Table Of Contents

What Is A Pass Through Entity?

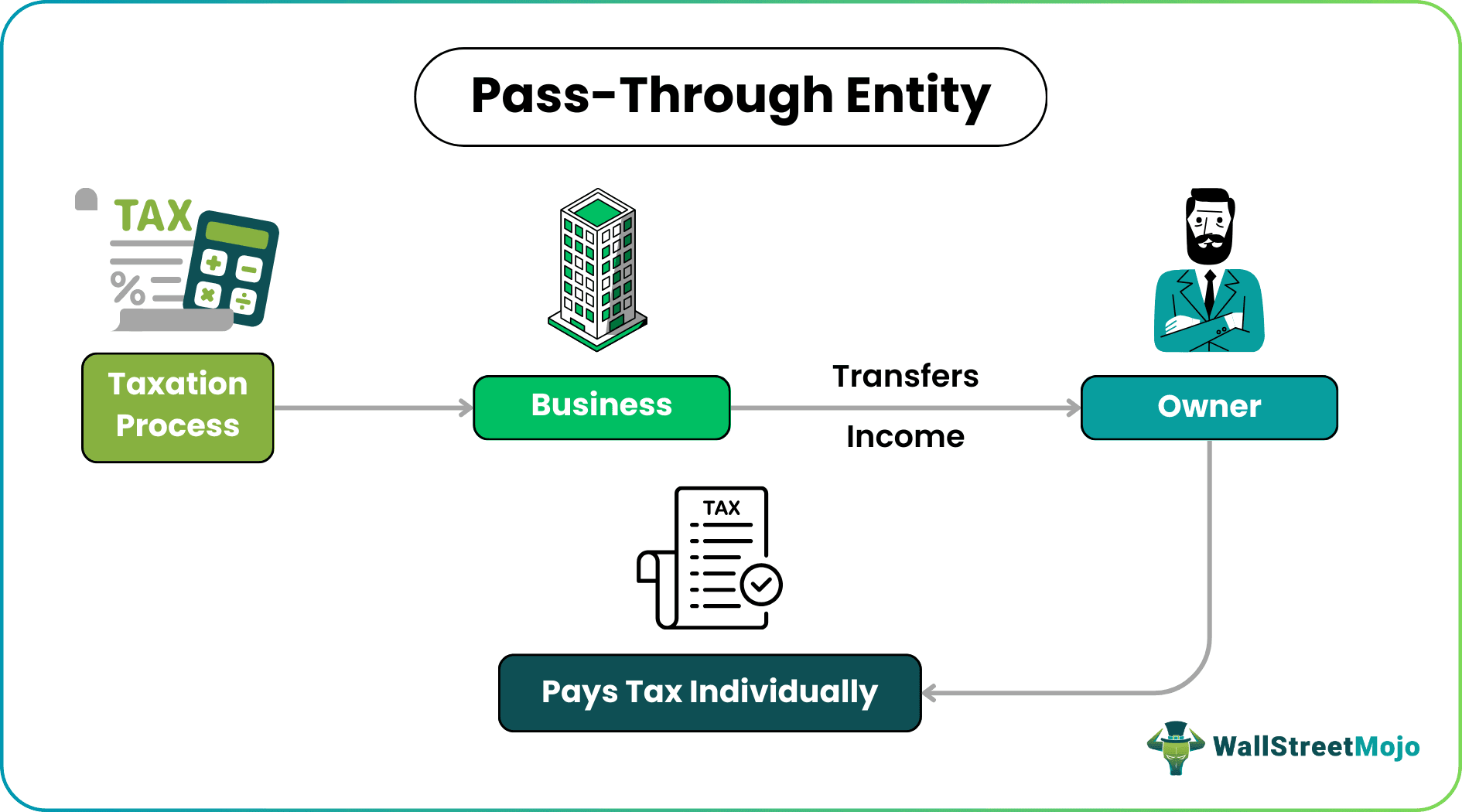

The pass through entity can be defined as a process by which any organization will be relieved from the double taxation burden. The entity passes its total income to the entity's owners; therefore, taxes are calculated individually for every owner.

