Table Of Contents

Return Inward Meaning

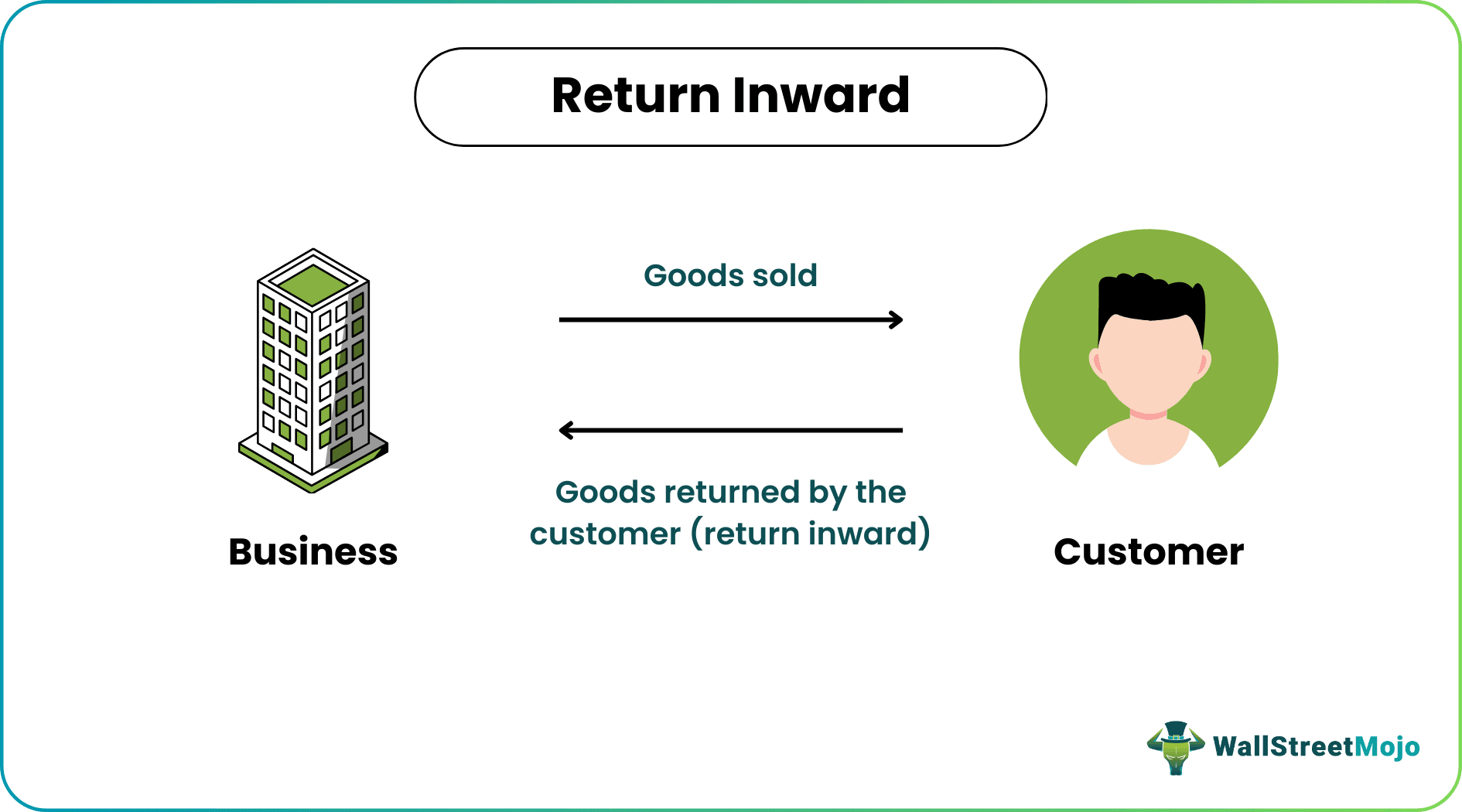

Return Inward, also known as sales return, refers to the goods returned to the business entity when the customers find that the goods delivered did not meet their expectations and, therefore, were unsatisfactory. It directly affects the operating activities of the business.

Hence, the returned goods are recorded in the Return inward journal from the copies of the credit note sent to the customer who returned goods or was overcharged. Various software technologies have been introduced to record the return inward. This is to avoid various errors coming up in the report. But there are a few elements essential for writing return inward such as date, details, identification no, related identification nos about the goods which need to be taken care of.

