Table of Contents

What Is A Portfolio Loan?

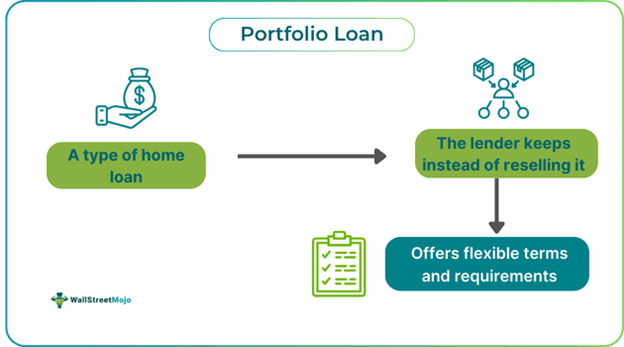

A Portfolio Loan is a type of home loan in which the lender issues and holds the mortgage in his investment portfolio instead of reselling it. These loans offer more flexible terms, conditions, and requirement criteria, which is why they are preferred by borrowers who are ineligible for obtaining conventional loans.

Portfolio lenders create and maintain the loans internally, as opposed to traditional mortgages that are offered for sale to investors on the secondary mortgage market. Since the portfolio lenders own and manage these loans, they have more autonomy when establishing the parameters of the mortgage, which is often beneficial to the borrowers.

Key Takeaways

- A portfolio loan is a type of home loan where the lender does not resell the mortgage but instead issues and retains it in his investment portfolio.

- Borrowers who are not eligible for traditional loans choose these loans because they provide more flexible terms, conditions, and lending requirements.

- Since these loans usually have less stringent requirements for credit score, credit history, and DTI ratio, individuals may find it easier to qualify for them.

- However, lenders often charge higher interest rates for these loans because of the lenient credit requirements.

How Does Portfolio Loan Work?

A Portfolio Loan is a type of mortgage that a lender provides and retains in their investment portfolio. Banks and credit unions underwrite these loans based on government-established rules and regulations. Based on the loan type, they generally involve a required minimum credit score, a maximum debt-to-income ratio (DTI), an essential down payment, and loan size restrictions. The lending requirements established by government-sponsored enterprises are not compulsory for obtaining such loans.

Potential homeowners who experience difficulty qualifying for a conventional mortgage loan may be able to purchase a property with the help of these loans. Since portfolio lenders do not require the same eligibility standards that traditional lenders do, they are incapable of selling their mortgages on the secondary market. Loan applicants with unconventional incomes or credit scores can acquire the funds they want to achieve homeownership through portfolio loans since traditional lending standards do not constrain them.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Eligibility Requirements

The portfolio loan requirements for eligibility are as follows:

- Individuals with poor credit histories may benefit from these loans. However, when evaluating their financial circumstances to decide whether they qualify for the loan, the lender will maintain a minimum credit score criteria.

- One benefit of this loan is flexibility with the down payment. However, the lender will still require a down payment, which will be determined by the borrower's income, DTI ratio, and credit score.

- The lender will verify the borrower's income streams and financial stability to make sure that they have the financial capacity to pay off the loan.

How To Get?

Portfolio loans are uncommon and are usually offered as a "perk" by lenders to their most loyal clients. If an individual has developed a long-standing connection with the local bank or credit union, they might be a suitable candidate to get such loans. To increase the likelihood of acquiring this loan, individuals may approach local lenders they have previously worked with and inquire if they are interested. In order to select a portfolio lender, individuals may initiate the process by analyzing the portfolio loan requirements and estimates offered by various portfolio lenders. It is beneficial to compare their offerings to standard lending options. Moreover, individuals must take into account the quality of customer service provided by each loan. To find out which loan option, terms, and conditions are the most suitable for them, individuals may seek out an expert home finance or mortgage specialist.

Examples

Let us study the following examples to understand this type of loan:

Example #1

Let us assume that Jake wants to buy a home and he does not have enough money to pay for the mortgage down payment. Moreover, he does not have a good credit score. As a result, he was denied a conventional loan. However, he approached a portfolio lender who checked his income stream and past credit history. He offered to lend him money with lenient terms and conditions but charged him higher interest rates. In this arrangement, the lender kept the loan in his investment portfolio. This is a portfolio loan example.

Example #2

Carlyle and KKR have come out among the last few bidders for a $10bn United States portfolio loan from Discover Financial, as reported by those who are acquainted with the situation. It took place as private investment companies stepped into a lending void created by the withdrawal of conventional financiers. As a team, the two investors are putting together an offer for the portfolio, which would satisfy their expanding credit requirements. These companies plan to extend far past their private equity foundation to obtain loans backed by assets like mortgages, rail carriages, rooftop solar energy, and credit card receivables.

Pros And Cons

The portfolio loan pros are:

- Individuals may find it easier to apply for these loans because they usually have less strict criteria for credit score, credit history, and DTI ratio.

- These loans have no lending limitations and might be an excellent way to obtain the financing required quickly.

- It improves the bond between lenders and borrowers. Since the lender manages the loan's administration, borrowers are likely to receive a customized approach.

The cons are:

- When lenders lend to borrowers who have unusual incomes or whose credit histories make them ineligible for conventional mortgage loans, they are taking on greater risk. As a result, they demand higher fees for such loans.

- Portfolio loan interest rates are often higher to compensate for the greater likelihood of default they bear when offering a loan with lenient credit conditions.

- This loan may contain a prepayment penalty clause, which is a cost imposed by lenders for early loan repayment.

Portfolio Loan Vs. Conventional Loan Vs. Blanket Loan

The differences are as follows:

Portfolio Loan

- These loans are mortgages that creditors issue and hold instead of selling on the secondary mortgage market.

- Compared to traditional loans, portfolio loans have less stringent underwriting requirements and shorter funding time frames. However, portfolio loan interest rates, closing fees, and down payments are higher.

- These loans may be feasible for borrowers who fail to satisfy the requirements for conventional loans.

Conventional Loan

- Conventional loans are mortgages for which the government does not provide insurance or guarantees. They are backed by and offered by private creditors.

- These loans come in conforming, jumbo, adjustable-rate, fixed-rate, and non-qualifying mortgage types.

- They are offered for both second residences and investment properties.

Blanket Loan

- A blanket loan, also known as a blanket mortgage, is a mortgage that covers numerous properties and uses the assets collectively as collateral.

- Since real estate investors and developers frequently purchase several properties at once, a blanket loan streamlines the process by combining all of the assets into a single loan.

- One does not have to repay the full amount due on a blanket loan if they sell off only one home.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.