The reason for passing through income structure is that the owners otherwise get double taxed. First, they pay taxes on the corporate profit, and later when the profit after tax is distributed to the owners, it is double taxed as individual income.

Table of contents

How Does Pass Through Entity Work?

A pass through entity, also commonly known as a flow-through entity is a type of legal business organization that transfers all its income in the name of the investors or owners, in order to avoid double taxation. In this process, the organization does not have to pay any taxes, rather the owner pays tax based on their individual rates on income.

This concept is followed in various kind of business. Since both the owner and business are liable to pay tax, there is a problem of paying tax twice, even though the owner is a part of the entity and earning from the same. Therefore, to avoid this, the system of flow-through is commonly followed, which shifts the entire earned income of the business in the name of the owner, who pays tax only once on the income earned from the business.

Thus, the tax liability entirely passes on to the owner, which is treated as their personal income, and they pay tax on it. But here the owners also need to keep in mind that they can also apply for any loss faced by the company against this income that is transferred in their name under the pass through entity deduction.

But sometimes the owners may have to pay tax on earnings that they have not yet received, Such, cases happen when the profits are reinvested in the business and not distributed to owners. But since the profits are appearing in the books, tax will be charged on them. Sometimes sole proprietors need to pay tax on self-employment, which will result in a huge tax outflow for the proprietor if the flow-through entity system is followed. In such cases, it is important to understand the tax implications thoroughly.

