Table Of Contents

What Is Periodic Inventory System?

A periodic Inventory System is defined as an inventory valuation method in which inventories are physically counted at the end of a specific period to determine the cost of goods sold. That means ending inventory balance is updated only at the end of the period instead of a perpetual inventory system where inventories are counted frequently.

Generally Accepted Accounting Principle allows firms to accept any model. xThe periodic system can be used in small and retail businesses where the inventory quantity is generally high, but the value is on the lower side. This way, businesses can save time and resources. The counting and tracking may be done either monthly, quarterly or annually and helps in keeping a steady and continuous record of the quantity of inventory with the company.

How Does Periodic Inventory System Work?

Periodic inventory system is a type of inventory management in which the company has to continuously keep a record of the inventory levels so that there is neither an excess quantity in storage nor there is a shortfall. If there is excess quantity then that may either be wasted or due to time lag, lose its value or benefit. It also leads to blocked cash which may be used for other beneficial purpose.

Similarly if there is a shortage, that may hinder the production and lead to mismanagement in the operation of the business. Thus, this kind of inventory management is very helpful.

The concerned department continuously keeps track of the raw materials, the work in progress and the level of finished goods, all three of them being a part of inventory tracking system. Under a periodic inventory system the goods are physically counted, without automatic use of any software of automated counting system. However, during the counting process, the accurate aand updated information of the inventory level will not be present.

The cost of goods sold is calculated in the process. But task can become tedious ad complicated if the quantity of inventory is very high and it also involves may types of the same. There is also the possibility of error while counting, misplacement or theft leading to inaccuracy.

Features

Here are some features under a periodic inventory system:

- Physical count – In this system, a physical counting process takes place in which the various levels of the stock which is the raw material, work in progress and finished goods are counted individually to record them in the books.

- No real time tracking – In the process, there is no real time tracking , which means that since there is no automated software of technology being used, there is a time gap between two counting sessions. During this time gap there is no accurate and updated stock level information.

- Calculation of Cost Of Goods Sold(COGS) – In this process, the COGS is calculated periodically in each case.

- Challenging process – Due to physical counting method, accounting periodic inventory system becomes complex and challenging and may lack visibility and control. There may be discrepancy and mismanagement leading to misleading information and data.

- Business based method – It should be noted that this kind of method is not suitable all types of business. It can be well managed in business that is small of has a fixed type of goods used as raw material or specifically requires periodic counting of stock for internal purpose.

Thus, the above are some characteristics of periodic inventory system which some companies follow to make their system efficient and transparent.

Steps

Below are the steps involved in the periodic inventory system –

- The Beginning and Ending Inventory is physically counted in a given period in this system.

- The company will also account for total purchases made for inventory in that period to find out the “Cost of Goods Available for Sale.”

- Cost of Goods available for Sale = Beginning Inventory + Purchases

- So, Cost of Goods Sold for that period will be:

- Cost of Goods Sold= Cost of Goods Available for Sale – Ending Inventory.

Therefore, the above are step by step approach to this kind of stock management which should be followed in the company so t make the system more efficient.

Journal Entries

The accounting periodic inventory system does not only involve counting the tracking the inventory levels but it also involves recording the entire system in the form of journal entry so the there is a clear record of it in the books of accounts.

