Table Of Contents

Revolving Fund Meaning

A revolving fund is a fund established for the specific purpose used to give loans to members or to be expended or invested for a specific purpose with the condition that repayments or benefits, or income from the fund may be used again for these purposes only. Also, legal status increases investors' faith that their money is in safe hands and cannot be misused.

Revolving fund loan is often used in developing countries to provide credit, i.e., money for willing borrowers for their business or other uses, and this concept is often used in the case of non-profit making organizations. It is necessary for the fund establishment authority to acquire legal status for clear terms and conditions between the fund establishment authority and its members.

Table of contents

Revolving Fund Explained

The revolving fund is established to carry out specific activities, and the primary advantage of this fund is it may be loaned or spent repeatedly. The basic idea behind that fund is a fund or money backup that remains available to finance organizations continuing activities. It circulates between the fund and the members.

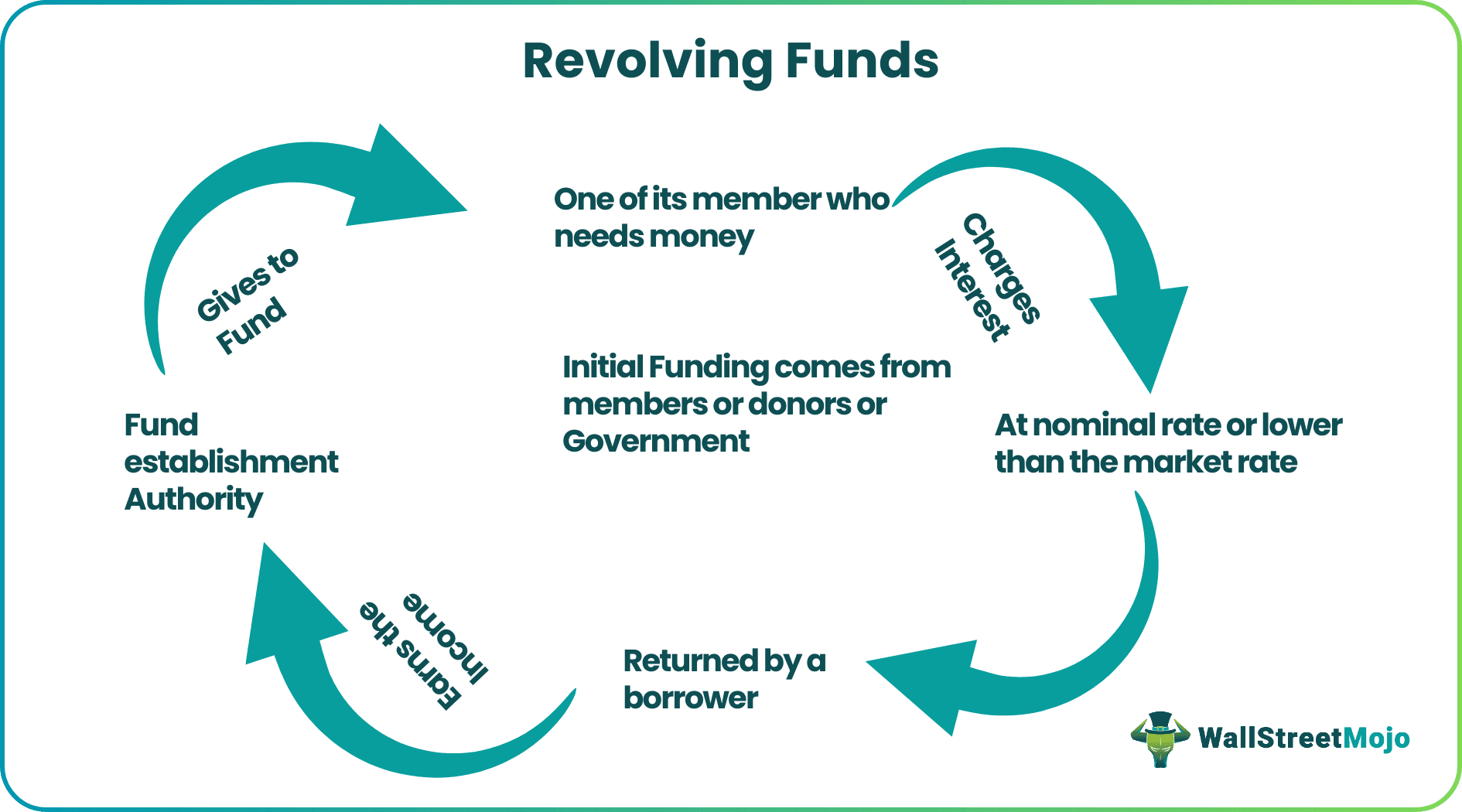

The initial contribution of this fund comes from its members, i.e., through initial fund investment in the case of Non-Governmental organizations. In the case of government revolving funds, it comes from the National (Central or State) Government, and in the case of Non-profit organizations, it comes from donors.

The initial loan of revolving funds came from its members, donors, Government, or a third party. Then, this fund is collectively given to one of its members who needs money where the fund establishment authority charges interest at a nominal rate or lower than the market rate. Those who had initial fund investments are also given interest on the money invested. Or, the fund can be invested in specific activities;, or it may be expended for a particular purpose, which benefits the long run.

Interest may be a nominal rate or lower than the market rate. At the year-end or after a specific period, the fund is returned by a borrower to a lender, i.e., fund establishment authority. Again, the fund is given to another willing borrower or invested or expended. In this way, rotation of funds takes place. Fund establishment authority earns the income from a fund, which is the difference between interest charged from the borrower and interest given to members, i.e., investors. That income is used for the welfare of members.

