Part of our Political Economy guide

Redlining Definition

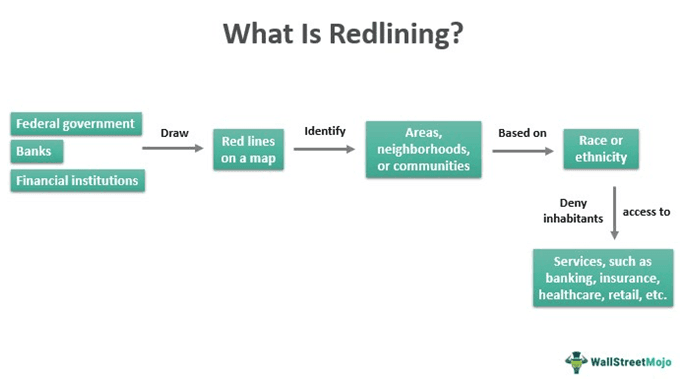

Redlining refers to the unethical, discriminatory practice of denying inhabitants of a particular neighborhood or community access to services, such as banking, insurance, healthcare, retail, etc., because of their race or ethnicity. It resulted from the age-old discrimination observed between the whites and the blacks in the United States, allowing the former to have their way.

The concept got its name from drawing red lines on a map to indicate areas where people of color would not avail of financial services. The federal government and banks propose systemic denial of loans services by either rejecting them or raising interest rates. It is common in student, consumer, business, home, automobile, and personal loans.

- Redlining meaning is the illegal practice of denying racial and ethnic minorities access to banking, insurance, healthcare, retail, and other services.

- The term originated from the practice of putting red lines on a map to highlight regions where people of color would not be able to access financial services, irrespective of their income or creditworthiness.

- The federal government and banks prohibit granting student, consumer, commercial, home, automotive, and personal loans by refusing them or increasing interest rates.

- The Fair Housing Act of 1968, the Home Mortgage Disclosure Act of 1975, and the Community Reinvestment Act of 1977 put a stop to discriminatory lending practices against the colored population of the U.S.

Understanding Redlining

Redlining restricts providing financial and other services to people of color or other minorities residing in a particular area. In the United States, it has prohibited generations of African Americans from obtaining home or home improvement loans. Besides, they were denied insurances and other financial services irrespective of their eligibility, such as income or creditworthiness.

The federal government, banks, and other lenders marked such neighborhoods and communities on the map via red lines to restrict lending services. Furthermore, unethical and discriminatory lending laws in these places were based on race rather than credit history. The red lines played a remarkable role in the history of discrimination in North America. The U.S. government implemented redlining on African Americans, either by disapproving loans or imposing higher interest rates.

Areas with a history of red line discrimination remain segregated and disadvantaged, with mostly non-white residents. Though redlining no longer exists, it created unequal wealth distribution between black and white people. Critics argue that the red lines in the heart and the social structure still exist, resulting in socioeconomic inequities.

In the 1960s, American sociologist John McKnight coined the term “redlining” to characterize the zoning of areas heavily populated by African Americans. These people were denied the benefits of financial schemes like mortgages and loans offered by the federal government or banks.

In his series of articles on redlining in real estate in the 1980s, American investigative reporter Bill Dedman highlighted how banks offered home loans to lower-income white individuals while refusing to lend to middle-income or upper-income colored individuals.

History

The origin of redlining dates back to 1862 when the U.S. government enacted the Homestead Act. The law excluded non-whites from government housing plans. Also, it kept them under the threat of violation if they were residing in the non-red-lined areas. It, thus, segregated blacks from the community and gave only a few parts far off from the white neighborhoods.

During the Great Depression in 1932, U.S. President Herbert Hoover introduced the Federal Home Loan Bank Act. It allowed lending institutions to apply codes to determine which locations were eligible for the federal government and bank mortgage loans and which were not. They used the color red to segregate regions for non-whites from whites. Anyone from those redlined areas was considered a risky investment by banks despite their creditworthiness.

In 1933, U.S. President Franklin Delano Roosevelt formed the Home Owners’ Loan Corporation, replacing the Federal Home Loan Bank Board. Its goal was to make mortgages affordable to promote homeownership. However, it did not provide any relief to neighborhoods predominantly inhabited by African Americans. The program marked areas on redlining maps as A (green), B (blue), C (yellow), and D (red). The new plan too avoided the D, i.e., redlined regions.

In 1968, the U.S. government introduced the Fair Housing Act as part of the Civil Rights Act, followed by the Fair Housing Amendments Act of 1988. Finally, the Act prohibited discriminatory lending practices based on race, ethnicity, gender, nationality, and religion.

The Home Mortgage Disclosure Act implemented in 1975 helped combat redlining and unfair lending practices. It required lenders to make loan data public. In 1977, the passage of the Community Reinvestment Act outlawed redlining. It encouraged banks and lenders to lend to the communities they serve.

Legal Implication

The redlining laws widened the racial divide by limiting access to various services, especially financial services, to whites only. As a result, redlining became an illegal and discriminatory practice. Furthermore, it prohibited banks from investing in the redlined areas. And the most critical aspect of the loan approval process was assessing the eligibility of the borrowers based on race and color rather than their creditworthiness or income.

Even though the Community Reinvestment Act put an end to redlining, the divide in the social structure still exists in the U.S., with the prevalence of racial discrimination.

Effects

The best approach to build equity in the U.S. is to own residential property. However, redlining limited the privilege of earning wealth to whites only. It resulted in an unequal distribution of resources across the country. The underdevelopment of redlined areas made its residents poorer.

The white and black residential premises in the U.S. are built based on the region’s exposure to pollution and its proximity with highways, banks, supermarkets, etc., with the former receiving priority in all respects. Investment restrictions in areas populated by racial or ethnic minorities harmed the housing market and economic growth.

The redlining practice impacted the overall social and economic structure. It also caused discrimination between the developed whites and the developing colored population. Even though housing policies underwent dramatic changes over the last eight decades, the inequality they caused persists.

Frequently Asked Questions (FAQs)

What does redlining mean?

Redlining is a practice of restricting financial and other essential services to residents of a particular area based on their race or ethnicity. The federal government and banks prohibit granting student, consumer, business, housing, vehicle, and personal loans to minorities by refusing them or raising interest rates. The name comes from drawing red lines on maps to indicate areas where people of color would not access financial services.

When did redlining end?

The Fair Housing Act of 1968, the Home Mortgage Disclosure Act of 1975, and the Community Reinvestment Act of 1977 ended unethical lending practices against colored individuals in the U.S. These laws required banks to make loan data public. Also, they encouraged lenders to lend to the communities they serve.

What are the effects of redlining?

The practice of redlining impacted the broader social and economic structure, resulting in discrimination between high-income whites and low-income blacks. Restricted investments in racial or ethnic minority communities negatively influenced the housing market and economic growth. Thus, the residents of redlined regions became poorer as a result of the underdevelopment.

Recommended Articles

This has been a guide to Redlining and its definition. Here we discuss how redlining works along with its history, legal implications, and its effects. You can learn more from the following articles –