Table Of Contents

What Are the Objectives of Financial Accounting?

The primary objective of Financial Accounting is to reveal the profits and losses of the business and provide a true and fair view of the business, which is aimed at safeguarding the interest of various stakeholders, internal and external, which are connected to the business.

Table of contents

- What are the Objectives of Financial Accounting?

- Objectives of Financial Accounting

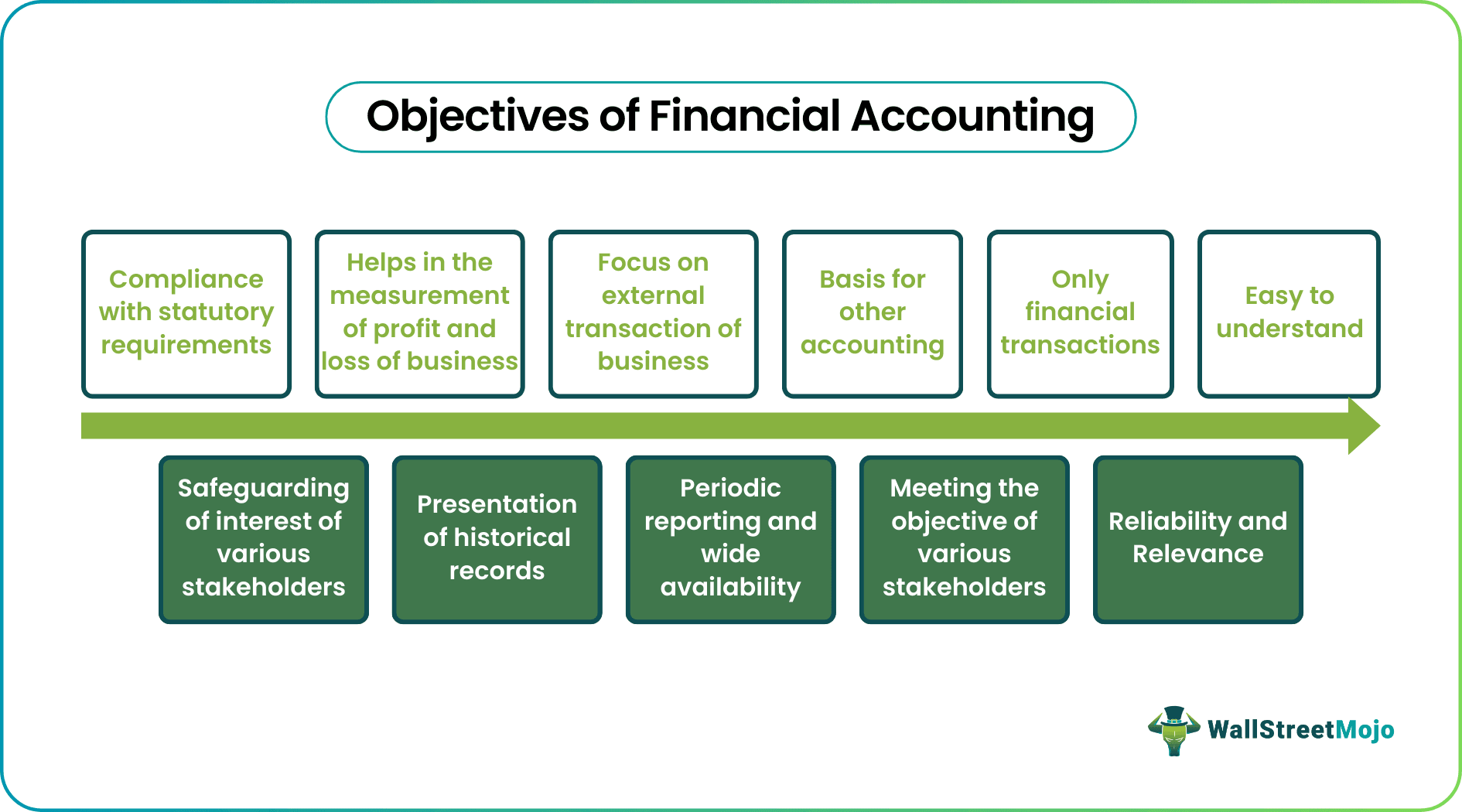

- #1 - Compliance with Statutory Requirements

- #2 - Safeguarding of Interest of Various Stakeholders

- #3 - Helps in the Measurement of Profit and Loss of Business

- #4 - Presentation of Historical Records

- #5 - Focus on External Transaction of Business

- #6 - Periodic Reporting and Wide Availability

- #7 - Basis for Other Accounting

- #8 - Meeting the Objective of Various Stakeholders

- #9 - Only Financial Transactions

- #10 - Reliability and Relevance

- #11 - Easy to Understand

- Conclusion

- Recommended Articles

- Objectives of Financial Accounting

- Financial accounting's main goal is to disclose the company's profits and losses and to present a genuine and fair picture of the company to protect the interests of all internal and external stakeholders that have a stake in the company.

- Financial accounting objectives vary in nature, from compliance with statutory requirements, focus on externalities of a business, stakeholder objectives to be met, etc.

