Table Of Contents

Revenue Expenditure Definition

Revenue expenditure refers to those expenditures which are incurred during normal business operation by the company, the benefit of which will be received in the same period and the example of which includes rent expenses, utility expenses, salary expenses, insurance expenses, commission expenses, manufacturing expenses, legal expenses, postage and printing expenses, etc.

They help in running the normal business operations smoothly and contribute to profitability and efficiency. Even though they do not directly increase asset value, they are useful in providing incentives to utilization of resources and assets so that the business runs effectively with minimum wastage and maximum cost control. However, its benefit is received within one accounting period.

Table of contents

Revenue Expenditure Explained

Revenue expenditure is the expenditure incurred by the company during its ordinary business operations. Here the benefit will also be received in the same accounting period in which expenses were incurred, and it shows as the expense in the company's income statement. Generally, such expenditures will be divided into two categories, i.e., expenses for maintenance of revenue-generating assets and the expenses on things used for generating the business's revenue.

This business uses the accounting principle of matching to link the expense incurred with the revenues generated in the same reporting period. It includes the spending by the company on the expense, which will match with the reported revenues on the income statement for the current year. Revenue expenditure in accounting is charged at the expense in the income statement as soon as the cost is incurred. With this concept, the income statement results will give more accurate results to the user of the company's income statement.

Revenue expenditure in accounting is the sum of the expense that the business incurs in the production of goods and services, which helps the company's revenue generation in an accounting period.

- There are primarily two types – one is related to the cost of sales, and the other is related to Opex. Cost of sale is the expense of acquiring goods or services that need to be sold in the market, and operating expense is an expense that needs to be done to run a business and its operations properly.

- These expenses are to be recorded in the same period when revenue is generated on produced of goods or services (matching principle).

Types

They are of two types revenue expenditure budget-

- Direct Expense

- Indirect Expense

#1- Direct Expense

The direct expense is the expense that occurs from the production of raw material to final goods and services. The direct expense example is wages of labor, shipping cost, power, electricity bill cost, rent, commission, legal expense, etc.

#2- Indirect Expense

Indirect expense occurs indirectly; they are generated in connection with selling goods and services and their distribution. Indirect expense examples are machinery, depreciation, wages, etc.

Revenue vs Income Explained in Video

Features

Some important features of such revenue expenditure of government or corporates as follows:

- Short period – These expenses are related to a short period, which is usually a year or one accounting period. The benefit of them is derived within that period.

- General expenses – They are general in nature and are of lesser value. They help in running the daily operations of the company smoothly and make work easier.

- No addition to asset – Since they are of small amount and does not involve purchase of heavy assets, there is no addition to the value of total assets of the organization. However, they help in working of the fixed assets smoothly.

- Recurring – The organization will incur such expenses every year, quarter or month. This means that they are recurring in nature, like wages, salaries, various bill payments related to daily business operations.

- Contribute to profitability – These revenue expenditure budget help in making the work condition, performance of resources and standard of work better. Therefore there is an increase in profitability of the business.

Examples

Let us understand the concept revenue expenditure of government or corporates with the help of some suitable examples.

Example#1

Revenue expenses are expenses incurred by the business in the daily working of the business, and the effect of which will completely be utilized within the current accounting year in which it is incurred. These costs are recurring in nature and do not form part of the fixed asset cost. Thus they are shown in the income statement of the year in which they are incurred.

