Table Of Contents

What Is The Right of Redemption?

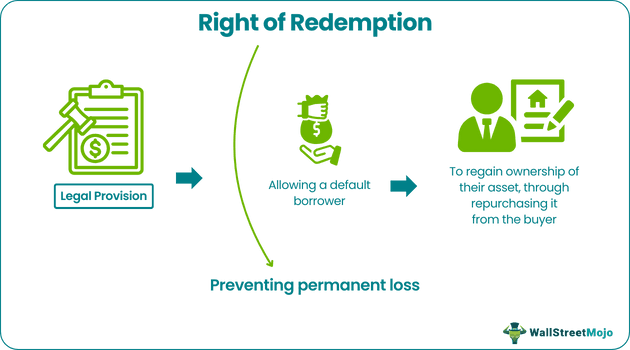

The right of redemption is a legal provision that grants defaulting debtors the ability to reclaim their asset, which was sold due to non-payment or foreclosure of a loan, by repurchasing it from the buyer within a specified time frame. Its primary purpose is to protect borrowers' rights and allow them to regain their assets without permanent loss.

The right of redemption is commonly utilized in tax sales and mortgage foreclosures. It prevents borrowers from facing homelessness or losing their property by allowing them time to manage their finances. However, exercising the right can involve lengthy legal proceedings and uncertain situations for buyers, who may risk losing the capital they invested in purchasing the asset if the borrower decides to redeem their property.

Key Takeaways

- The right of redemption grants defaulted borrowers or debtors the ability to repurchase their asset, which was sold due to non-payment or foreclosure, within a specified timeframe.

- Its purpose is to protect borrowers' rights and prevent permanent asset loss.

- The right of redemption allows borrowers to reclaim their property by paying off the outstanding debt, penalties, fees, and interest.

- The right of foreclosure enables lenders to recover their invested capital by allowing borrowers to reclaim the property before the foreclosure decree is finalized.

How Does Right Of Redemption Work?

The right of redemption is a legal concept in banking that allows a debtor to reclaim their property, which has been sold or foreclosed upon, by compensating the buyer with expenses and costs within a fixed time frame. It is crucial in loan agreements, particularly in mortgage loan foreclosure, non-repayment, and tax sales.

When a homeowner purchases a home using a mortgage loan, the property becomes collateral for the loan. If the homeowner defaults on mortgage loan repayment, the bank can initiate foreclosure and seize property ownership based on the loan agreement.

Foreclosure occurs when certain conditions are met:

- First, the borrower has missed three consecutive loan installments.

- Second, the borrower fails to inform the lender after receiving a default notice.

- Third, the borrower does not pay the missed installments and late fees after receiving the default notice.

Once these conditions are met, the lender can file for foreclosure and proceed with the sale of the mortgaged property. If the lender successfully forecloses on the home, they can sell the property to recover the outstanding dues and close the loan.

However, the borrower is granted a redemption period after the foreclosure. During this time, the borrower can fully repay the loan and halt the foreclosure proceedings. They may also have the right to repurchase the property from the buyer through a redemption bond. The redemption period provides debtors sufficient time to reclaim their homes and resolve the outstanding debt, ensuring the possibility of regaining ownership and avoiding complete property loss.

The redemption process involves complex legal procedures, necessitating debtors to understand applicable laws thoroughly. Borrowers can exercise their redemption right before or after the foreclosure auction, but they must repay the purchase cost, expenses, interest, and fees within the stipulated redemption period. The right of redemption in mortgage loans serves as a means for homeowners to regain their property and provides an opportunity for profit for buyers who purchase homes below market value. In addition, it offers borrowers a lifeline and a second chance to save their property and avoid displacement.

Examples

Let us look at a few examples to get a good hold on the topic.

Example #1

Suppose Sarah is facing financial difficulties and falls behind on her mortgage payments. As a result, the lender initiates foreclosure proceedings on her property. However, Sarah's right of redemption allows her to reclaim the property within a specified timeframe by paying off the outstanding debt, fees, and penalties. She manages to secure a loan and exercises her right of redemption, paying the full amount owed to the lender. As a result, Sarah regains ownership of her property and avoids losing her home.

Example #2

Suppose Michael, a homeowner, encounters unexpected financial challenges and defaults on his mortgage payments. As a result, the lender begins the foreclosure process on his property. However, Michael exercises his right of redemption by selling some of his assets and borrowing funds from family members. He approaches the lender and pays off the outstanding debt, fees, and interest before the foreclosure process is finalized. As a result, Michael successfully exercises his right of redemption, reclaiming his property and resolving the default situation.

Right Of Redemption vs Equity Of Redemption

Let us compare the two using the table below:

| Right of redemption | Equity of redemption |

|---|---|

| It allows the borrower to reclaim their home after foreclosure proceedings by paying the remaining debt, penalties, fees, and interest before the foreclosure decree finalizes. | Debtors must pay the costs associated with outstanding debt and interest associated with foreclosure. |

| Borrowers are provided with a redemption period before or after the foreclosure. | Borrowers could avail of it only before the court finalizes the foreclosure. |

| It differs from state to state. | It is available to borrowers in all the states. |

| Borrowers must pay the full cost, including penalties (if applicable), foreclosure sale price, and interest. | Debtor must pay the costs associated with outstanding debt and interest associated with foreclosure. |

| Borrowers get an excellent opportunity to reclaim ownership over their mortgaged property and save themselves from homelessness. | It helps borrowers to save their property by mending the default of the loan and keeping the ownership of the property. |

Right Of Redemption vs Right Of Foreclosure

Let us compare the two using the table below:

| Right of redemption | Right of foreclosure |

|---|---|

| The lender's right is to legally take possession of the defaulting borrower's property to recover their investment. | The lender exercises the right of foreclosure after the foreclosure process has been initiated. |

| Borrowers can exercise the right at any time before the foreclosure process is completed. | The right of redemption provides borrowers with the opportunity to avoid homelessness and retain ownership of the property. |

| The mention of "clever borrowers making handsome profits" is misleading and unrelated to the right of redemption. | The purpose of the right of foreclosure is for the lender to recover their capital by selling the mortgaged property. |

| The mention of lenders suffering due to below-market property prices is not directly related to the Right of Foreclosure, as market factors influence the sale price. | The right of redemption allows borrowers to avoid homelessness and retain ownership of the property. |

Frequently Asked Questions (FAQs)

Section 60 of the right of redemption refers to a specific provision in certain jurisdictions' laws that outlines the redemption rights of defaulting borrowers or debtors. It establishes the legal framework and conditions under which the right of redemption can be exercised.

The right of redemption provision provides several benefits. It allows defaulting borrowers or debtors to reclaim their assets, preventing permanent loss. It offers an opportunity to resolve financial difficulties and regain ownership. Additionally, it can help maintain stability in housing markets and provide a safety net for borrowers facing temporary hardships.

It is subject to certain limitations. These limitations can include specific time frames within which the redemption right must be exercised, the requirement to repay the full outstanding debt and associated costs, and the potential for the redemption right to be forfeited if the conditions are not met within the specified period. Furthermore, limitations vary depending on jurisdiction and applicable laws.