Table of contents

Return Inward Explained

The concept of return inward, also known as sales return, is the process in which the customers return the goods or services they have purchased from a company. This may be due to the product not being able to meet their expectations because they are either damaged or defective or does not match the actual product description due to any other reason.

There is a fall in the sales revenue because the sale is reversed or adjusted to record for return inward in trial balance. In such case, the customer may want to return the item and get refunded or exchange it with something similar but more useful.

It is necessary to note the following rules that are strictly followed in such situations.

In the Journal:

- The records are made in chronological order, with the name of the customer and the number of goods the customer has returned.

- Entries are recorded at a list price less than any discount provided.

- Entries are supported by credit notes which are sent to the customer.

However, it is necessary to accurately record such transactions in the books as soon as they happen; otherwise, the accurate financial condition will not be reflected. Proper recording of sales return will also ensure that the inventory level is managed properly. This is also useful in order to assess how frequently the sold products or services are returned.

Based on the above information, the business can analyze the various reasons for customer dissatisfaction and take steps to control the problems or identify the areas where there is discrepancy during production or delivery. This will lead to better customer service, and increase the overall earnings of the business.

Journal Entries

When the return inward or sales return occurs, the business will compulsorily have to record the transaction in the books to reverse the sale. However, depending on the accounting system followed, the entries are as follows:

The first step is to do the revenue reversal in the account statement. For that there are two possible situations.

If the transaction is done in cash, then:

Return Inward or Sales Return A/c Debit

To Cash A/c

If the transaction is done on credit, then:

Return Inward or Sales Return A/c Debit

To Sales A/c

Next, the business has to check whether the inventory is still in a saleable condition or not. If they can still be sold, then the business will put them in the inventory back once again for resale. In that case, the inventory will increase, and the cost of goods sold will come down. The entry will be:

Inventory A/c Debit

To Cost Of Goods Sold A/c.

Thus, the above are the entries for recording the return inward in trial balance and financial statements.

Example

Below is the example of Return Inward -

The below example can be understood concerning the total amount generated in the "Return Inward Journal," which is transferred to "Trading Account Format." Various sales entries are accounted for a month (time duration differs from organization to organization) and are noted serially.

Return of journal monthly total is transferred to less return in “Trading Account Format.”

- Accountability of these return inward in final accounts becomes useful as it is a mere addition to the amount that has been undertaken as there is a return in sales.

- It is shown on the credit side of the “Trading Account Format.” Just below the sales, the total amount of return calculated from the “Return Inward Journal” is put into place.

- When return inward is more, this indicates to the company about the related product. These issues must be addressed immediately, affecting the company's sales.

Advantages

Return inward is sales return and is an important element while preparing a trading account. It helps the management decide the price of the product. One can decide whether or not to continue with a required product.

- Each sales returns need to be debited from the sales return account.

- Value, quantity, and reasons for sales returns can all be known from the sales return book.

- Also, the total amount of sales returns can be obtained.

- Clerical work can be reduced by using a sales return book.

- Errors committed if any while writing the sales return book or return inward book is normally detected at the time of posting to the sales return account.

- As sales return is recorded serially in the sales return book, particulars of any sales return on any day can be located in the sales return book.

Disadvantages

It becomes very important to include return inward in final accounts. If projected without return inward, the total sales amount would reflect the incorrect amount in the accounting. Still, the entire entity is carried in a separate journal, because of which it becomes very important to carefully note all the values in the returned journal under the different headings and update them regularly.

Return Inward Vs Return Outward

Both the above financial terms are two types of accounting concepts that are widely used in any business. But there are some basic differences between them. Let us try to identify the differences as given below:

- The return inward is sales return and the latter is also known as purchase return in the accounting process.

- The former happens when the customer returns the goods or services that the company has sold to them and the latter occurs when the vendor or the return the goods and services purchased by them from the supplier.

- The former happens when the customer is dissatisfied because the product does not meet their expectation due to damage, defects, or any other valid reason. The latter occurs when the business is not satisfied with the products received from supplier and has to return it back to them.

- The return inward results in reduction in sales of the business which affects profit if the goods are not in a condition to be sold once again. The return outward results in fall in cost of goods sold and inventory of the business.

- The accounting entries are different in both the cases. For the former, the sales return is debit and cash or sales account is credited. For the latter, the cash account is debited and purchase return or return outward is credited.

Thus, it is necessary to understand both concepts very clearly and make the accounting entries immediately in the books so that the financial statements reflect a correct view of the condition of the business.

Recommended Articles

This has been a guide to Return Inward and its meaning. We explain the differences with return outward along with journal entries, example & advantages. You can learn more about excel modeling from the following articles –