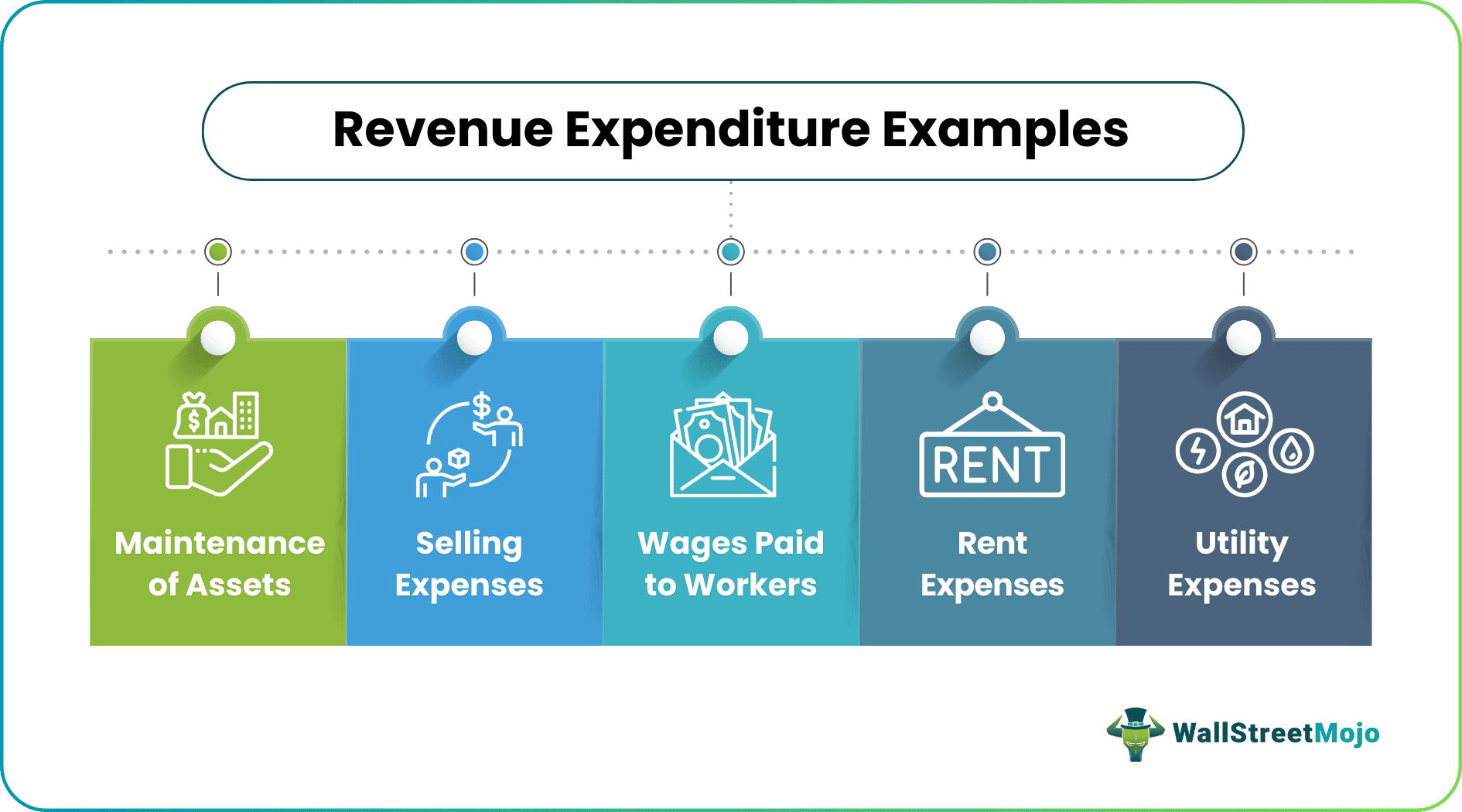

- Repair and Maintenance of the Assets - The companies plan revenue expenditure incurred on the repairs and maintenance of the assets generating the revenues are considered as the revenue expenditure as expenses are incurred for supporting the business's current operations and do not affect the asset's life.

- Wages paid to workers of the Factory - The wages paid to the workers are required to work for the company and run the business to generate revenues. So, these are considered to be revenue expenditures.

- Utility Expenses - Utility expenses such as expenses incurred on phone bills, water bills, electricity bills, etc., are required to be spent by the company to continue its business operation and generate revenue. Without these resources, the working of the businesses cannot effectively take place and thus are part of revenue expenditures.

