Table Of Contents

What Is Remote Deposit Capture?

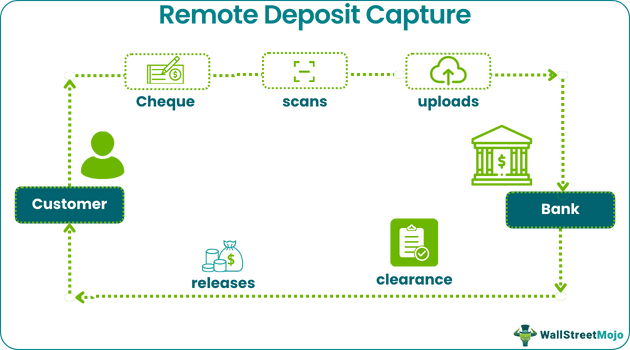

Remote Deposit Capture (RDC) service is an electronic mode of clearing checks by scanning and uploading them into digital format. The main purpose of this mode is to enable faster check clearance instead of traditional, age-old methods via banks.

The mobile remote deposit capture is a perfect alternative to clear checks in remote places without banks. It reduces costs and fosters quick processing of the checks. In addition, it provides convenience to both banks and customers. However, there are various security challenges possessed by this RDC system.

Table of contents

- What Is Remote Deposit Capture?

- Remote Deposit Capture (also RDC) is a disruptive technology that allows customers to scan, check images, upload them online, and process the clearance.

- Here, there is no need to visit the bank's physical branch for check clearance. It can happen remotely. The only criteria are an internet connection, device, server, and scanner.

- The "Checks 21 Act" passed in 2004 during the federal legislature remarks the beginning of the RDC program in the United States.

- However, there can be chances of check duplication or poor image quality for errors made by humans or applications.

How Does Remote Deposit Capture Work?

Remote Deposit Capture is a system that allows checking clearance electronically via digital images. Thus, it becomes easy for customers to clear their checks in any part of the globe. The only requirement for this system is a scanner, computer, and internet connection. Banks mostly provide this service to business owners as they have a pile of checks to deposit rather than individuals. However, individuals and other organizations can also have access to this service.

In the traditional mode of clearance, the depositor (company) used to collect checks from the customers. However, the process of RDC differs from the traditional system. Once the owner receives the checks, the respective accounting entry is made in the accounts receivable ledger. Later, the checks must be digitally scanned by the owner. Here, the scanning must happen by capturing both sides of the check. Next, the digital images must be uploaded in a digital deposit. Once uploaded, they must transmit these images to the RDC provider (or financial institution) via FTP (File Transfer Protocol). However, a secure internet connection is a must for it to work. Plus, the encrypted file must be 128-bit.

As soon as the bank receives the images, they will provide the ACH (automated clearing house) decision. However, the banks must adhere to the NACHA (National Automated Clearing House Association) and remote deposit capture regulations. Later, the bank will send a carbon copy to the clearing house. As a result, the depositor will receive funds in their account.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Examples

Let us look at the examples of remote deposit capture market for a better understanding of the concept:

Example #1

Suppose Tensen owns a business that is engaged in the service industry. As customers subscribe to their services, they earn revenue from them. Thus, the accounts team collects and deposits them in the bank for clearance. However, in recent years, the RDC service has bloomed.

Therefore, Tensen decided to pair for this service. As a result, the accumulated checks were scanned and uploaded to the bank's site. Later, in a few hours, the bank processed the data and images, cross-checked the information, and sent it to the clearance house. Thus, the checks cleared, and funds were released to Tensen's business account.

Example #2

Another example is the increased scrutiny of security vulnerabilities in the payments processing sector involving remote deposit capture (RDC). U.S. bank regulators are focusing on this area due to concerns about potential money laundering activities by drug cartels and terrorists. This heightened attention has led banks such as Citigroup and HSBC to invest substantially in technology and staff to detect suspicious transactions in electronic check processing through RDC.

The primary worry is that RDC, which enables the electronic transmission of check images, could be exploited for illicit purposes. For instance, drug cartels might utilize exchange houses in Mexico to scan checks, transmit them to U.S. accounts, and channel the funds through legitimate businesses. These regulatory pressures are causing compliance costs to rise for banks.

Benefits

Let us look at the benefits of the remote deposit capture to the customers and business owners:

- Lower Costs: Barely any costs are incurred compared to the traditional system. The basic requirements for this service include an internet connection, server, and system to upload the files. However, the prior method wanted the depositor to travel to the bank to deposit the checks.

- Saves Time: As the check clearance occurs online, there is no need to visit the bank. Therefore, time is saved, and the depositor can work on other projects simultaneously.

- Increased Security: RDC provides the depositors with the ultimate security during clearance. Since the transfer occurs electronically, it gets transmitted in encrypted form. Therefore, there are no chances of theft compared to physical transfers. In the latter case, there are possibilities of misplacements of the checks.

- Flexibility: Customers can perform RDC anytime as it is available beyond the bank timings. Some banks have scheduled availability timings till 10 p.m. in their respective time zones. Compared to normal deposits, business owners have the flexibility to operate easily here.

- Easy Accessibility To Funds: As the process happens quickly, the customer can easily get the check amount in their bank account. Thus, the funds can be, thus, disbursed to the suppliers and employees.

Remote Deposit Capture vs Image Cash Letter

Although RDC and image cash letter (ICL) follow a similar process, they have different functions to perform. So, let us look at the differences between them:

| Basis | Remote Deposit Capture | Image Cash Letter |

|---|---|---|

| Meaning | RDC technology allows customers to scan their checks and enable faster clearance. | An image cash letter is a file format that transmits or transfers the check data (digital images) between banks. |

| Objective | To ensure quick check clearance through electronic methods. | To allow electronic transfers between banks for clearance. |

| Process | The customer uploads the check's image and sends it to the bank. | Here, the bank will form a digital image of the check and other data and forward it to the other bank. |

| Parties involved | Here, depositors and banks are the major players. The former includes businesses, organizations, and individuals. | In this case, the process occurs between banks. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Remote Deposit Capture (RDC) offers convenience by allowing you to deposit checks from anywhere, eliminating the need to visit a physical bank branch. It saves time, reduces costs associated with travel, and accelerates check clearance. Businesses, in particular, benefit from streamlined operations and faster access to funds.

RDC can carry some risks, primarily related to security. Ensuring a secure internet connection and adherence to encryption standards is crucial to minimize risks. Additionally, there is a potential for errors like check duplication or poor image quality, which can lead to processing issues.

Remote Deposit Capture (RDC) is not considered an Electronic Funds Transfer (EFT). While both involve electronic transactions, RDC specifically refers to the electronic capture and deposit of paper checks into a bank account. EFTs encompass a broader range of electronic financial transactions, including account transfers, card payments, etc.

Recommended Articles

This article has been a guide to what is Remote Deposit Capture. Here, we explain its examples, benefits, and compare it with image cash letter. You may also find some useful articles here -