Table Of Contents

What Is Revenue Recognition Principle?

The revenue recognition principle is a generally accepted accounting principle (GAAP) that outlines the specific conditions under which the revenue is recognized or accounted for. Cash may be received earlier or later after the goods and services have been delivered to the customer and the revenue is recognized.

This principle clearly outlines when and how the revenue earned should be recognized and recorded in the books of accounts. It provides a uniform and useful framework that records the amount collected. Since earning revenue is the main aim of a business and is a benchmark to evaluate its performance, it should be recorded with reasonable certainty and help in improving comparability among companies.

Table of contents

Revenue Recognition Principle Explained

It is crucial to understand the revenue recognition principle and properly account for it. The accrual principle of revenue recognition in accounting aids in understanding the actual level of economic activity within a business. The deferred principle of accounting results in a correct reporting of assets and liabilities and guards against treating unearned income as an asset. It is crucial to understand the revenue recognition principle in accounting and properly account for the same.

It would primarily result in two types of revenue recognition principles: the Accrued revenue and the Deferred revenue accounts.

#1 - Accrued Principle of Revenue Recognition

source: Colgate SEC Filings

Under accrual accounting, revenues need to be recorded in the same accounting period it has been earned, irrespective of the timings of the related cash flows from that transaction.

Suppose the seller is doubtful about receiving the amount from the customer. In that case, he will recognize an allowance for doubtful accounts in the amount by which the customer will likely default on the payment.

#2 - Deferred Principle of Revenue Recognition

source: Salesforce SEC Filings

Deferred revenue refers to the payments received in advance for the services yet not rendered or goods yet not delivered. The deferred revenue classifies as an asset once the company delivers the services or goods to the customer. If a company receives advance payment, it classifies it as a liability, as the service is not yet performed and needs to be delivered in the future.

Salesforce.com reported its deferred income under the current liability section. It is $7,094,705 in FY2018 and $5,542,802 in FY2017.

Features

The five essential criteria for identifying the phenomenon about revenue recognition on the sale of goods as provided by IFRS is as follows-

- Risks and rewards have been transferred from the seller to the buyer.

- The seller does not have any control over the goods sold.

- The collection of payment from the goods and services is reasonably assured.

- The amount of revenue can be reasonably measured.

- Costs of earning the revenue can be reasonably measured.

#1 - Performance

Conditions (1) and (2) refer to performance. It occurs when the seller has completed the transaction as required for him to be given the payment.

#2 - Collectability

Condition (3) refers to Collectability. The seller must have a reasonable expectation that he will be paid for the performance. An allowance account must be maintained if the seller is not fully assured of receiving the payment.

#3 - Measurability

Conditions (4) and (5) refer to Measurability. The seller must match the revenues to the expenses as per the matching principle concept.

Revenue vs Income Explained in Video

Examples

Let us understand the concept of revenue recognition principle in accounting with the help of some suitable examples, as given below:

Example#1

A cleaning company named XYZ Ltd. has committed to providing services to a customer. The company accepted the prepayment of its monthly fee of Rs.300 in advance for a full year. This advance fee is considered as deferred revenue expenditure and should be treated as a liability since the service is yet to be performed by the cleaning company. The advance fee received, which is effectively unearned, is converted to an asset only after the cleaning company performs the monthly service as promised to the customer.

Other examples are advance rent payments, annual prepayment for software use, prepaid insurance, advance payment for newspaper subscriptions, etc.

Example#2

LMN Ltd. bills Rs.100 per hour for the service rendered. In January 2017, it performed 6000 hours of consulting, thus generating revenue of Rs.6,00,000. The company decided to invoice the clients in February 2017.

The company will have to record Rs.6,00,000 as accrued revenue on the balance sheet of January 2017 and Rs.6,00,000 in revenue in the January income statement. Thus, it recorded that the company earned revenue in January though it has not received the payment for the same.