Types

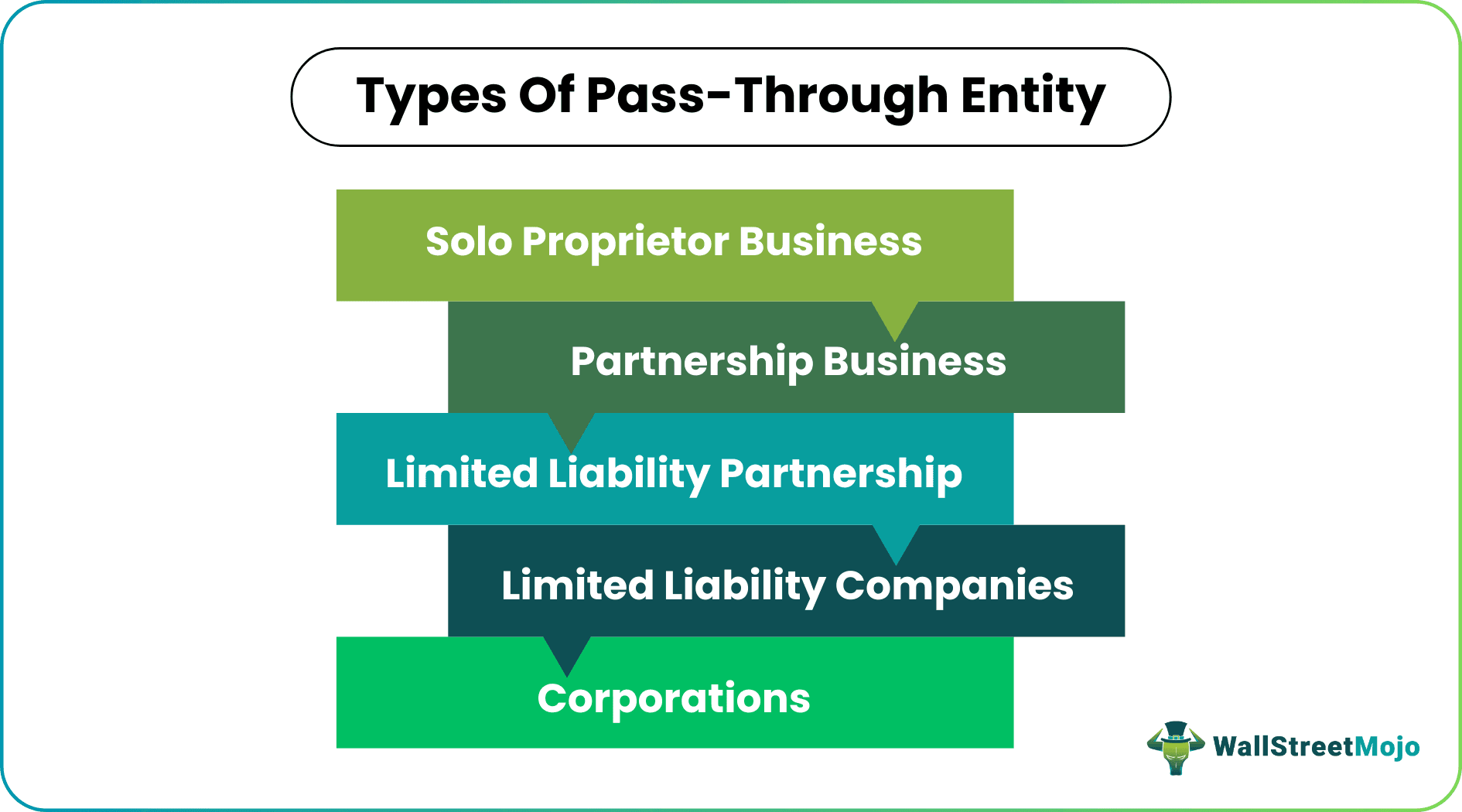

This method of electing pass through entity is very good for avoiding double taxation and many types of organizations use it to make the tax payment less complex. Let us understand the different types of organizations that follow this process.

- Sole proprietor – In this case the owner is a single person who will not have to file for tax return separately. They need to report their net profit on Schedule C, Form 1040. However, the net income of such business owners also need to pay the payroll taxes, which falls under the Sel-Employed Contribution Act (SECA).

- Partnerships – In case of partnership pass through entity, they file for tax returns at entity-level (Form 1065). But not all owners are allocated profits. Only those who report their net income on Schedule E (Form 1040), get the profit share. Genetal partners pay the SECA tax , while limited partners, who’s liability is limited upto their contribution to the business, pay SECA tax on “guaranteed payments” that are like a compensation for labor service.

- Limited Liability Companies – The owners of such organizations, who are also known as members, may be the above or even foreign entities. They do not have any limit to the number of members.

- S Corporations – They may be any domestic corporation that elect to work as S Corporation. They need to file for tax return but the profits are transferred to the shareholders and reported in Schedule E (Form 1040). Their shareholders are limited to 100 ad can issue only one type of stock. They do not pay SECA Tax.

Examples

Let us understand the concept of pass through entity deduction and taxation with the help of some suitable examples, as given below:

Example #1

A manufacturing partnership firm distributes its income entirely to its partners. The firm is considered a pass through entity. Suppose the income for the year was $40,000, and expenses to meet the business requirements were $20,000.

Now, the earnings before interest and taxes come to $20,000 i.e. ($40,000 – $20,000).

If the interest on the loan is $5,000, the earnings before taxes (EBT) come out to be $15,000. It is the firm's income for the year after deduction, which will be distributed among the partners in a ratio mentioned on their partnership deed. Say, for example, the partners have agreed to share 50% each. Then the income will be distributed equally between each one of them. By following this method, the partners will be taxed only once in their capacity, leading to a lower tax burden.

