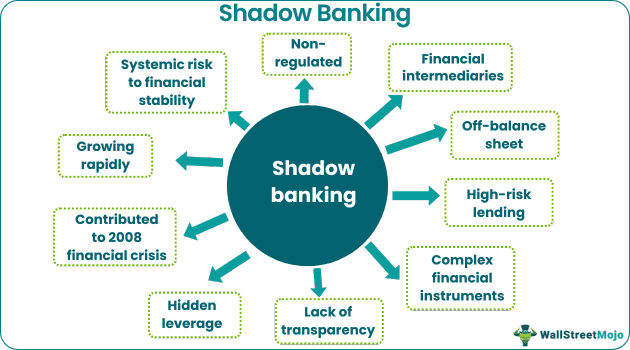

The shadow banking system refers to the network of non-bank financial intermediaries that offer services similar to traditional banks. Despite their important role in the financial system, they are not subject to the same regulations and oversight as traditional banks, as they operate outside the regulated banking sector.

These institutions typically engage in securitization, repurchase agreements, and other forms of lending and borrowing that can create liquidity and provide credit to individuals and businesses. However, some of them can also pose risks to the financial system if they become too large or interconnected, making it important for regulators to monitor and regulate the sector to help mitigate systemic risks.

Table of contents

- What Is Shadow Banking?

- Shadow banking refers to a system of non-bank financial intermediaries that engage in activities similar to traditional banks but without being subject to the same regulatory oversight.

- It can include money market funds, investment banks, and non-bank finance companies (NBFCs).

- They played a significant role in the 2008 financial crisis, as the collapse of institutions such as Lehman Brothers and American International Group (AIG) led to widespread financial turmoil.

Investors seeking a comprehensive platform may consider Saxo Bank International for a variety of account types and investment options.

Shadow Banking System Explained

The shadow banking system is defined by the Financial Stability Board (FSB), an international organization, from a broad and narrow perspective. "Credit intermediation and activities involving entities outside the traditional banking system" is the FSB's wide definition of this system. At the same time, its narrow definition states that developments increase systemic risks, particularly in maturity or liquidity transformations, imperfect credit risk transfers, leverage, and indications of regulatory arbitrages that undermine the advantages of financial regulation.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Two crucial elements make up the definitions, as mentioned earlier:

- First is the involvement of non-banking financial institutions or organizations not affiliated with a bank that carry out "bank-like" activities of maturity and liquidity transformation, credit risk transfer, and direct or indirect financial leverage.

- Second, executing operations like securitization, securities lending, and repo transactions are significant funding sources for non-bank firms. Thus, entities that actively engage in financial intermediation, such as finance companies or NBFCs, or provide financing to such entities, like mutual funds, are considered shadow banks.

Globally, these organizations could be categorized under the following broad categories:

- Money market funds

- Credit investment funds

- Hedge funds

- Finance companies that accept deposits or deposit-like funding

- Securities brokers' dependent on wholesale funding

- Securitization instruments

It's worth noting that different countries and regions may have different definitions of shadow banking, and this list may not be comprehensive or equally applicable in all locations.

For efficient cross-border payments, many individuals and businesses use the Wise Money Transfer UK or Wise Money Transfer US services for transparent and low-cost transfers.

Function

Shadow banking was primarily concerned with non-bank financial entities participating in maturity transformation. For example, when commercial banks fund long-term loans with deposits, which are often short-term, they engage in maturity transformation. The same is true of shadow banks. In the money markets, they generally raise or borrow short-term funds that they then utilize to purchase assets with longer-term maturities.

However, because typical bank regulations do not govern them, they cannot borrow money from the Federal Reserve in a time of need. In addition, they also lack traditional depositors whose money is insured; as a result, they operate in the 'shadows.'

Broker-dealers that use repurchase agreements to fund their assets would be included in the ambit of shadow banks. In a repurchase agreement, an entity that needs money sells a security to raise the cash required and then promises to buy the security back at a set price and on a certain date to pay back the loan. Shadow banks also include money market mutual funds that pool investors' money to buy corporate IOUs (commercial papers) or mortgage-backed securities. The same goes for finance companies that sell commercial paper and then utilize the revenues to grant credit to households.