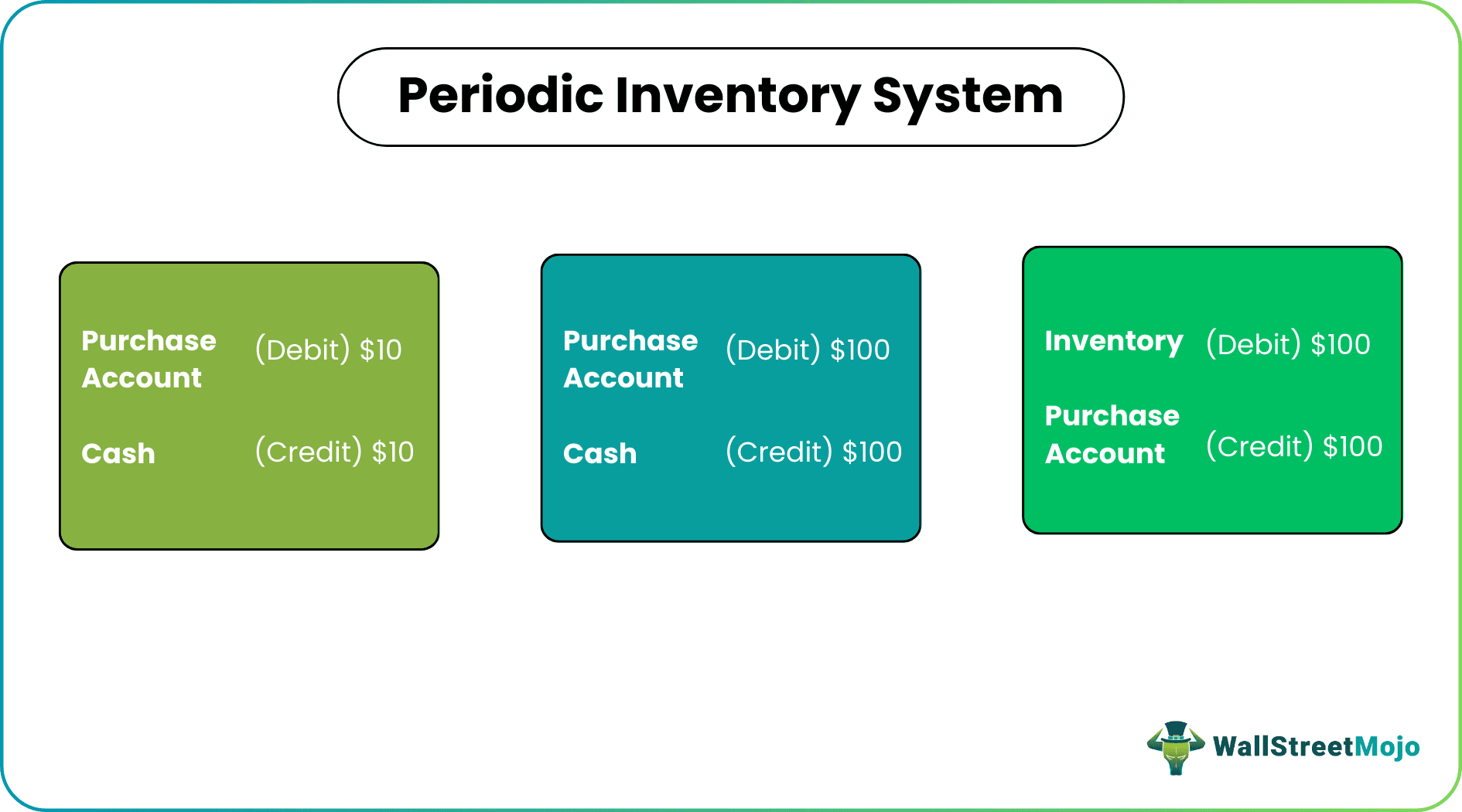

Let’s say you are running a retail business, in which your firm must purchase inventory almost every day to run your day-to-day business. Suppose your company has adopted the Periodic Inventory system for calculating the “cost of goods sold.” Now, on a given day, your firm needs ten units of inventory costing $1 each and has purchased that in the current accounting period through cash. In total, the purchase made $10. Of course, some of that inventory can become” Finished Goods” and be sold during the period, but your accountant doesn’t need to worry about that. Instead, a “purchase account” will be created in a periodic system for each bought inventory, which is an ‘asset.’ All the inventory purchases are stored in this account.