The company will convert Rs.6,00,000 of accrued revenue to accounts receivable once the invoice is sent. The accounts receivable will, in turn, be converted to cash when the payment is received from the respective customer.

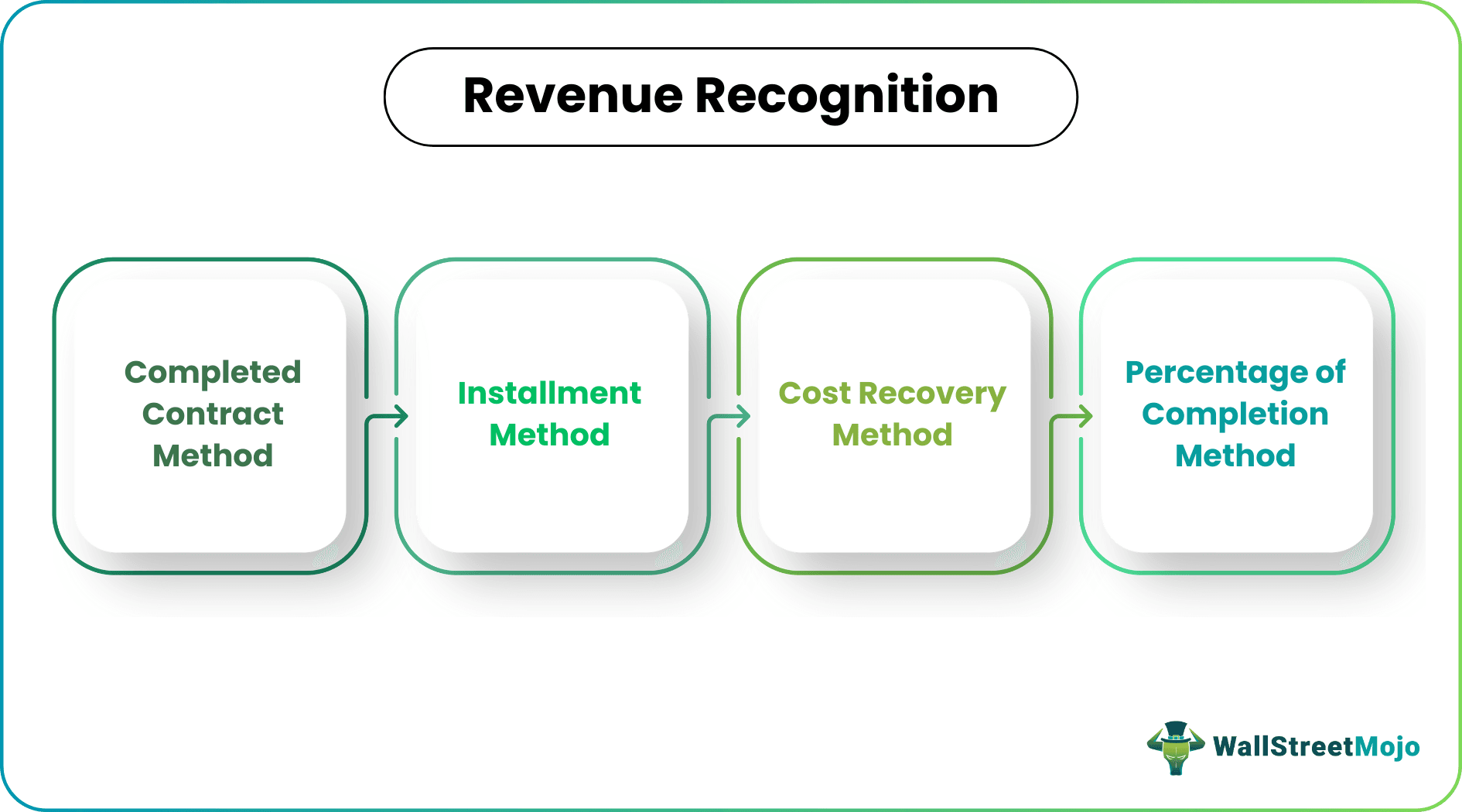

Methods

The methods for revenue recognition in an income statement have been explained.

