Table Of Contents

What Is Rabbi Trust?

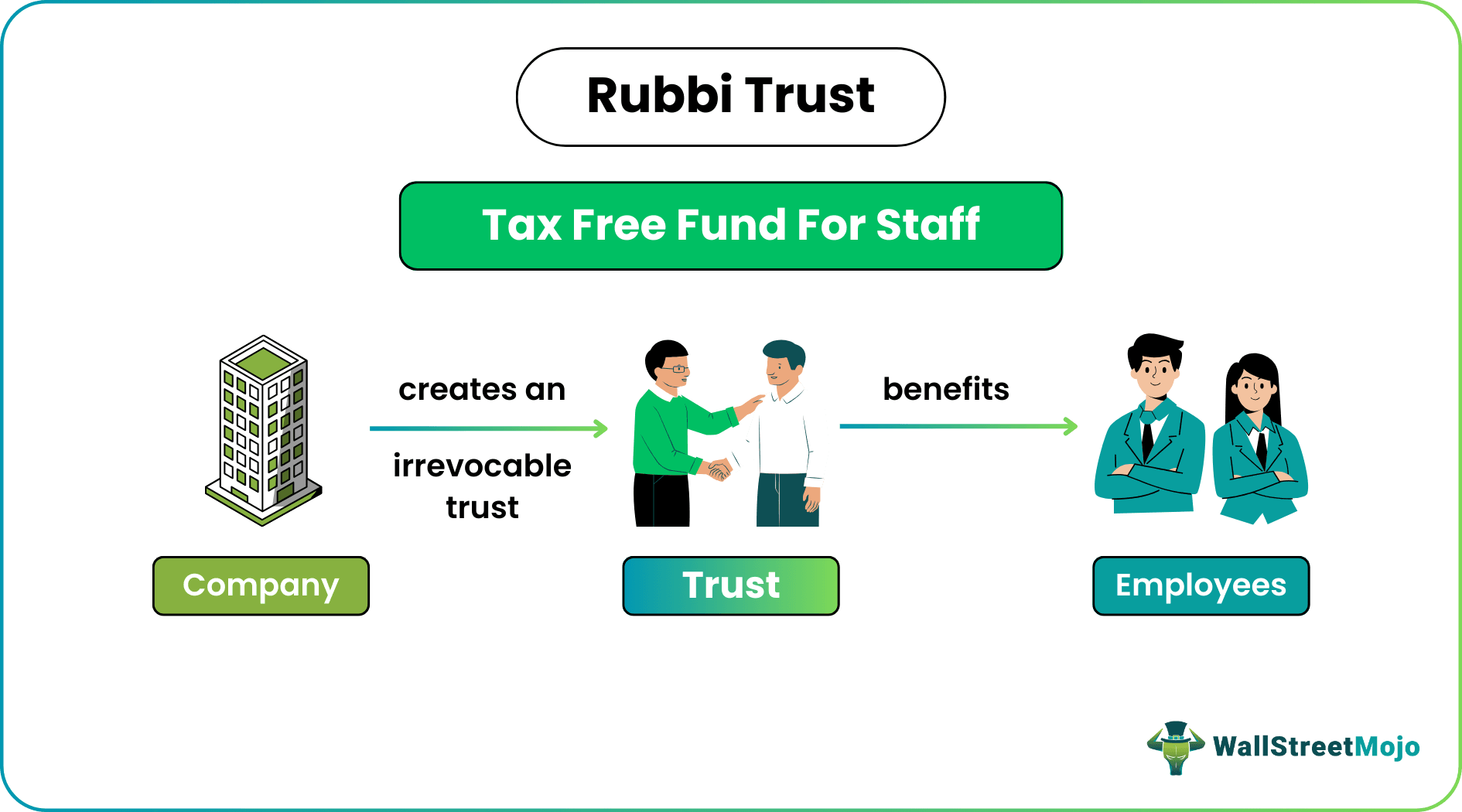

A Rabbi Trust is an irrevocable trust established and maintained by employers to set aside funds for their employees' benefit. The trust aims to provide security to employees by setting aside funds from the employer's general assets for their benefit.

Companies cannot withdraw funds from the trust to meet losses or expenses. Furthermore, any changes in management or mergers & acquisition do not affect the trust's funds. Only the beneficiaries have the power to change the details of the trust. However, creditors can claim trust funds to pay their outstanding dues if a company declares.

Table Of Contents

- What Is Rabbi Trust?

- Rabbi Trust is a non-qualified employee trust created to increase the employer and employee's mutual benefit and welfare.

- It ensures the safety and tax-free growth of the employees’ funds, assuring firms retain talented senior executives for business growth.

- The employer created the trust to benefit the employees in every situation except for bankruptcy and not to allow or protect the exploitation of employees by the employers.

- A significant difference between Secular and Rabbi Trust is that funds in the former remain safe from creditors, and creditors can claim it in the latter.

How Does A Rabbi Trust Work?

Rabbi Trust is defined as a special trust established by employers to provide a safe fund for the non-qualified benefit of their executives. Moreover, the Internal Revenue Service (IRS) authorized a Rabbi and his group to establish and use this type of trust in a private letter and Revenue Procedure 92-64, later known as Rabbi Trust. The Rabbi Trust plan aims to provide additional benefits to its employees in a secure and tax-efficient manner.