Periodic Inventory System Journal Entries for the same will be as follows:

| Purchase Account | (Debit) $10 |

| Cash | (Credit) $10 |

Same as above, let’s say for the accounting period, you purchased inventory for a total of $100(100 units of $1 each). Below will be the journal entries for the Periodic Inventory System –

| Purchase Account | (Debit) $100 |

| Cash | (Credit) $100 |

At the end of the accounting period, you need to determine your firm’s actual ending inventory and “cost of goods sold.” At first, his $100 will be shifted from Purchase Account to Inventory Account. This purchase account can be a temporary account to hold all the inventory purchases for a given accounting period.

At the end of the accounting period, below will be the process.

| Inventory | (Debit) $100 |

| Purchase Account | (Credit) $100 |

Examples

Let us try to understand the process with the help of example.

So, in this example of a periodic inventory system, your current period beginning inventory account was $1,000, and since at the end of a period, $100 was also added to that account. So, the inventory account now will be $1,100. This will be yours. “Cost of goods available for sale.”

Cost of Goods available for Sale = 1000+100 =$1100

We are having the final “Cost of Goods Available for Sale” as per our books. But the firm still doesn’t know the amount of inventory sold in the period. At the end of the period, your company will physically check the inventory. Let’s say the Ending inventory count is 1,050 units. Each unit costs $1, so the physical checked ending inventory is $1,050. To reconcile the physical inventory count with the inventory accounts in books, we will have to shift $50 from the inventory account to “Cost of goods sold.”

| Cost of Goods Sold | (Debit) $50 |

| Inventory | (Credit) $50 |

We can say the same as the below equation:

Cost of Goods Sold = Cost of Goods available for Sale -Ending inventory.

Here, we have not accounted for “Work in Progress,” “Raw Material,” etc. We are physically counting inventory only at the end of the period and reconciling that with the inventory recorded in the books.

Which Companies Use The System?

- The periodic inventory system advantages is mainly for small and retail businesses.

- Companies with relatively high inventory quantity but per-unit price is lower.

- Where companies cannot stop this daily routine to inspect inventory regularly physically;

Advantages

The system of periodic inventory has its own advantages. Let us look at them in detail in the points given below.

- Since no physical counting was needed between the periods, a lesser workforce was required. That means it is cheaper because there is no need to keep company. p workforce who will manage the stocks during that interval, saving time and money of the company.

- Regular work does not get hampered because of physical checking only at the end of the period. At that time, the concerned department will count for which a separate workforce is assigned without disturbing the routine.

- Quantity is physically inspected at the end of the period, so it is reliable in verifying the end-of-period accounting.

- No need to verify “Work in progress” or “raw materials” in between the periods. It is automatically done during the counting since the data collected after counting is used to keep track of the various stock levels, that is raw material, work in progress and finished goods.

Disadvantages

Along with periodic inventory system advantages there are also some limitations that should be noted before using the process. They are as follows:

- It will not provide any information about the Cost of Goods Sold in the interim period.

- Since there is minimal information between the periods, there can be a significant adjustment that needs to be made at the end.

- The chances of fraud are quite high.

- For large companies, this system is not suitable.

Periodic Vs Perpetual Inventory System

The above are the two types of stockpile tracking and management system that companies use according to their rules and requirements. But first, let us try to understand the differences between them.

- Inventory is not tracked daily for the periodic system, while it is physically tracked regularly after each transaction in the perpetual system.

- A Perpetual system is a costlier and more time-consuming process.

- In a perpetual system, goods count is limited, but they are highly valued. The main characteristics of periodic inventory system is that the inventory count is on the larger side with a lower value per unit value.

- Companies need a separate workforce for tracking inventory in the Perpetual system, which is not needed in the Periodic system since it is done occasionally.

- In a perpetual system, inventory quantity and condition can be known for the whole period, which is impossible in the periodic system.

Recommended Articles

This has been a guide to what is Periodic Inventory System. We explain it with example, journal entry & differences with perpetual inventory system. You may learn more about it from the following articles –