Table Of Contents

What are the Overhead Costs?

Overhead costs are those that are not related directly to the production activity and are therefore considered indirect costs that have to be paid even if there is no production; examples include rent payable, utilities payable, insurance payable, and salaries payable to office staff, office supplies, etc.

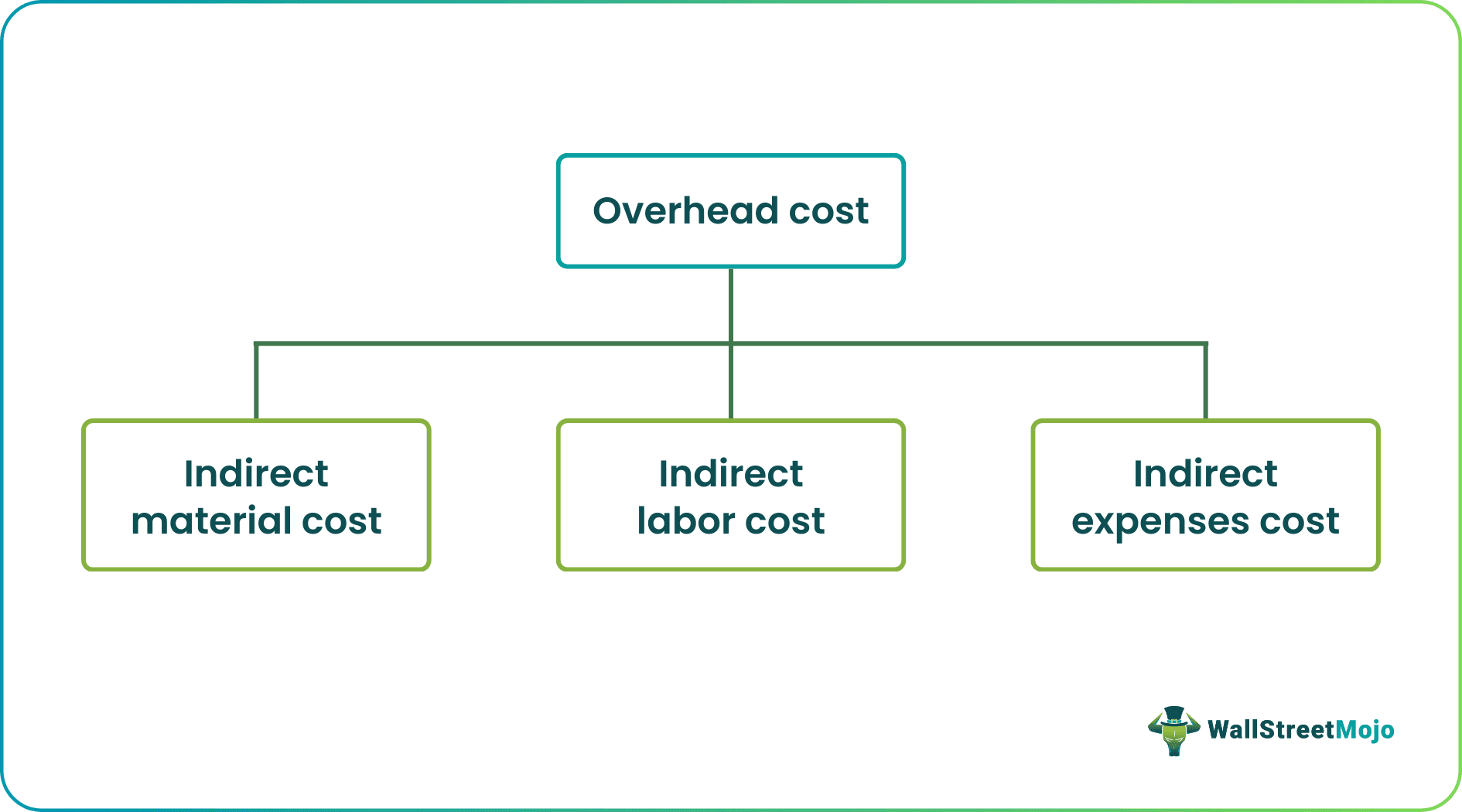

Overhead Cost refers to the cost of indirect material, indirect labor, and other operating expenses, which are associated with the typical day-to-day running of the business but cannot be conveniently charged directly to any specific product or service, or cost center. They are Indirect and need to be shared among the cost units as precisely as possible. In other words, it is the cost incurred on labor, material, or services that cannot be economically identified with a specific saleable cost of goods or services per unit of the business.

