Table Of Contents

What Is A Secured Creditor?

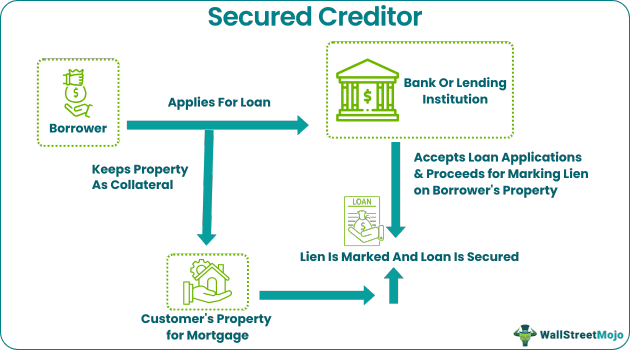

A secured creditor refers to a financial institution that lends money to debtors by taking collateral as security. They do it to safeguard the money lent to borrowers in case of default by selling the collateral security and having first right over the asset in case of bankruptcy filings by the debtor.

Debtors get better purchasing power, good terms and conditions, and a low processing fee in case of loans backed by collateral. However, the collateral placed as security gets marked as a lien. It allows the creditor to seize & sell the property in case of debtor's default. Therefore, lenders collect collateral security from debtors with poor credit records.

Table of contents

- What Is A Secured Creditor?

- A secured creditor provides credit to a borrower in place of collateral as security for the loan to ensure that the loan can get cleared if there is a loan default or bankruptcy.

- It safeguards the lender's money and ensures hassle-free sale of the collateral to close the loan.

- Some secured creditor loans are home, mortgage, and vehicle loans.

- The presence of collateral to safeguard the loan is the major difference between a secured creditor and an unsecured creditor.

Secured Creditor Explained

A secured creditor refers to a type of creditor that provides a loan to a debtor after pledging its asset as collateral for the loan. In other words, secured creditor meaning implies a process where the lender marks a lien on the property the borrower offers as collateral. After marking the lien, the creditor gets the legally enforceable right to sell the collateral to get the full loan amount. For this, the lender often registers the claim of lien in a government authority like official land records constituted for the same. So, creditors use it to stop the customer from hindering secured creditor loans.

The collateral loan is a protection shield for the loans of the creditor that it gives to an individual or a business. It is so because if an individual or firm defaults on a loan under collateral, the lender can use the legal right. They can approach the court to auction the property and get its money back due in the loan. Moreover, in case of bankruptcy of a business or individual, the secured lender having collateral property gets the first right of claim to sell off the property and close the loan.

Collateral also provides a surety of loan to the individual or firm with a weak credit record. It is because the collateral guarantees the full repayment of the loan to the creditor in case of a borrower's default. Also, one should note that chapter 7 & chapter 13 of bankruptcy law does not give any immunity to the borrower in case of a bankruptcy filing. As a result, the lender can go for the secured creditor bankruptcy and claim the collateral property for selling to close the loan.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Examples

Let us use a few secured creditor examples to understand the concept better.

Example #1

One of the best examples of this type of loan is a mortgage loan by a bank. Under this type of loan, a bank receives an application for a loan against property from the borrower. The bank then asks for necessary documents and copies of property documents to be verified for any lien on the property and the genuineness of the property owner.

After the genuineness and lien-free status of the property are verified, the bank then asks the borrower to get the valuation of the property for setting as collateral for the mortgage loan. The borrower and the lender sign an agreement of mortgage soon after they complete the valuation. It gives the lender the property's right to ownership through a lien.

Hence, the banks send the borrower's property to the appropriate authority for marking a lien after the bank approves the loan and before sanctioning the loan amount for disbursal. The bank owns the property until the borrower fully repays the mortgage loan. Then, in case of default by the borrower or bankruptcy of the borrower, the secured creditor lays claim over the property and sells it off to clear the outstanding loan amount and close the loan.