- Selling Expenses - Selling expenses are required for selling the products timely. It is used to promote and market the products to the customers. As it is spent on increasing the business sales, they form part of the revenue expenditure.

- Rent Expense - The expenses incurred in renting the premises on which the business operates or renting the other materials will be considered part of revenue expenditure as they are essential for running the business.

- Other Expenses - Any other expenses related to generating the revenue of the business or maintenance of revenue-generating assets are to be considered the revenue expense.

Example#2

Consider a company XYZ Ltd manufacturing and selling the packets of the pen. The company spends each year on various expenditures such as pens manufacturing, salaries to employees, Utility bills, repairs and maintenance, acquisition of the assets, etc. It is not sure about which expenditure to be treated as revenue expenditure.

- The amount spent every year required for generating revenue or maintaining revenue-generating assets will be considered revenue expenditures. Additionally, expenses incurred to acquire any of the assets or improve the capacity or life of the assets will be treated as the CAPEX.

- In the present case, the amount spent every year for making pens and packing them for employees, Utility bills, wages to workers, insurance, rent, etc., will be categorized as the revenue expenditure.

- Apart from this, any repair cost on machines used to manufacture pens will also be considered revenue expenditure.

- On the other hand, any amount the company spends on acquiring the assets or upgrading the machinery used for the manufacturing of the pens for increasing capacity, life or quality, etc., will be treated as the company's capital expenditure.

Example#3

Company ABC Ltd. started the business of manufacturing and selling bakery items in the market. For that purpose, it buys a machine so that the bakery items can be produced. The company's owner is arguing that it should be treated as revenue Expenditure. How should it be treated?

- In the present case, the initial purchase cost of the machinery and installation costs will be classified by the business as the capital expenditure because the benefit of the machinery will be derived by the business for the several accounting periods and not in a single accounting period.

- However, any subsequent cost incurred on the company's repair and maintenance will be considered the revenue expenditure. It is because when the cost of repair and maintenance incurs, neither increases the earning capacity of the machine.

- The machine will be going to produce the same quantity of the bakery products as it used to do earlier when first it was put to use by the business, nor will it increase the life expectancy of the machinery. I.e., the life of the machinery will remain the same as it was at the start, and the cost is incurred just for the maintenance of the asset. So, the initial purchase of the machinery will be considered a capital expenditure and not a revenue expense.

Revenue Expenditure Vs Capital Expenditure

Both the above financial concepts are crucial parts of financial accounting and preparation of financial statements. Therefore, it is important to understand the differences between the two. Let us study them in details.

- The former refers to the daily operational costs or expenses that the business incurs while the latter is the cost incurred for maintain the heavy assets, or purchase, upgradation of fixed assets that are of high value.

- The former will give benefit for a short period of time which is usually for one accounting period and the latter gives benefit for an extended period of time, which is more than a year.

- Some examples of the former include rent, wages, salaries, electricity bills, stationery cost, travel expenditure, etc. But the latter include items like purchase or upgradation of machinery, vehicles, plants, building or installation of software that will make the work easier and less time consuming, etc.

- The former is fully charged and shown in the year in which it is incurred and appears in the profit and loss statement, but the latter is shown in the balance sheet upto the value that is depreciated within one year and the entire cost is spread over its lifetime.

- The former does not add to the value of existing assets of the organization. It just helps in running the operations of the business smoothly and creating a workplace that can meet the proper standards. But the latter increases the asset value of the company and are investments that are of high value with return expectations over number of years in future.

Therefore, the above are some important differences of both the financial concepts. It is necessary for analysts, investors and other stakeholders to understand and plan revenue expenditure in-depth so that the concerned items can be easily identified from the financial statements to evaluate the current financial position of the entity and make investment decisions accordingly.

Recommended Articles

This article has been a guide to Revenue Expenditure and its definition. We explain the differences with capital expenditure, examples, types and features. You can learn more about accounting from the following articles –