Table of Contents

What Is Regulation W?

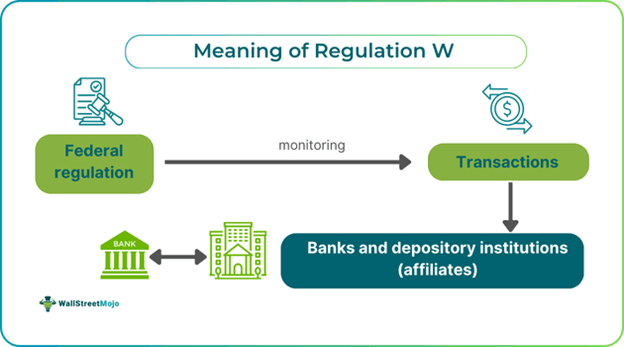

Regulation W is a federal legislation developed for limiting certain transactions between depository institutions like banks and affiliates (having common control with). The sole purpose of this regulation is to protect banks and federal depository insurance funds from unwanted risk by setting certain limits on transactions.

On April 1, 2003, the Federal Reserve Board enacted the Regulation W banking rule. It provides a foundational pillar for most banking transactions and drives the risk seen in the settlement process, compliance and regulatory systems. However, the act also expects greater transparency from banks and depository institutions.

Key Takeaways

- Regulation W is a federal rule issued by the Federal Reserve Board to oversee transactions between banks and depository institutions (also known as affiliates).

- Although this rule became effective on April 1, 2003, its history dates back to the Banking Act of 1933. It aims to prevent the misuse of banking resources.

- Among the various compliances, having collateral attached with credit given to an affiliate, transactions with an affiliate owing not more than 10% of the institution’s capital,

- Likewise, a similar value of not more than 20% capital in case of transactions with all affiliates is a key provision.

Regulation W Explained

Regulation W is a banking regulation that oversees depository transactions between banks and affiliates. It intends to protect the participants from any risk when transferring funds. Thus, if a bank tries to exceed its credit limits, legal consequences may apply. Simply put, this act tries to limit covered transactions (a transaction type with an affiliate that includes the borrowing or lending of securities). Also, it requires banks and affiliates to have collateral for certain transactions. This act includes two sub-sections, 23A and 23B.

Although the act was enforced in 2003, its history dates back to the 1930s. In 1933, the Congress passed Banking Act to prevent misuse of bank resources. However, there was a need to consider nonmember banks as well. Hence, the amendment of the Federal Deposit Insurance Act (section 18) allowed extension coverage to insured nonmember banks (by adding section 23A). Likewise, in 1987, an attempt to equate affiliate terms with nonaffiliate ones led to the addition of 23B in the Competitive Equality Banking Act of 1987. In the coming years, the definition of affiliate will also be amended to include financial subsidiaries.

With all these amendments, the Federal Reserve Board (FRB) officially adopted Regulation W banking rules to include 23A and 23B on December 12, 2002. Although this act came in 2003, the FRB issued a letter stating that other banks must comply with the guidelines mentioned in Regulation W 23A and 23B.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Compliance Requirements/Key Provisions

The Federal Reserve Board does require banks to follow some compliances to mitigate transactional risks in their operations. Let us look at the key provisions in accordance with Regulation W 23A and 23B in brief:

#1 - Quantitative Limits

- Any credit extended to any affiliate must be secured with a collateral security. It includes collateral in the form of cash, securities, or other readily marketable assets.

- Transactions with affiliates should not be more than 10% of the capital held by the institution.

- Likewise, transactions with all affiliates must account for only 20% of the institutional capital.

#2 - Definition of Affiliate

Here, Regulation W affiliate refers to the parent company, sister company (directly or indirectly controlled by the same company as that of the bank), and investment funds.

#3 - Covered Transactions

Regulation W-covered transactions include loans or extensions of credit, securities transactions, asset purchases, and other financial arrangements between a bank and its affiliates.

#4 - Depository Institutions

FRB defines depository institutions as insured depository institutions (any banks or savings associations whose deposits are secured by any corporation) that do not include a branch of a foreign bank.

#5 - Exemptions

- A set of transactions between the bank and its wholly owned subsidiaries do not fall under this act.

- Also, intraday extension of credit is treated the same way.

- This section also exempts the purchase of non-recourse loans (where only collateral is recoverable) from an affiliated insured depository institution.

When Does Regulation W Apply?

The compliances of Regulation W 23A and 23B apply to institutions depending on the type of transaction and relationship between member banks and affiliates. It includes various entities related to the bank, commonly known as affiliates. It applies to transactions with the affiliate that lead to borrowing or lending of securities to the extent that this transaction causes enough credit exposure. Likewise, Regulation W covered transactions and considered any derivative transaction creating similar exposure.

In the same lane, if the bank proceeds are used for the benefit or transferred to the affiliate (also known as an attributional transaction), it must follow the guidelines of this regulation. Other transactions include;

- A loan or extension of credit, including asset purchase (also subject to repurchase).

- Purchase of assets or securities issued or from affiliates.

- Any document pertaining to the granting of an acceptance, letter of credit, or guarantee. Additionally, it contains a standby letter of credit or endorsement from an affiliate.

- Acceptance of any security or debt obligation as collateral for any loan or extension of credit from the affiliate.

Importance

Regulation W plays a pivotal role in securing transactions between member banks and other depository institutions. It ensures that enough financial stability is maintained in the system. At the same time, it also considers the interests of the depositors vested in these financial institutions like banks. As a result, the depositors face minimal or no risk. Also, banks enable various risk management practices to mitigate any potential threat possessed by transactions initiated by the affiliates. Likewise, similar efforts are also made to create terms that favor both banks and affiliates. Hence, no participant feels that the terms of Regulation W affiliates act as a disadvantage to any participant.

Challenges

Apart from the regulations created for banks and affiliates, there are certain limitations of Regulation W. It includes a lack of awareness regarding regulatory requirements among business and support/control units, an incomplete or inappropriate list for affiliates and transactions related to them, and a lack of bank entity-specific policies, controls, and reporting for each entity. Additionally, outdated and expired policies for end-to-end transactional guidance for all businesses, functions, and entities (including the investment bank and front office). Even derivative transactions have limited guidance on collateral requirements and processes.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.