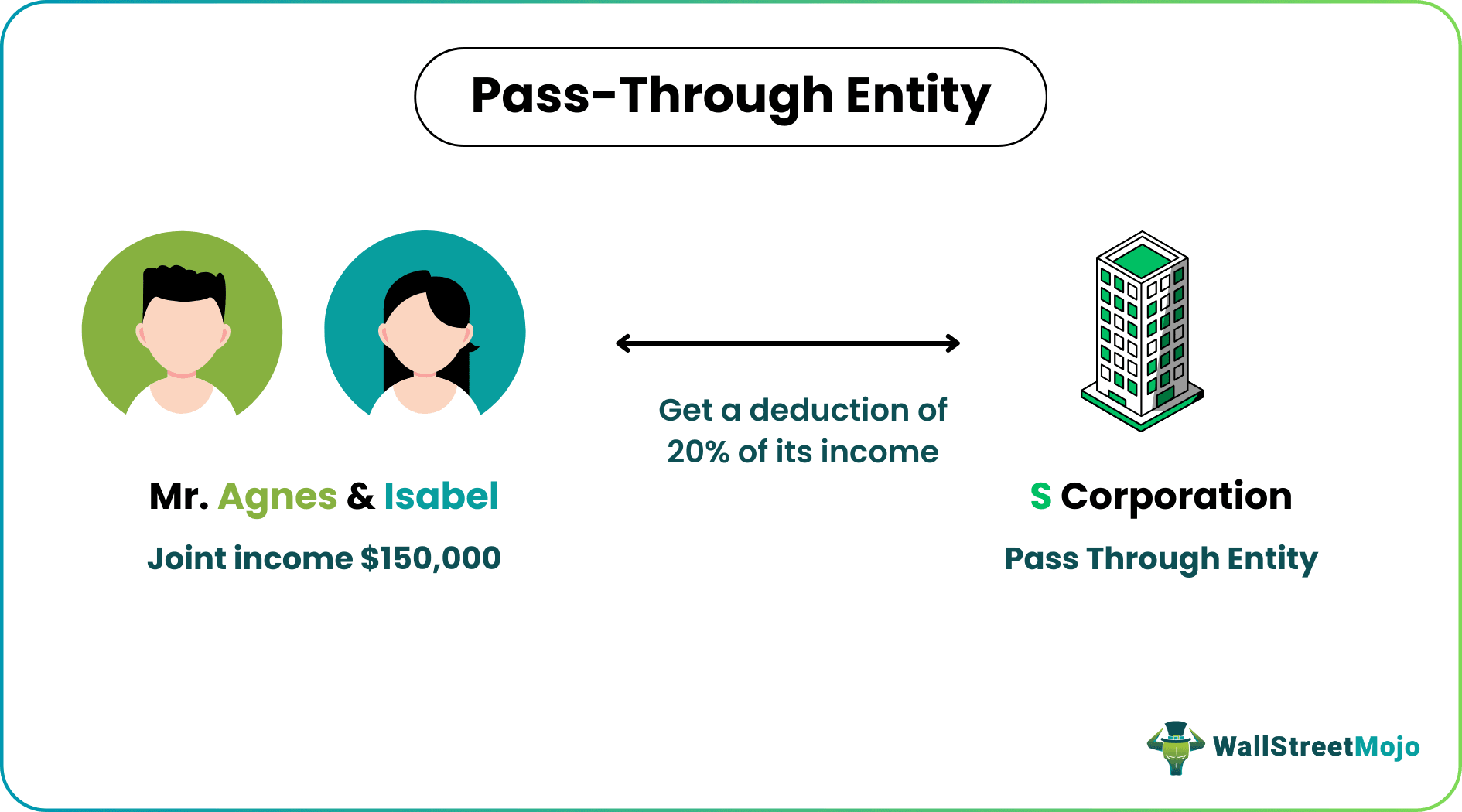

Example #2

Let’s take another example. Mr. Agnes is a sole proprietor. He is engaged in a construction business. He is married to Isabel, and now their joint income is $150,000. He plans to open an S corporation so that the entire income of the husband and wife gets clubbed. Also, they may be eligible to get a deduction of 20%. Per the general rule issued for pass through entities, the owner will get a deduction of 20% on its income. Mr. Agnes can now claim a deduction for the entire $150,000.

The above examples give us a clear idea about the process of electing pass through entity in which the concept is followed in entities in order to avoid double taxation.

Benefits

Some common benefits of the concept of relevant pass through entity are given below:

- Tax Benefits: The most significant benefit of using this mechanism is that people in business can easily save on their taxes. The pass through entity helps the business owners pass their income to them. Double taxation can be avoided using this mechanism. Owners have to pay taxes on their dividend income and the income from their businesses; thus, they are relieved from paying double taxes to the government. The government approves these mechanisms, so there are no chances of future obligations regarding the taxes on the same.

- Income gets Clubbed: The income of both husband and wife can get clubbed if the income is routed through a corporation or LLC. The income tax will be given on the sum after clubbing.

- Deduction Available: The basic deduction of 20% on the income is available to the owners, 20% on the qualified business income.

- Income can be Diverted: If an S corporation or LLC owner opts to get their business income passed through the S corporation, he can easily do it. The income will be taxed on a simple individual tax bracket for an individual and his business. The owner can arrange to get a fixed amount from this type of pass

- through entity he has created. A later stage can show this as a salaried or fixed income and will pay a tax per normal tax rate, which is levied on salaried income. Using this mechanism, he will easily escape the corporate taxes he has to pay for that income.

- Limited Liability Obligation: This type of pass through entity's owner has one advantage: limited liability. It means that whatsoever happens, the assets of the owners are well protected. In case of litigation also, the owners are relieved from the claims.

- Easy Switching Options: It is very easy to switch the potions in which we would like to be taxed. Suppose we have an S corporation and plan to switch it to LLC. We can easily do it. Thus this helps in the planning of our finances as well.

Limitations

The limitations of the concept of relevant pass through entity are detailed below:

- Profit Distribution System: In this mechanism, the profits or losses will be shared by the owners in their desired ratio, but in some types of pass through entities, the distribution is restricted to the percentages of their own in that corporation. Now, this creates confusion and disagreement between the owners. Thus this becomes one of the most important disadvantages of this type of entity.

- The Complication in Registration Formalities: Saving taxes is an art that is a little bit complicated also. The registration process in this type of entity is somewhat complicated in the beginning. The government checks all the documents carefully and then gives the registration number. After getting the registered entity, the owners can switch the S corporation to LLC or vice Versa.

- Rules Changes from Each State to State: The rules are different in all states and countries. The owners are not allowed to use the rules as a whole. They have made their corporation's rules per the state, which can be a bit complicated. Moreover, whenever they want to migrate to another state or country, they again have to consider establishing the rules; this is the biggest problem with the pass through entity. Even they have to make a point while transacting with other states and countries.

The concept of a pass through entity is very structured. The entity helps us avoid double taxation each time the owner pays tax as an individual and corporate taxpayer. This mechanism is ingenious for those who can use it carefully. The cons of this mechanism should also be considered while planning to opt for such a scheme of business structure.

Pass Through Entity Vs Disregarded Entity

Both the above are related to organizations following a particular tax payment system which prove beneficial for them. However, there are some differences between them, as follows:

- As the name suggests, the former has a system where they can pass on the taxes from the business to the owner, but the latter is a type of entity that is typically ignored or disregarded for taxation purpose by Federal government.

- In case of the former. Such entities can be single owner or sole proprietor, partnership pass through entity, S Corporation, LLCs, and so on. But in case of the latter, commonly the entity is a single member one, in which the IRS (Internal Revenue Service) disregards it as an organization that is separate from the owner,

- In case of the former, there are S Corporations that pay taxes which transfers the income to the shareholder and the shareholders are taxed. But in case of the latter, since they are sole owners, they may choose to be taxed as separate legal entity who will pay tax on their income, in which case they are called C Corporation.

- For the former, the tax payment system may become complex as the type of entity changes, which means, for sole ownership, the process may be easy but for partnership or LLC or S Corporation, the process becomes complex, due to increase in the number of owners. But on the other hand, the tax payment process remains easy for the latter due to only one member.

- Under IRS, a single member entity will automatically claasified as a disregarded entity. But in case of any other form of organization, it is not done so. They may be disregarded or pass through entity.

Thus, the above are some basic differences between the two concepts.

Recommended Articles

This article has been a guide to what is a Pass Through Entity. We explain it with examples, differences with disregarded entity, benefits, limitations & types. You can learn more about accounting from the following articles –