Table Of Contents

What Is Pay As You Earn (PAYE)?

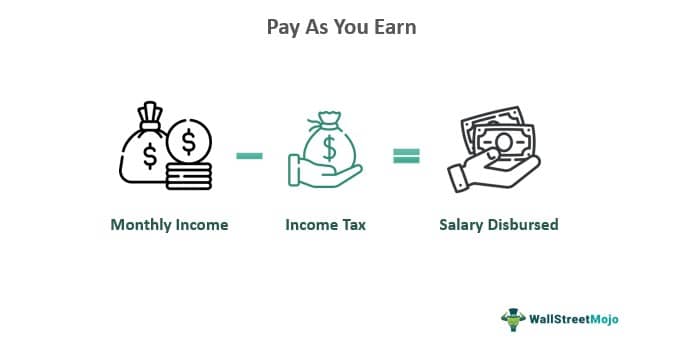

Pay as you earn (PAYE) is a tax payment system whereby the employer disburses the monthly salary to the employees after deducting their outstanding income tax, universal social charges (USC), and pay-related social insurance (PRSI) liabilities. This system aims to ensure that employees' taxes are deducted from their paychecks throughout the year rather than in a lump sum at the end of the year.

In many countries, PAYE is the system through which income tax and social security contributions are collected from employees' paychecks by their employers on behalf of the government. Employers are responsible for calculating and deducting the correct amount of tax and social security contributions from each employee's salary and remitting them to the government regularly.

Key Takeaways

- Pay as you earn (PAYE) is a tax payment system in which employers deduct income tax, social security contributions, and other relevant deductions from employees' paychecks on behalf of the government.

- The deductions made by employers through PAYE are considered pre-payments towards the employee's tax liability.

- The employee may be entitled to a tax refund if the amount deducted exceeds the tax liability.

- PAYE is also a loan repayment scheme initiated by the federal government for student loans.

How Does Pay As You Earn Work?

Pay as you earn (PAYE) or pay as you go is a process of withholding the due tax liability of a salaried employee automatically by the employer. The latter deduct the outstanding tax amount from the paycheck on each payday and then deposits it with the respective tax authority. It is applicable on every paycheck so that the burden of annual tax liability is evenly distributed throughout the period.

Moreover, if the sum deducted is more than the employee's tax liability, the surplus amount is repayable to the latter. Moreover, suppose the amount withheld as PAYE is less than the employee's actual tax liability. In that case, the difference is payable by the employee when filling out the income tax return with the tax authority.

In the UK, it is a mandatory practice for salaried employees whose earnings fall in National Insurance Lower Income Level. Furthermore, if a person jointly files the income tax return with their spouse, then their income and debt are considered for PAYE. However, if the spouses file the income tax return separately, individual income and liabilities are considered for PAYE.

Pay as you earn (PAYE) also refers to a federal government's student loan scheme with a repayment period of a maximum of 20 years, whereby the borrowers can repay the due amount in monthly installments, draining 10% of their discretionary income. The discretionary income is the difference between a borrower's adjusted gross income and 150% of the poverty line figure for their respective family size.

Qualifications

In the US, any person who has taken a federal loan for the first time after October 1, 2007, whether direct or direct consolidation or has taken a subsequent direct or direct consolidation loan after October 1, 2011, is eligible for the pay as you earn a plan. Moreover, the borrower should be able to provide evidence of their financial hardship by submitting the relevant documents.

Advantages

The PAYE system is beneficial to the government, tax authorities, employees, and students in the following manner:

PAYE as a tax payment system

- It is one of the crucial sources of revenue for the government.

- It facilitates the tax authorities in timely tax collection.

- The tax bur den of the employees, especially the lower income groups, is evenly distributed as they can pay a portion of their annual tax liability every month.

PAYE as a student loan scheme

- It is one of the most feasible income-driven repayment plans for low-income borrowers overburdened with grad school debt or federal student loans.

- A married borrower who jointly files the income tax return with their spouse can together repay the loan.

- PAYE is a good option for those who don't expect their income to rise significantly or have a big family size and are dealing with financial hardship.

Revised Pay As You Earn vs Pay As You Earn vs Income-Based Repayment

PAYE is a Federal government-initiated student loan plan with a maximum of 20 years of repayment tenure, monthly installments, and disbursing of 10% of the discretionary income instead of paying at a fixed rate. The revised pay-as-you-earn (REPAYE) is a kind of income-driven repayment scheme wherein the student loan is disbursed with a repayment period of a maximum of 25 years and is repayable at a percentage of the borrower's discretionary income.

An income-based repayment (IBR) refers to the loan schemes initiated by the federal government whereby the borrowers can pay off the obtained money in monthly installments. The annual repayment usually amounts to 15% of the borrower's discretionary income.

Some of the other dissimilarities between these three plans are discussed below:

| Basis | Pay As You Earn (PAYE) | Revised Pay As You Earn (REPAY) | Income-Based Repayment (IBR) |

|---|---|---|---|

| Eligibility | Must have taken a federal direct loan or direct consolidation (FFEL or Perkins loan) between October 1, 2007, to October 1, 2011; Regular payments have been made toward these loans; Possess documents to prove financial hardship. | Must have taken a direct loan from the fed. | No new borrower qualification is required. |

| Repayment Cap | 10% of the borrower's discretionary income depending upon the standard repayment plan cap. | 10% of the borrower's discretionary income. | Before July 1, 2014, 15% of the borrower's discretionary income depended upon the standard repayment plan cap; on or after July 1, 2014, 10% of the borrower's discretionary income depended upon the standard repayment plan cap. |

| Repayment Tenure | 20 years | 20 years for undergraduate students and 25 years for graduate students. | If borrowed before July 1, 2014, the repayment period was 25 years; but borrowings on or after July 1, 2014, are repayable in 20 years. |

| Interest Subsidy | In the case of subsidized loans, the government pays off the interest or the difference for three consecutive years when the borrower's monthly income is not enough. | In case of negative amortization, when the monthly earnings are insufficient to meet the interest, the government bears 50% of the difference. | In the case of subsidized loans, the government pays off the interest or the difference for three consecutive years when the borrower's monthly earnings are not enough. |

| Forgiveness | The balance amount is forgiven after 20 years of making regular payments, and the income is considered taxable by the IRS thereafter. | The balance amount is forgiven after 20 years of regular payments for undergraduate students and after 25 years of regular payments for graduate students. Also, their income is considered taxable by the IRS thereafter. | Before July 1, 2014, the balance amount was forgiven after 25 years of making regular payments. However, on or after July 1, 2014, the balance amount is forgiven after 20 years of making regular payments. In both cases, the income is considered taxable by the IRS thereafter. |

| Married Borrower | In the case of joint filing, the income and liabilities of both the partners or spouses are considered. | Whether it is a separate or joint filing, both spouses' income and liabilities are considered. | In the joint filing case, both partners' income and liabilities are considered. |