Example #2

Another example of this type of loan is a vehicle loan. Under it, the secured creditor facilitates buying vehicles for and on behalf of the customer. After that, the customer goes to the bank and applies for a vehicle loan, availing of secured creditor rights. The bank then extracts the applicant's credit score and assesses the customer's eligibility for a car loan.

After the bank gets assurance that the customer can repay the car loan, it disburses the amount equal to 80% of the car's price in the form of a cheque in the name of the car dealer. So, after the borrower receives the car, the bank hypothecates the vehicle in its reputation for securing the loan collaterally. Finally, it gets done to secure the car loan and give the right of sale of the vehicle by the bank to clear the outstanding loan amount to incase the car owner defaults on the loan.

Example #3

On June 30, 2020, a Canadian entertainment company, Cirque Du Soliel, incurred a heavy loss due to the COVID-19 pandemic. Cirque had a liability of $1.5 billion. So they filed for bankruptcy protection from their creditors. They filed under the CCAA – Companies' Creditors Arrangement Act in the United States.

Later, Cirque accepted a purchase offer from their creditors, serving as a minimum bid for the investor's auctions. The creditors acquired all of the company's assets according to an agreement. The company promised the lenders a 40% stake under the TPG consortium's proposal. The shareholders would have assigned a smaller debt share to the creditors.

So, a new agreement on a second stalking horse bid replaced the decisions between the company on its secured creditors and its shareholders like Chinese Fosun, American TPG, and others as lenders opposed the deal. The secured creditor's rival bid had set a low-end bar for buying its assets.

Further, the creditors offered to invest $300 and $375 million into Cirque and reduce its debt. It will also maintain the company's headquarter.

Secured Creditor vs Unsecured Creditor

The secured creditor and unsecured creditors are different from each other, as discussed in the following table.

| Secured creditor | Unsecured creditor |

|---|---|

| It is a type of creditor that give loans to a debtor based on the collateral provided to it. | Under this type, the creditor provides a loan to the debtor without any security or collateral. |

| The collateral pledged by the debtor to the lender acts as security against any default on the loan by the debtor. | In case of default, the lender cannot mark any property of the borrower as a lien in court to recover the loan. |

| The secured creditor marks a lien over the collateral property that gives it primarily the legal right of sale to recover its loan in default of loan or bankruptcy. | This type of loan gets provided by the lender to only the salaried account holder having salary disbursed through the lender and to the existing customer with a good relationship and track record with the bank in the form of a credit card. |

| In case of default or bankruptcy, the lender can take the court’s help to sell the collateral property to recover the loan. | The debtor cannot get forced to repay the loan by the unsecured creditor. |

| A mortgage loan, car loan, and HELOCS are some of the instances of secured credits. | Personal loans are loan types provided by the unsecured creditor. |

| Furthermore, a person with weak or poor credit history can also get a loan from the creditor as the loan gets fully covered with the lien marked on collateral that always has a higher value than the loan amount. | Moreover, the lenders do not provide loans to everyone but a select few, even if the person has the best credit score as they are unsecured loans. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

To become a secured creditor, one must- register the business trade name with the government, use UCC-1 filing to enforce the process easier, get a security agreement done, common law copyright established, and a change backorder is required. Finally, get UCC-1 recorded in the name of the secretary of state's office in the debtor state.

Bondholders refers to investors acquiring bonds from organizations, governments, or corporations. They invest in debt secured by an asset. Issuers specifically keep their assets are mortgages while taking debt. As a result, bondholders have secured creditors.

Hinder secured means the debt collectors try to destroy the property to collect their dues. Such at is illegal and against the debt collection laws.

A secured creditor can buy any house by – getting all the details of the property, outlining the necessary conditions for the buying, stating ways for repayment by the seller, and getting a covenant readied to prevent any reselling of the property by the seller.

Recommended Articles

This article is a guide to What is Secured Creditor. Here, we explain it with examples and compare it with unsecured creditors. You can also go through our recommended articles on corporate finance -