Management and Administration

Let us understand the coherence of government revolving funds or other such types with management and administration through the explanation below.

- As discussed above, legal recognition of funds increases investors' faith; hence it becomes necessary to legally recognize the fund and comply with all the norms relating to funding for maintaining legal status. But sometimes, some fund-establishing authorities do not legalize the fund, and that type of fund is called an informal revolving fund.

- Managing authorities manage it called a management team decided by members of the fund is a legally recognized fund. It is necessary to submit all the reports to the registered authority. Audit of the fund becomes essential, and submission of an audit report and other reports like contributors list, amount of contribution, receipts and payment statement, etc., are to be submitted to the registered authority of the fund. Annual accounts and annual reports of the fund are also to be sent to members of the fund.

- In the case of the informal revolving fund, it is not required to submit a report as it is not registered. But it is recommended that an audit be done and a report be sent to the members. However, the chances of bankruptcy by the borrower are high; hence no guarantee of money.

Structure

Let us understand the structure of a revolving fund loan through the discussion below.

- A revolving fund is established by its members who are users of funds for some specific purpose. Then members decide regarding the managing authority of the same along with deciding whether to recognize the fund or not legally.

- After that, members collect an initial fund investment, and then the fund is given to the member who needs and is willing to borrow at agreed terms. At the year-end, the interest is given to investors, and audited annual accounts are also sent to investors.

- In the case of the legal revolving fund, all statutory requirements must be complied with, and all documentation relating to funding is to be submitted to the registering authority.

Types

Each type of revolving fund loan serves distinct purposes, tailored to meet specific financial requirements within a business. Let us understand each of them to gauge which ne fits which situation better through the detailed explanation below.

- General Revolving Fund: Broadly applicable for various operational needs and expenses across different departments. It provides a high degree of flexibility, allowing funds to be allocated based on changing priorities and emerging needs.

- Project-Specific Revolving Fund: Designated for specific projects or initiatives, ensuring dedicated funding for targeted objectives. It enables better control and tracking of expenses related to particular projects, enhancing financial accountability.

- Emergency Revolving Fund: Reserved for unforeseen or urgent expenses, offering a financial cushion for emergencies. It ensures rapid access to funds in critical situations, preventing disruptions to essential operations.

- Capital Revolving Fund: Used for capital investments, allowing businesses to allocate funds for acquiring assets, expanding facilities, or making long-term strategic investments. It supports long-term planning by providing a stable source of capital for substantial business initiatives.

- Operational Revolving Fund: Geared toward covering routine operational expenses, supporting the smooth functioning of daily business activities. It also serves as working capital for ongoing operational needs, promoting financial stability.

Sustainability

The operations of the revolving fund are to be monitored periodically. It usually becomes self-sufficient after a specific period, but factors responsible for its failure are inflation, imbalance in interest income and expenditure, liabilities, hefty legal expenses, etc. The proper management of the fund and fast recovery of the cost generate a sense of ownership and financial viability and increase sustainability and faith.

Importance

Let us understand the importance of government revolving funds and other such sources through the points below.

- Revolving funds provide a flexible mechanism for capital management, allowing businesses to use and replenish funds as needed. This flexibility is particularly valuable for managing short-term operational needs and unforeseen expenses.

- Revolving funds serve as a reliable source of working capital, ensuring that companies have access to liquidity for day-to-day operations, such as inventory management, payroll, and other immediate financial requirements.

- By maintaining a revolving fund, businesses can better navigate periods of cash flow volatility. The availability of funds on a revolving basis helps bridge gaps in cash flow, preventing disruptions to essential business functions.

- Revolving funds promote capital efficiency by allowing companies to reuse the same pool of capital for various purposes. This minimizes the need for frequent external financing and reduces the cost associated with obtaining new funds.

- Businesses can swiftly seize opportunities, whether it's a strategic investment, acquisition, or responding to market trends, by having readily accessible funds through a revolving mechanism.

- Revolving funds offer an effective way to manage debt service obligations. Companies can use available funds to service debt when needed, optimizing interest expenses and ensuring timely repayments.

- In dynamic business environments, revolving funds provide the adaptability required to respond quickly to market changes, capitalizing on growth opportunities and navigating challenges effectively.

Revolving Fund Vs Petty Cash

Understanding the distinctions between revolving funds and petty cash is crucial for businesses to efficiently manage their financial resources, addressing both routine and more substantial operational needs. Let us do so through the comparison below.

Revolving Fund

- Primarily used for larger, ongoing business expenses and operational needs.

- Generally, involves a larger pool of funds, suitable for sustained operational requirements and periodic replenishment.

- Typically managed by financial or accounting departments, with established procedures for allocation, use, and replenishment.

- Offers flexibility in usage, allowing businesses to address various operational and strategic needs over time.

- Transactions and usage of revolving funds are often subject to detailed documentation and reporting for financial oversight.

Petty Cash

- Primarily used for small, day-to-day expenses and minor purchases.

- Involves a smaller amount of cash, often held in a physical petty cash box, and is meant for quick and minor transactions.

- Managed at the departmental level, usually by designated petty cash custodians who handle small transactions and maintain a limited amount of cash.

- Provides flexibility for immediate, low-value transactions without the need for formal approval processes.

- Transactions from petty cash are recorded with simplified documentation, often involving receipts and a petty cash log.

Recommended Articles

This article has been a guide to Revolving Fund and its meaning. Here we explain the structure, sustainability, and importance, and compare it with petty cash. You may learn more about financing from the following articles –