1) - Completed Contract Method

Under this method, the revenue associated with a transaction is recognized only after completing the transaction. This method is generally used in case of uncertainty concerning the collection of funds from the client.

2) - Installment Method

The seller accounts for the transaction by using the installment method when the customer is allowed to pay for the product/service over several years.

3) - Cost Recovery Method

As per the cost recovery method, the revenue recognition is only done after the cost factor of the sale has been paid by the customer in cash.

4) - Percentage of Completion Method

The seller can recognize some gain or loss related to the deal in every accounting period in which the deal continues to be in force. This method is usually adopted while handling long-term projects.

Following the revenue recognition principle in GAAP and IFRS strictly is very crucial in order to present a true and fair view of the financial statements. This is so that stakeholders can identify the financial health of the business properly and make investment decisions that affect the future expansion and growth of the company. Companies can streamline compliance and simplify complex accounting tasks by adopting specialized revenue recognition software that automates these processes. Also, raise the GST invoice as per the details sent in the mail trail.

Steps

The revenue recognition principle in GAAP and IFRS followed in the modern industrial era is very updated and transparent in nature. It helps to easily compare the financial statements of peer companies by following a few standardized steps as given below. Let us try to understand the same.

Step#1

It is necessary to identify and agree to the terms and conditions of contact related to transfer of goods and services. Both the vendor and the client must agree to the terms specified in the contract regarding delivery and payment collection of the same and abide by the rules and face legal consequences in case the consequences are not met. The contracts are typically a written document by may sometimes be verbally specified, depending on the relationship between the client and vendor.

Step#2

This step involves identifying the products or services that are transacted. Every agreement will revolve round some specific product or service that the parties will deal with in the process.

Step#3

Next, it is necessary to identify the prices at which the goods will be sold. These prices in the core revenue recognition principle are not only the price of product but will also include any discount, sales promotion incentives, sales return policies, any extra fees, penalty for delay in payment, etc. Such prices are fixed after analysis of many external and internal factors like current market price of competitors, production cost, product demand, customer base, future expansion plans, etc.

Step#4

In this step, the selling price is clearly allocated to different parts of the contractual obligation so as to bring about a clarity in the price levels of the entire product or service.

Step#5

Finally the required revenue is recognized when the transaction is complete and the amount for payment is realized by the seller. Both the parties are satisfied with meeting the transaction obligations. The fund received in recorded in the books of accounts following the accounting rules for transparency, accountability and information for stakeholders.

Thus, the above are the steps followed in the core revenue recognition principle so that every business can record details of every transaction properly and refer to them for future purposes.

Revenue Recognition Principal Vs Revenue Recognition Agent

The above are two different concepts followed in the revenue accounting process. However, there are some differences between them as follows.

- The former deals with the different criterias and guidelines a business follows to recognize the revenue earned in the financial statements, whereas the latter deals with how an entity acts as a agent to facilitate a transaction of purchase and sale.

- In the former, both the buyer and seller has complete control over the products and services bought and sold. But in case of the latter, the agent does not have any control over the goods.

- In case of the former, the buyer or seller are the main parties and in case of the latter, the agent is just an intermediary.

- For the former, the entire amount transacted in recorded in the financial statements but in case of the latter, the value recorded in the books has been after deduction of the commission charged by the agent.

Therefore, it is important to understand whether a company is acting as a principal or an agent while facilitating any transaction because this will decide the amount that is entered in the accounting books and displayed in the financial statements. This in turn will affect the perception of stakeholders and decisions of management.

Recommended Articles

This article has been a guide to what is Revenue Recognition Principle. We explain it with examples, differences with revenue recognition agent, features & steps. You may learn more about accounting from the following articles –