Table Of Contents

Residual Interest Definition

Residual interest, a fundamental financial concept, pertains to the accruing interest on various interest-bearing accounts. Commonly encountered in credit cards, loans, lines of credit, mortgages, and structured credit investments, residual interest is crucial in maintaining a fair and accurate accounting of interest charges.

Beyond its accounting function, it is designed to provide financial incentives for borrowers to manage their debt responsibly. This dynamic plays a significant role in the broader financial system, impacting borrowers, lenders, investors, and regulators alike. A comprehensive understanding of this interest is essential for responsible borrowing, informed investing, and ensuring the overall stability of the financial landscape.

Table of contents

- Residual Interest Definition

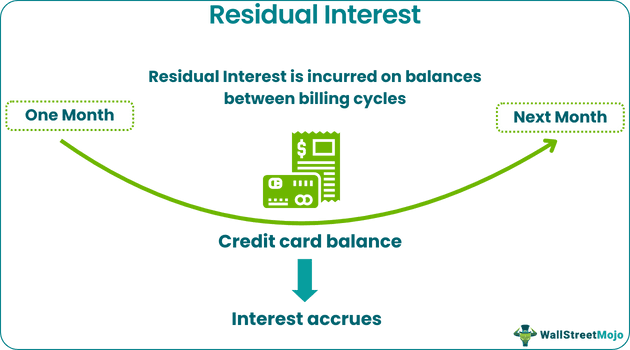

- Residual interest on credit cards, also known as trailing interest, is the interest charged on the remaining balance of a credit card after the statement is issued.

- To estimate it, multiply the daily interest rate by the outstanding balance and then by the number of days the interest accrues.

- To avoid it, pay the full monthly balance, utilize the grace period, leverage 0% APR offers, set up automatic payments, and stay informed about the account's terms and conditions. By being proactive and responsible, one can eliminate this hidden cost.

Residual Interest Explained

Residual interest, also known as trailing interest, accrues on a balance during the period between the conclusion of one billing cycle and the date the card issuer receives a payment. It introduces an often overlooked cost in the case of credit card usage. The intricacy arises from the daily accumulation of interest on revolving credit accounts, calculated based on a daily interest rate derived from the annual percentage rate (APR). Even if users diligently pay the full balance reflected on their monthly statements, interest accumulates on the previous month's charges until the credit card issuer receives and processes the payment.

Understanding the mechanics of this interest is paramount for users to make informed decisions about their credit card usage and payment timing. While minimum payments might meet immediate credit card agreement requirements, they can lead to substantial trailing interest charges over time. To optimize financial well-being and mitigate these hidden costs, paying the credit card balance in full each month before the payment due date is highly recommended.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

How To Calculate?

While credit card companies automatically calculate residual interest, individuals can estimate this cost themselves. This helps them to make informed decisions about their credit card usage and manage their debt effectively.

Residual Interest Calculation:

- Gather information: Annual Percentage Rate (APR) on the credit card statement or online.

- Determine Daily Interest Rate: Divide APR by the number of days in a year.

- Estimate Daily Interest: Multiply the daily interest rate by the current balance.

- Calculate Accrual Period: Subtract the payment date from the current date to determine the number of days interest accrues.

- Estimate Residual Interest: Multiply the daily interest by the number of days in the accrual period.

While this calculation provides an approximation, understanding the process allows individuals to estimate potential residual interest charges and make informed decisions about their credit card usage. By actively managing their debt and striving to pay their balances in full, they can minimize these charges and achieve their financial goals.

Examples

Let us look at some examples to understand the concept better -

Example #1

Nelnet has acquired a residual interest in federal student loans totaling $1.9 billion from a Greystone & Co. affiliate. This transaction involves obtaining rights to the residual interest in GCO Education Loan Funding Trust-I by acquiring notes issued by GCO Student Loan Interest Margin Securities Trust-I. Nelnet anticipates an immediate positive impact on its base net income following the purchase.

Example #2

Imagine Mary, a responsible credit card user who consistently pays her monthly bill on time. To her surprise, she noticed a residual interest charge on her next statement despite settling the stated amount promptly. Mary discovers that the residual interest arises from the daily accrual of interest on her previous month's balance, calculated based on her credit card's annual percentage rate (APR).

For instance, if Mary's APR is 18%, her daily interest rate would be approximately 0.0493% (18% divided by 365 days). If she had a $1,000 balance from the previous month, the daily interest would be about $0.49. Over 30 days, this amounts to $14.70, explaining the residual interest she observes.

How To Avoid?

The strategies to avoid residual interest charges are the following:

- Many credit cards offer a grace period between the billing cycle's end and the due date. Pay the statement balance in full before this date to avoid residual interest. Remember that missing payments or carrying a balance can eliminate the grace period, resulting in interest accumulation.

- Regularly check the credit card statements and understand the terms related to interest charges. Knowing the account's policies empowers one to make informed decisions and manage their credit card effectively.

- Some credit cards provide 0% APR on balance transfers during introductory periods. Use this offer to pay down the debt without incurring extra interest for a specified time, saving money on residual interest charges.

- One should set up automatic payments to ensure that they never miss a deadline. This prevents late fees and stops the accrual of residual interest. It's a hassle-free way to manage the payments consistently and save money.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

No, it is not a liability. It represents the interest accrues on an outstanding balance commonly associated with credit cards. While liabilities often refer to financial obligations, residual interest is an ongoing cost calculated on the remaining balance, not a standalone financial obligation.

Interest generally refers to the cost of borrowing money, while residual interest specifically relates to the lingering interest on a credit card's remaining balance after the statement is issued. Residual interest captures the continuing accrual of interest on a revolving credit account during the period between billing cycles.

This interest is not a separate line item on a balance sheet. Instead, it's a component of the total interest expense incurred by a borrower. In financial statements, interest expenses reflect the overall cost of borrowing, encompassing both regular interest charges and any residual interest accumulating on outstanding balances.

Recommended Articles

This article has been a guide to Residual Interest and its definition. Here, we explain how to calculate & avoid it, and its examples. You may also find some useful articles here -