- Examples include the cost of Indirect Material, Indirect Labor, and Indirect Expenses. It varies from business to business, and they are an indispensable part associated with the smooth running of the business.

- They vary with the level of production (Variable Overheads), or they may be altogether independent of the level of output (Fixed Overheads) or a mix of both (Semi-Variable Cost).

- A business needs to keep a close watch on this cost, and efforts should be made to keep it low as that gives the business the ability to price its products more efficiently so that it remains competitively superior to its competitors.

Table of contents

Calculation Example of Overhead Costs

Overhead Costs include Advertising Cost, Insurance Cost, Rent, Utilities, Depreciation, Spoilage cost, Postage & Stationery Expenses, etc.

Let's understand the same with the help of a Numerical example:

ABC Limited has incurred a total overhead cost of Rs 120000 and spent 24000 direct labor hours (10 workers employed for 48 hours per week for 50 weeks during the year)in a production of its three product lines A, B, and C. ABC is trying to work cost one its product line. A. Details of which are as follows:

- Material Consumed: Rs 2000

- Direct Labor Hours: Process A: 10 hours @ Rs 8 per hour

- Process B: 5 hours @ Rs 10 per hour

- Work Overhead is levied based on Direc Labor Hour Rate

Direct Labor Hour Rate= Rs 120000/24000.

= Rs 5.00 per hour

Types of Overhead Costs

Based on Behavior wise classification, we can divide this into the following types:

#1 - Behavior- Wise Classification

Based on Behavior wise classification, we can divide this into the following types:

- Fixed Overheads

Such Overhead expenses are the ones that are fixed in nature and don’t get impacted by the increase or decrease in production activity or volume of output manufactured by the business. These Overheads are fixed within a specified limit and are not influenced by managerial actions up to such limits.

Fixed Overhead Examples include Rent and Depreciation.

- Variable Overheads

Such Overhead expenses are the ones that vary in direct proportion to the output volume. These overhead expenses are directly affected by business activity.

Variable Overhead Examples include Shipping expenses, Advertising Costs, etc.

- Semi-Variable Overheads

Semi-Variable Overhead Expenses are the ones that are partly fixed and partly variable in nature. As such, they contain both fixed and variable elements and, therefore, don’t fluctuate in direct proportion to business output. Semi-variable overhead examples include Telephone Charges etc.

#2 - Function- Wise Classification

Based on Function wise classification, it can be divided into the following types:

- Manufacturing Overheads

It comprises all indirect costs, whether in the form of Indirect material, indirect Labor, or Indirect Expenses, which are incurred in the manufacturing of the goods and services. It is also known as Factory Overheads, Work Overheads, etc.

- Administrative Overheads

It comprises those costs incurred in discharging the accounting and administrative services, and it is impossible to associate the same with the per-unit cost of production.

- Selling and Distribution Overheads

It comprises the selling and distribution overheads incurred in marketing and dispatching of the products and includes expenditure incurred in transportation etc.

- Research and Development Overheads

These Overhead expenses are usually incurred on a new product or process development. They are not identifiable to be charged on any specific product or service line catered by the business.

Examples include the cost of raw material used in research, staff cost indulged in Research, etc.

Allocation of Overhead Costs

It is a two-step process which comprises:

#1 - Selection of Approximate Cost Center

It involves an analysis of the Overhead for selection to the appropriate Cost Center. It will depend on several factors, including the level of control required and the available information.

#2 - Determination

This stage involves analysis to determine the Overhead Cost, which can be assigned to each Cost center, and it involves Cost Allocation and Cost Apportionment. Cost Allocation is achieved by identifying a cost specifically attributable to a particular cost Center. In cases where the same is not possible, Cost Apportionment is applied to allocate the cost among cost centers based on the estimated benefit received by each cost center. For example, it is impossible to allocate electricity expenses in a Service Organization across its divisions, and as such, the cost is apportioned among the divisions based on Estimates.

Conclusion

Overhead Costs are an essential part of the total cost incurred by a business in the production of goods or rendering of services. They require close monitoring to ensure the same is within acceptable levels.

Recommended Articles

This article has been a guide to what overhead cost is in accounting and definition. Here we discuss types of overhead costs along with calculation examples and how to allocate them. You may also have a look at the related articles: