Part of our Banking Products guide

What Is Open-End Credit?

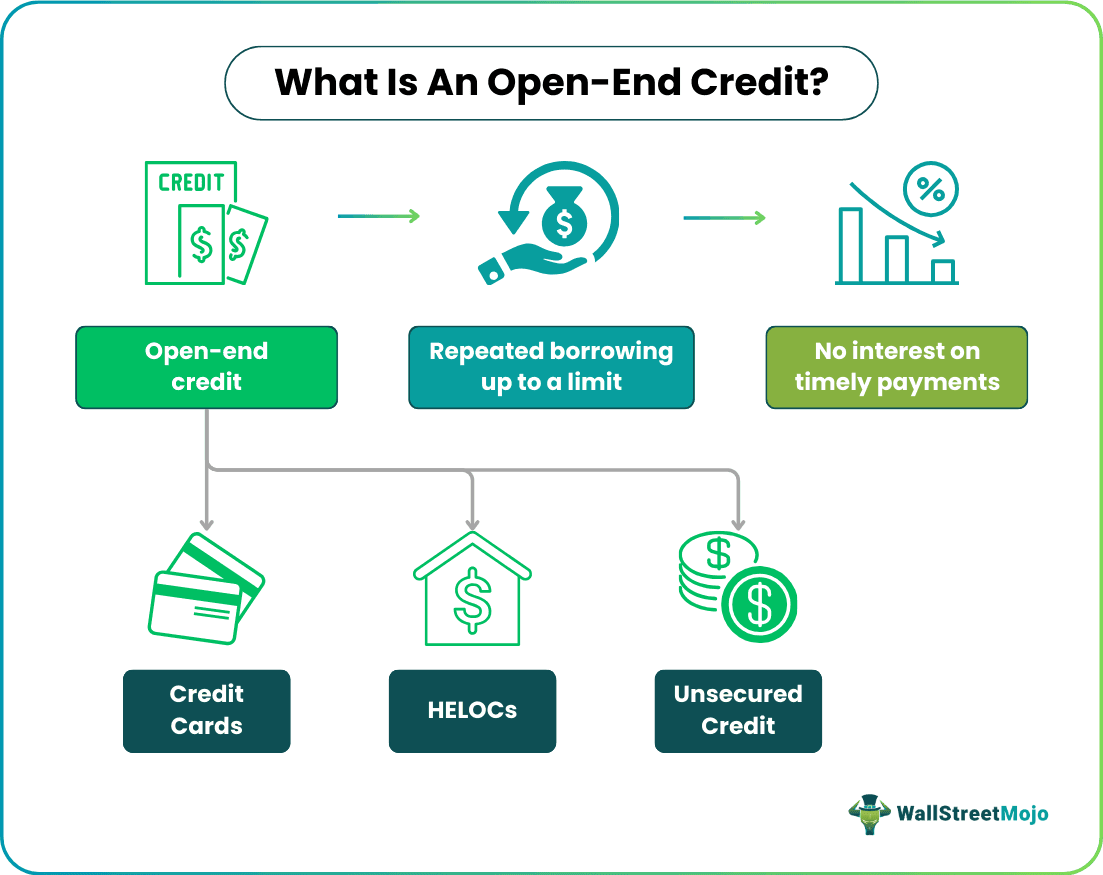

Open-end credit is a type of financing where a borrower can borrow as many times as possible up to a certain limit and repay them on the due date. Also called revolving open-end credit, the main objective of this credit facility is to allow flexible borrowing and support firms and economies.

It is a pre-approved loan given by financial institutions like a credit card that allows individuals easy access to money anytime. Also, if an individual manages to make timely payments, there is no interest charged to them. However, there can be an annual fee applicable to the user.

- Open-end credit is a loan facility given by financial institutions where a person can borrow money many times until it reaches the defined limit. Then, on repayment, they can borrow again.

- The most popular credit facilities include credit cards, where re-borrowing occurs until full credit payment. Other types include HELOCs and unsecured lines of credit.

- It is suitable for shorter periods as there are monthly repayments of the borrowed amount.

- After repayment, the credit renews, and the user can borrow again with the same facilities.

Open-End Credit Explained

Open-end credit allows borrowers to borrow money as many times as they need to a certain level. The borrower must repay the issuer (lender) as soon as it exceeds the limit. Once payment is made, they can borrow again to that limit. If they fail to make payment, the lender might charge interest on them. For example, credit cards allow people to borrow money repeatedly and repay the amount to the card issuer.

Unlike other forms of credit, an individual can use the same credit repeatedly as often as they wish. Once they make purchases with that credit, they must pay back the principal plus interest. So, if they pay on time, their credit score will improve. If the current limit is non-satisfactory, they can ask the lender to increase it. However, if they fail to make payments or default, the lender might reduce the limit by a significant limit.

As per the Federal Reserve, the lender must disclose an annual interest percentage of 1/8th of 1 percentage that a borrower needs to pay.

Three types of open-end credit transactions occur daily. It includes credit cards, home equity lines of credit (HELOC), and unsecured lines of credit. The only difference is that HELOC provides a revolving home open-end credit facility. And an unsecured line of credit provides credit without any collateral or security.

History

The origin of open-credit agreements dates back to the mid-20th century in the United States. In the 1920s, U.S-based oil companies and hotels started issuing them to customers for easy purchases without paying cash immediately. Card issuer Diner’s Club, in 1949, became the first lender to issue credit cards as a form of revolving open-end credit facility to customers for flexibility and easy purchases.

In the initial year, the number of borrowers increased by 10,000 across 28 restaurants. However, large-scale use started in the late 20th century. People started making outstanding defaults on payments. The lenders started charging penalties on credit defaults. As a result, during the Great Recession in 2008-2009, financial institutions imposed restrictions and the eligibility to avail of this credit facility.

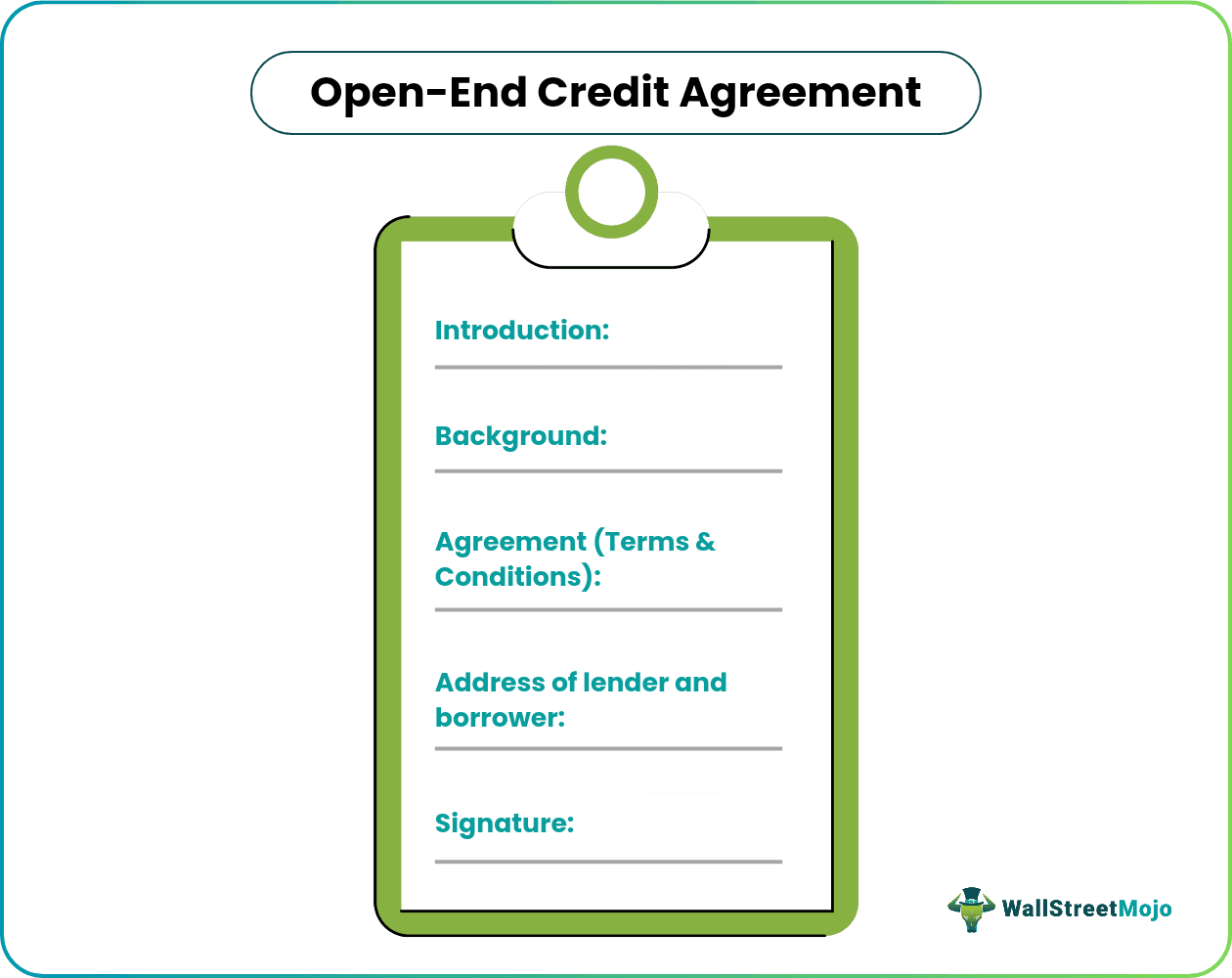

Open-End Credit Template

Let us look at the components of an open-end credit template to comprehend the agreement involved between the lender and borrower:

- Agreement Date And Parties Involved – The date on which the open-end credit agreement becomes effective and the parties’ names are involved.

