Table Of Contents

Reinsurer Definition

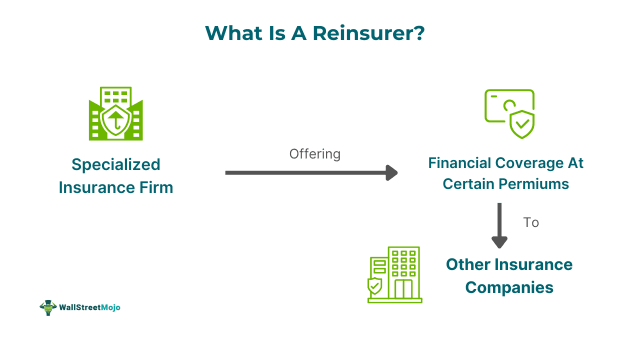

A reinsurer is a specialized insurance firm that provides necessary coverage to other insurance companies called cedents after charging premiums. It limits liability on particular risks, stabilizes loss experience, protects against calamities, and increases insurers' capability to provide a higher quantum of coverage limits.

Reinsurers achieve their aims by taking responsibility for a portion of the risk from insurers, reciprocating by charging a portion of premiums. This helps insurers reduce risk exposure, free up capital, and expand their underwriting capability to better serve their policyholders through financial stability and risk management in the insurance sector.

Key Takeaways

- A reinsurer is a unique insurance company that supplies essential financial coverage to other insurance firms by getting premiums.

- Some important functions comprise restricting liability for guarding against natural disasters, enhancing insurers' capacity to offer larger coverage levels, and stabilizing loss experience and certain risks.

- It helps facilitate claims settlement, provides expertise in underwriting and pricing policies, aids insurers in managing risk, increases financial stability, and reduces costs.

- It protects insurers against extreme losses by transferring or sharing risk, while insurers protect the finances of businesses or individuals against sudden life, health, or business losses.

Reinsurer Explained

A reinsurer is a firm offering financial safety to insurers after getting premiums on the risks they cover so that insurers can enlarge their business and handle more risks despite their weak balance sheet. Reinsurance firms permit insurers to stay solvent by recovering all or some amount of payment made to claimants. Hence, it decreases the net liability on single risks and offers catastrophe protection from multiple or large losses. It also increases the underwriting capacity of insurers by freeing up their capital.

It gives increased security concerning solvency and equity by enhancing their capability to face significant financial events. It also paves the way for insurers to underwrite huge risk volume without exceedingly raising their administrative costs. It has been used in the insurance industry for many reasons, like stabilizing underwriting outcomes, acquiring expertise, spreading risk, expanding capacity, and obtaining catastrophe protection and financing.

It impacts the financial world in real time because it invests in financial markets and offers the required capital to the industry. It has a global impact on industries by helping governments, insurers, and society holistically consider the existing risky economic landscape. Moreover, Reinsurance Group of America, or RGA reinsurer, is one of the largest reinsurance companies and acts as a treaty and captive reinsurer in the United States.

Role

It plays multiple roles in various sectors, as mentioned below:

- It aids insurers in managing risk by sharing and spreading risks throughout different parties.

- Insurance companies increase their capacity and financial stability with the help of risk absorption capabilities and extra financial resources.

- It provides essential help in claims settlement and loss recovery, allowing policyholders to receive compensation for the worst losses.

- It becomes vital to provide expertise in claim risk assessment, underwriting expertise, pricing policies, and determining correct coverage levels.

- They provide the necessary risk absorption capabilities and additional financial resources to help insurers meet solvency and regulatory requirements.

- It also supplements and adds newer technological advancements, such as artificial intelligence and big data analytics, to drive innovation, improve underwriting accuracy, and enhance claims management.

- They augment insurers' capabilities of risk mitigation and management through risk transfer, risk evaluation, and risk handling means.

- They provide financial stability and the ability to adapt to market volatility and risk management, which in turn leads to insurers' stability.

- It also contributes to the global economy and reinsurance industry by contributing significantly to financial markets and offering funds to the economy.

Examples

Let us talk about a few examples to help you understand the topic.

Example #1

An online article published on 29 May 2024 discusses Grant Thornton's adverse viewpoint on Bermuda insurers, which is named Annuity and Life Re (Holdings). Furthermore, the auditor observed that the company had totally failed to consolidate the financial records of Multivir Inc., its subsidiary, because of fully impaired investment and impending plans to sell it to another company. Holdings have further reported $563,077 as its net income for FY 2023 in contrast to $1,937,212 as reported losses in FY 2022.

Moreover, the auditor pointed out that the financial position of the said company needed to be accurately represented by its financial statements in its conclusion. It highlighted important notes like bad loans to Multivir Inc., including $100,000 as allowances for principal and interest worth $869,019 in FY 2023 as compared to the principal of $51,500 and interest of $864,299 in FY 2022.

Example #2

Let us assume that a global insurance company – Megacorp, headquartered in Old York, faces exponential demand in hurricane claims due to climatic upheavals. Hence, to mitigate such a huge risk, Megacorp asks for help from AtlaRe, one of the reinsurer companies based in Fresh York. For this purpose, a treaty between AtlaRe and Megacorp takes place where AtlaRe would cover 20% of potential losses going beyond $1 billion from hurricane incidences in the US coastline occurring in the next year.

Moreover, the treaty also bound Megacorp to pay huge premiums to AtlaRe based on historical data and shared risk. As a result of the treaty, AtlaRe widens its risk across numerous clients and diversifies its portfolio, while Megacorp successfully protects its funding against any catastrophic event.

Reinsurer Vs Insurer

Reinsurer

- Provides protection to insurers against extreme losses through transferring or sharing risk.

- Spreads risks amongst reinsurers or insurance companies.

- The primary insurer has a contractual relationship with the reinsurer.

- Primary insurers pay premiums to them in exchange for taking responsibility for a part of their risks.

- Reimburses a part of the claims paid to insurers after they pay the claims.

- The amount of risk taken by reinsurers has certain limits as per reinsurance agreements.

- Risk exposure and the insurer's profile form the basis for assessing and underwriting reinsurance contracts.

Insurer

- Gives safety to the finances of businesses or individuals against sudden life health or business losses.

- Distributes risk between entities or individuals needing coverage.

- Individuals or businesses have a direct relationship with the insurer.

- Policyholders have to pay premiums to insurers based on risk factors and coverage.

- As per contract terms of insurance, they settle the claims of policyholders directly.

- Every individual and business policy has a specific, predefined coverage limit.

- Premium calculation and risk evaluation of individuals and entities lead to the assessment and underwriting of respective policies.