The trust's grantor is any company that creates it, and the trustee is the entity in charge of its daily operations, overseeing its management and administration.

The distribution rules for a Rabbit Trust are determined by the Trust's specific terms and the employer's plan. And this is how trust works:

- First, the employer establishes the Trust with the help of a legal and financial advisor.

- Then, the employer contributes funds to the trust on behalf of its staff. Therefore, the schemes offered by the Rabbi Trust plan include deferred compensation plans, employee retirement plans, and other non-qualified employee benefit plans.

- The trustee manages the funds contributed to the trust, which are held separately from the employer's general assets.

- Moreover, the employees do not have access to the funds in the trust until certain conditions are met, such as retirement, disability, or other qualifying events.

- Additionally, the contributions made to the trust by the employer can be deducted as a business expense, subject to certain limitations and requirements under the tax code.

- Lastly, when the employees become eligible to receive the benefits, they are subjected to income tax on the amounts paid.

As a result, a well-drafted Rabbi Trust agreement is critical to ensuring that the entrust operates under applicable laws and regulations and provides the intended assistance to executives securely and efficiently.

Taxation

Firms must understand the Rabbi Trust accounting & fundamental taxation regulations while drafting these trusts. It is because these trusts have some unique features not covered under the trust model of the IRS. Hence let us look at some essential taxation rules and their significance in the points below:

- The trust gets classified as a guarantor trust enabling the creditor to lay claim on it during bankruptcy.

- As a result, when an employee withdraws their funds from the trust, they will not be taxed on their deposits.

- Also, due to it, the trust offers tax-free growth of the funds for employees.

- Therefore, the income received by the employee through the trust funds deposited by the employer will not be subject to additional income tax.

- An employer has to pay all the taxes related to the fund.

- Employers will have to report all the deposits and income of the trust to legal authorities.

- The trust must comply with the rules and regulations under Section 409A of the IRS, which governs the taxation of non-qualified deferred compensation plans.

Pros And Cons

Let us look at both sides of the trust in the table below:

| Pros | Cons |

|---|---|

| Employees get the advantage of tax-free funds from the employer. | As per the trust’s distribution rules, employees get taxed when they withdraw funds. |

The funds grow till the employee withdraws them. | Generally, setting up and administering this trust can be expensive, particularly for smaller firms. |

| Employers use it as a means to retain talented top executives till retirement. | Employers must refrain from taking back their contributed funds in the Trust. |

| High-earning employees get additional pension benefits bypassing the IRS pension benefit limits. | Employers have no tax benefits from the government for the trust funds. |

| In the case of mergers, these funds remain intact for the employees. | Firms pay all the related taxes and formalities to the government. |

Example

Let us look at an example to clear our concepts. Suppose a company named Globex Corporation has top executives providing tremendous growth in its business, revenue, and brand reputation. The management does not want them to leave the company at any cost. Hence, they form a Rabbi Trust where the company will contribute five percent of the annual salary every quarter in the name of these executives.

The executive has a high-salary bracket of $150,000 annually. Therefore, they will receive an extra rabbi fund of $7500 quarterly in this trust fund. Hence their net annual salary would be $180,000. However, they would only pay the income tax on their annual salary of $150,000, not $30,000.

Thus, they would get a corpus of $300000 funds on their retirement besides the pension benefits and salary accumulation. Moreover, $300,000 would be taxed when they withdraw the funds from the trust. Therefore, one observes that the rabbi fund allows extra benefits and fund growth without tax liability as a supplementary pension on retirement.

Rabbi Trust vs Secular Trust

The main difference between the Rabbi Trust and a Secular Trust is their purpose and governing laws that apply to them. The former is a non-qualified Trust allowing the employer to set aside funds to pay its employees. On the other hand, Secular Trust is a trust where the grantor transfers the assets to the trustee to be managed to benefit one or more beneficiaries.

| Rabbi Trust | Secular Trust |

|---|---|

It gets set up to hold funds to create a deferred compensation plan. | It has been a fund dedicated to employees' benefits and welfare. |

These funds can get claimed by creditors during bankruptcy. | The trust could not get revoked under any circumstances. |

Other than creditors' claims, the funds get secure. | It provides tremendous benefits to the employee, like firewalling the funds from forfeiture. |

Limited grantor control over assets in the trust. | Greater control over the assets in the trust. |

Can be terminated if the employer becomes insolvent or if the plan is fully funded | The grantor or the court order can terminate it at any time. |

Frequently Asked Questions (FAQs)

These trusts can be funded or unfunded, depending on the terms of the trust agreement and the employer's preferences. However, in an unfunded trust, the employer promises to pay the employee in the future. On the other hand, a funded trust is where the employer sets aside the funds in a separate account.

No, the Employee Retirement Income Security Act of 1974 (ERISA) does not act on the trust as it has the nature of a top hat plan as section 201 of ERISA considers it a special maintained for paying deferred compensation to top management executives.

The trustee of this Trust can be any individual or entity willing to fulfill the fiduciary duties associated with serving as a trustee. Generally, the trustee is appointed by the employer or plan sponsor. In addition, the trustee may be a financial institution, a professional trustee, or someone familiar with the trust laws.

Recommended Articles

This article has been a guide to what is Rabbi Trust. Here, we explain its taxation, pros and cons, comparison with secular trust, and its examples. You may also find some useful articles here -