- Background – Here, the agreement states the borrower’s rights and liabilities. Similar information from the lenders is stated.

- Agreement (Terms And Conditions) – It mentions the approved credit amount, and maximum credit limit. According to the Federal Reserve, the limit is ($2,500,000).

- Interest Rate – It states the interest rate applicable on late payments.

- Repayment Date – A borrower must pay within 30 days of notice to the lender on a timely basis. Otherwise, there will be a penalty issued to them.

- Others – The other details include the termination rights of the borrower as well as the lender, outstanding balances, and others.

Examples

Let us look at a few examples of open-end credit transactions to understand the concept better:

Example #1

Suppose Klestin is an electronics shop owner in England. He wants to bulk purchase refrigerators from the supplier but needs more money. Also, his overdraft facility has exceeded its limit. Thus, he opts for a credit card, a kind of credit facility. Klein made a purchase of $15000 that needs to be paid within a certain period. The lender might charge a penalty or interest if he fails to repay the amount.

Nevertheless, Klein benefits from making payments on time. If he wants to borrow money in the next month, he can do so. Since the open-credit facility is revolving, it gets renewed on the due date.

Example #2

According to a TransUnion report of 2022, more than 1.96 million credit cards have been issued to citizens in the United States. Among them, 20.1 million were new users accessing the open-end credit facility. In November 2022, the number of HELOC users increased by 30% year-on-year this year. Many users have shifted their focus from personal loans to HELOCs for better convenience.

Advantages And Disadvantages

Open-end credit has certain pros and cons. While it offers easy flexibility, users can easily borrow money from lenders. In addition, individuals using credit facilities like credit cards allow them to earn rewards which in turn improve their credit scores. In addition, they also get a revolving credit that facilitates re-borrowing once payment of the earlier transactions is completed.

However, there are certain disadvantages to it as well. Borrowers need to pay high maintenance fees for this facility. Although they do not charge interest on early payments, a penalty is chargeable if it exceeds the due date.

| Advantages | Disadvantages |

|---|---|

| Easy flexibility | Higher maintenance fees |

| Earn rewards | Unexpected terms and conditions |

| Revolving credit facility | |

| Lower interest rates |

Open-End Credit vs Closed-End Credit

Although open-end and closed-end credit provide credit facilities, they have huge differences. The former allows a borrower to borrow cash to a certain limit. Some examples of it include credit cards, HELOCs, and unsecured credits.

In contrast, the latter allows users to access a lump sum amount at the approval they need to pay, along with interest on a future date. However, it acts reverse for the former. If a borrower pays on time, the issuer will not charge any interest. But, if they default, they need to pay the penalty.

| Basis | Open-End Credit | Closed-End Credit |

|---|---|---|

| Meaning | It is a revolving facility that allows re-borrowing up to a certain limit. | A non-revolving facility that enables borrowing only once. |

| Purpose | To enable repeated borrowing until renewal. | To give an instant credit amount for a specific period. |

| Types | Credit cards, HELOCs, unsecured lines of credit. | Personal loans, mortgages, |

| Duration | Suitable for short-term periods | For long-term period |

| Effect on credit score | Timely payments increase the score. | Outstanding debts can decrease the score. |

| Interest applicable | No or lower interest rates | High-interest rates |

| Payment | Monthly payments | On a future date |

| Borrowing | Infinite times up to a limit. | Instant disbursement of credit on approval. |

Frequently Asked Questions (FAQs)

Is a mortgage an open-end credit?

No, it is not. Mortgages and loans fall under the category of closed-end credit, as borrowers cannot borrow again and again. However, in the case of open-end credit, the person can borrow many times, unlike the former, where borrowing happens once.

Is open-end credit the same as buy now, pay later (BNPL)?

No, there is a slight difference between them. In buy now, pay later, individuals get a small credit facility. However, in the former case, the credit limit is higher, allowing them to make huge purchases, which is impossible through BNPL.

Are car loans open-end credit?

No, car loans are a part of closed-end credit, where an individual can get a lump sum amount on approval. As a result, they can access the vehicle and make instant purchases simultaneously.

Does open-end credit involve installments?

No, there is no installment method in this type of facility. A borrower needs to make full payments at once monthly. Otherwise, they will attract a penalty fee for it.

Recommended Articles

This article has been a guide to what is Open-End Credit. Here, we explain its examples, comparison with closed-end credit, advantages, disadvantages, & history. You may also find some useful articles here –