Table Of Contents

What Is A Recourse Loan?

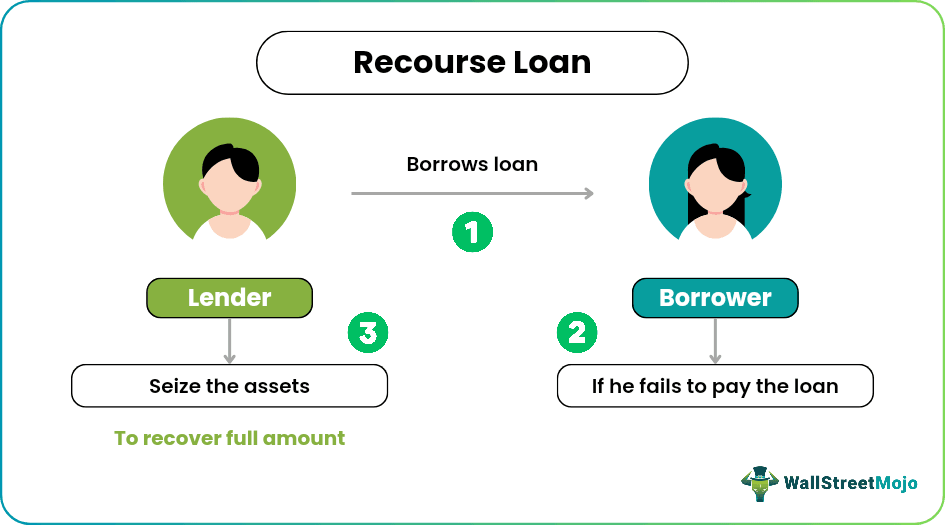

A recourse loan is a type of loan where the lender can extract the full amount of money lent to the borrower if they fail to pay. Then, the lender can seize the asset for which the loan was taken and confiscate the borrower's other assets to recover the full amount lent.

Whenever any borrower asks for a loan, the first check is whether the lender will get their money back. A recourse loan is a special legal safety given to lenders to protect their money. The lender's money to the borrower is an investment for the lender.

So, to safeguard the lender's investments, the government provides steps to recover the full money of the lender from the borrower. Such loans are protected loans for lenders, which helps them to recover the full loan money, even if the mortgaged asset failed to cover it up in full.

Table of contents

- What is Recourse Loan?

- A recourse loan is a loan where the lender can remove the full money given to the borrower if they cannot pay. Then, the loan lender may seize the asset for which the loan was taken and take away the borrower's other assets to retrieve the total amount lent.

- In a nonrecourse loan, the lender can sell the asset the borrower kept as a mortgage.

- Recourse loans are very demanding in the economy. They help small businesses to grow.

Examples of Recourse Loan

Example #1

Albert is planning to start a new business in catering. His estimation of cost is $50,000. He is not employed and has never taken any loan earlier. It will be difficult for Albert to get a loan from any bank looking for creditworthiness in the current scenario. He has never taken any loan earlier, so he does not have a credit score, making it even harder to get a loan.

So, he is getting a loan from a person or loan agency that will be giving a loan but with a clause that the loan will be recourse. Knowing that recourse loans are riskier than normal mortgage loans where the liabilities are restricted, he will still go for it as he needs money to do the business. However, if Albert fails to make payment, then the lender has the right to drag Albert to court and sell any or all of his assets to recover their money.

Example #2 - Full Recourse or Partial Recourse

Mr. X applied for a loan of $10,000 with full recourse terms from Thomas and used another loan of $20,000 with a partial recourse scheme (80%) from David. If Mr. X fails to pay both the loans, then Thomas will be able to recover his full money by selling assets of Mr. X in full, but David will also be able to recover his money to the extent of 80% of $20,000.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Influence of Recourse on the Borrowers

Any recourse loan is risky for the borrowers. It creates an extra liability on a borrower to pay the amount in full if the mortgaged asset falls short. However, borrowers who are actually in need of money and have intentions to pay back the money in full should not be worried about the recourse clause. Such loans are easy to get as it is safe for the lender, and they have the advantage of claiming any asset they want.

Recourse vs Non-Recourse loan

A recourse loan is a type of loan where the lender can claim the full money back if the borrower fails to pay back the money. In non-recourse, the lender has the right to sell the asset that the borrower kept as mortgaged.

For example, a borrower borrowed $10,000, and the asset he kept was worth $7,000. If the loan is non-recourse, then the lender can recover only $7,000 from selling the investment, and the rest of $3,000 will be again for the borrower and a loss for the lender. On the other hand, if the loan had been a recourse loan, the lender would have sold out the asset and other assets of the borrowers until and unless the loan is recovered in full.

Advantages

- Borrowers who do not have all the proper paperwork can still get a loan as the loan is safe to the lenders and ready to lend without all valid documents.

- Recourse loans help in the proper flowing of money in the economy. In addition, as the loan is safer than non-recourse, many new lenders invest their money, helping small businesses flourish and strengthen the economy.

Disadvantages

- In recourse loans, borrowers are charged a much higher rate than regular banks. It also makes it difficult for the borrower to pay the loan in full due to the increased interest rate.

- At times, lenders know that a borrower will not be able to pay back, but still, they give loans because they know that the asset values are more, which they want to confiscate.

- When a borrower fails to pay a loan, it means he does not have money. If lenders start to sell off their remaining assets, it gets really difficult for the borrower to cope psychologically

Conclusion

Recourse loans are very popular in the economy and are helping small businesses to flourish. As a society, we should all have good ethics, which will help us to grow together. It is the responsibility of the borrower to pay back the entire money borrowed. It is also necessary for lenders to think about the borrower's state.

If the borrower cannot pay the loan due to his poor financial condition, it is better to waive off part of the loan or the loan in full.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Generally, mortgages are nonrecourse loans. In this loan, they may only use the home as collateral. In other words, the lender can only seize the home if the borrower cannot repay the loan.

SBA loans help small businesses to grow. In addition, they do not provide recourse loan options. Still, they possess nonrecourse finances that protect the amounts for fixed assets, real estate, etc.

A partner's nonrecourse loan to a partnership refers to a recourse loan to the partner to the scope where another partner does suffer the economic risk of loss. A partnership liability is a nonrecourse liability if no partner has any financial risk of loss for that liability.

A loan that is secured by assets or collateral is referred to be non-recourse. The issuer may take possession of the collateral if the borrower defaults. Furthermore, even if the collateral is insufficient to fully offset the defaulted amount, they are prohibited from pursuing the borrower for additional damages.

Recommended Articles

This article is a guide to Recourse Loan and its meaning. We discuss the influences and examples of recourse on borrowers, advantages, and disadvantages. You can learn more about accounting and financing from the following articles: -