Table of Contents

What Is Real Estate Syndication?

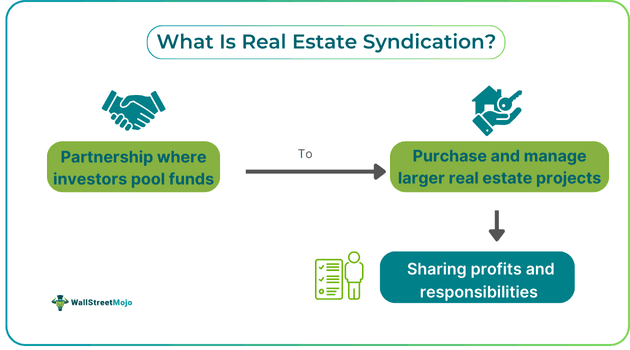

Real estate syndication refers to collaboration amongst more than one investor to pool their monetary resources together for buying or developing a single or multiple large commercial real estate properties. It aims to provide investors with participation opportunities in large-value deals that are not possible for any single investor.

It enables individuals to make investments in real estate assets without taking the burden of directly managing them while getting profits from possible returns on their investment. It helps investors combine their capital to access investment avenues in high-value markets, mitigate their risks related to property ownership, and diversify their portfolios.

Key Takeaways

- Real estate syndication comprises multiple investors pooling their resources to buy or develop large commercial real estate

- Offering participation opportunities in high-value deals not accessible to any single investor.

- It has three phases: Origination, Operation, and Liquidation, which involve identifying assets, conducting due diligence, closing deals, and selling or refinancing assets, respectively.

- It offers various tax benefits, such as interest and depreciation deductions, but market downturns or bad property management can lead to losses.

- It allows investors to own a share in the property using a syndicate, while in REITs, investors own shares of a company managing numerous properties.

Phases

For newcomers, real estate syndication can seem complex at first glance, but in reality, it follows a relatively straightforward process. Syndications generally proceed through three main phases, each with its own set of tasks and objectives.

- Origination—This is the initial phase, where the sponsor or syndicator focuses on identifying appropriate investment opportunities. It involves searching for suitable properties, conducting thorough due diligence, and assessing the asset's financial viability. Once the property is deemed a good fit, the next step is to negotiate terms and close the deal, secure financing, and finalize the acquisition.

- Operation – After acquiring the property, the syndication moves into the operational phase. This phase includes executing the business plan, which can involve anything from property renovation to leasing. During this stage, the syndicator oversees the day-to-day management and ensures that short- and long-term goals are met. The focus is on maximizing cash flow and property value through strategic operations like tenant management, improvements, or cost-cutting measures.

- Liquidation – The final phase is liquidation, where the goal is to realize the investment's gains. This often involves selling the asset after its value has appreciated or refinancing it to extract equity. Profits are then distributed to investors, allowing them to cash out, and the syndication comes to a close. In some cases, the asset may be held longer to achieve better market conditions before liquidation.

Examples

Let us understand the topic using a few examples.

Example #1

An online article published on February 7, 2024, discusses the challenges and risks associated with investing in private real estate funds.WCI founder Dr. Jim Dahleemphasizes the practical complexities of these investments due to the need for centralized performance data, unlike mutual funds. While real estate syndications often project higher returns than REITs or stocks, their actual performance can vary widely and is often opaque.

Dr. Dahle illustrated this with his investment of $100,000 in 2017, which:

- Projected a 57.5% gain

- Delivered a 14.1% return in the year leading up to September 2022

- It was anticipated to achieve a 12.9% internal rate of return (IRR), assuming liquidation by late 2023 or early 2024.

However, a recent update revealed that one of the fund's office properties experienced a complete loss of capital due to adverse market conditions. This event underscores the high risks inherent in syndicated real estate investments.

Example #2

Let us assume that a real estate syndication called Skyline Capital attracts investors to purchase a commercial property named OAKY in Old York City. The value of OAKY is $15 million. Skyline Capital's sponsor, who manages the deal, invests 20% (or $3 million) in the property, while 20 other investors contribute the remaining $12 million, with each investing between $200,000 and $1,000,000.

The syndication's goal is to renovate OAKY and lease its office spaces to technology companies. It promises to provide investors with a quarterly return based on rental income, yielding an 8% annual return. After 6 years, Skyline Capital sold the property for $20 million, resulting in a 50% return on the investors' initial capital, including rental cash flow distributed during the holding period.

Pros And Cons

Let us use the table below to understand the negatives and positives of the system of syndication for being safe:

| Pros | Cons |

|---|---|

| Small investors can participate easily in high-worth real estate deals using low capital. | Day to day management decisions can’t be taken by passive investors. |

| Provides investment portfolio diversification for investors throughout a wide range of multiple properties. | Market downturns or bad property management can lead to losses. |

| Tends to give passive, steady income to investors through rental income. | As they have long periods of holding so, they give limited liquidity options. |

| Offers various tax benefits like interest and depreciation deductions. | Requires huge upfront costs such as acquisition. |

| Experienced sponsors give expert property management leading to efficient property handling. | Passive investors may find it hard to comprehend the sophisticated agreements and legal nature of the structure. |