Examples

Here are some shadow banking examples -

Example #1 - 2008 Financial Crisis

Financial institutions other than the traditional banking system presented a grave threat to financial stability, as learned from the 2007–2008 financial crises. Moreover, the crisis was significantly exacerbated by the near failure of non-bank financial institutions such as Lehman Brothers, an investment bank; American International Group (AIG), an insurance company; and GE Capital, a finance company.

These shadow banks produced subprime mortgages, packaged them into mortgage-backed securities, and distributed them throughout the financial system. It contributed to the crisis of 2007–2008. Similar to the traditional depositor runs, they also worsened the crisis as creditors fled the shadow banking industry.

Organizations like Lehman Brothers and AIG became systemically important due to their scale, connectivity to other financial firms, the complexity of operations or assets, reliance on short-term funding, and vulnerability to bank-type runs, leverage, and other factors. In essence, the failure of these non-bank financial institutions was one of the contributing factors to the 2008 financial crisis, but the shadow banking sector did not solely cause it.

Example #2 - Companies

One example of an organization engaged in shadow banking is a money market fund, which pools money from many investors to purchase short-term, low-risk securities such as government bonds, certificates of deposit, and commercial paper. Money market funds are considered shadow banks because they carry out bank-like activities, such as maturity transformation, but are not subject to the same regulations as traditional banks.

Pros And Cons

Pros of shadow banks:

- More lending options: They offer more lending options and alternative forms of financing, making credit more readily available to individuals and businesses.

- Lower costs: They typically operate with lower overhead costs and can offer lower interest rates and fees than traditional banks.

- Flexibility: They often offer more flexible repayment terms and can be more adaptable to changing economic conditions.

- Faster processing times: They can often process loan applications and disburse funds more quickly than traditional banks.

Cons of shadow banks:

- Lack of regulation: They are often not subject to the same level of regulation as traditional banks, which can lead to higher risk for borrowers and lenders.

- Insufficient protection: They do not have the same level of insurance protection as traditional banks, which means that borrowers and lenders may face a greater risk of loss.

- Opacity: They are often less transparent than traditional ones, making it difficult for borrowers and lenders to understand the risks involved.

- Market instability: They can significantly create instability, particularly during economic turbulence. It can lead to a negative impact on both borrowers and lenders.

Shadow Banking vs Traditional Banking

Let us look at the differences between shadow and traditional banking:

| Points | Shadow Banking | Traditional Banking |

|---|---|---|

| Regulations | Less regulated and often operate outside the traditional banking system. | Heavily regulated by government agencies, such as the Federal Reserve and FDIC. |

| Deposits or nature of business | Involved in non-deposit-taking activities, such as lending, securitization, and investment banking. | Take deposits from customers and use that money to make loans. |

| Market position | Often viewed as more speculative and less secure. | Plays a central role in the financial system and is seen as more stable and secure. |

Want a smarter way to bank on the go? Revolut offers a user-friendly app with global access, crypto and stock trading, and innovative budgeting tools—all in one powerful platform.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Shadow banking is not illegal. However, regulations may vary by country, and activities that fall under the definition of shadow banking may be subject to different rules and oversight compared to traditional banking activities. Shadow banking regulation aims to reduce systemic risk, improve transparency and stability in the financial system, and protect consumers.

There are several suggestions on how it can be regulated, and some of them involve enacting legislation to improve and better monitor systemically risky shadow banks, implement steps to minimize the development of risks in the shadow banking industry, especially systemic risks, and better supervision of securities financing transactions (SFTs), etc.

NBFCs are known as shadow banks because they are not regulated as strictly as traditional banks and operate similarly to banks but without being subject to the same level of regulatory oversight. As a result, it can make them more vulnerable to financial risk and instability.

Recommended Articles

This has been a guide to what is Shadow Banking. We explain its examples, compare it with traditional banking, its functions, and pros & cons. You can learn more about it from the following articles –