- A predetermined periodic reporting period, typically quarterly, half-yearly, and annually, is used when performing financial accounting. It makes comparisons simple and maintains the information's relevance and educational value for different stakeholders.

- One of the prime aspects of accounting, financial reporting's main goal of creating financial accounts, is to determine whether a business made a profit or suffered a loss during the relevant time.

#1 - Compliance with Statutory Requirements

One of the objectives is to ensure compliance with local laws related to taxation, the Companies Act and other statutory requirements relevant to the country where the business undertakes. It ensures that the business affairs adhere to such laws and relevant provisions comply while business is conducted.

Financial Accounting Video Explanation

#2 - Safeguarding of Interest of Various Stakeholders

It provides suitable and relevant information related to business operations to stakeholders such as Shareholders, Prospective Investors, Financers, customers, and creditors. They are not just appropriate for those who have existing business relationships but also for those who are interested in having future collaboration with the business by providing them with meaningful information about the business. In addition, further financial accounting standards ensure control over accounting policies of businesses to protect the interest of investors.

#3 - Helps in the Measurement of Profit and Loss of Business

It measures the business's profitability for a particular period and discloses the net profit or loss of the business as a whole. It also exhibits the Assets and Liabilities of the business.

#4 - Presentation of Historical Records

Unlike other accounting, it focuses on the presentation of historical records and not on forecasting the future. Therefore, the primary rationale for preparing Financial Accounts is ascertaining profit earned or loss incurred by the business in the period concerned.

#5 - Focus on External Transaction of Business

It focuses on a transaction that the business enters into with external parties, such as customers, suppliers, etc. The accounts are prepared to quantify the business, costs incurred as expenses, and resultant profit or loss earned based on these transactions.

#6 - Periodic Reporting and Wide Availability

Financial Accounting is undertaken with a pre-specified periodic reporting period, usually quarterly, half-yearly, and annually. It enables easy comparison and keeps the information relevant and informative for various stakeholders. Further Financial Accounts are available publicly and are accessible to everyone who wants to know about the business and its performance.

#7 - Basis for Other Accounting

The other types of accounting, namely cost accounting or management accounting, provides their base data from financial accounting. It acts as a source for different types of accounting undertaken by the business. It deals with business transactions broadly, which acts as a base for Cost Accounting to further identify costs with products and services.

#8 - Meeting the Objective of Various Stakeholders

- Another essential objective is meeting the needs of various stakeholders, which are associated with the business. Different stakeholders have different purposes, such as lenders to the business intend to assess the capability of the business to pay interest and principal, which is lent to the business or prospective lenders, so they are more interested in the solvency of the business and focus on that aspect.

- Similarly, customers are interested in knowing the growth and stability of the business and focus more on cash flow statements and financial statements to determine the ability of the business to provide better business terms and a consistent supply of goods and services.

#9 - Only Financial Transactions

Financial Accounting records only those transactions which can be denominated in monetary terms or those which include financial aspects as such non-financial transactions are outside its purview. Accordingly, it serves the objective of only Financial Transactions.

#10 - Reliability and Relevance

An important objective is to prepare reliable financial statements, and decisions can be based on them. For this purpose, such Accounting should represent a faithful representation of transactions and events undertaken by the business, represented in their actual substance and economic reality perspective.

#11 - Easy to Understand

- Among all the objectives discussed above, it is the primary objective that Financial Accounts are prepared so that they are easily understandable by intended users.

- However, while meeting this objective in mind, it must be equally essential to ensure that no material information is omitted because it will be complex and cumbersome to understand for various users. In short, efforts must be made to prepare Financial Accounts in an easy way to know wherever possible.

Conclusion

Financial Accounting serves many objectives and involves recording, proper classification, and summarization of financial transactions and events that a business undergoes to provide relevant and meaningful insights to various users.

It involves a four-step objective cycle, depicted below, and is a critical Accounting branch.

- Step 1: Identifying the Financial Transaction that needs to be recorded. Non-financial transactions are not recorded.

- Step 2: Once a transaction is to be recorded, it should be clubbed in groups with similar characteristics /nature, which involve interpreting the transaction and making a correct journal entry.

- Step 3: Once transactions are recorded and clubbed together, they need to be summarized, enabling various intended users to understand and interpret the business results.

- Step 4: Finally, provide the answer to users of such Financial Statements regarding the profit or loss made by the business (Profit and Loss Account) and the resources on a particular date deployed to make such profits (Balance Sheet).

Frequently Asked Questions (FAQs)

Financial accounting is known as the process of recording, compiling, and reporting the numerous transactions occurring from corporate operations throughout time. It is a particular branch of accounting. This accounting stream's main goal is to depict a company's overall performance appropriately. Additionally, this information is vital information for other parties.

Financial accounting can be challenging or simple, depending on a person's interests. Accounting isn't always simple; there are instances when it calls for sifting through data, putting puzzle pieces together, and locating obscure financial information, particularly when conducting an audit or handling intricate tax computations.

Accounting is a set of procedures business entities use to record their financial transactions. These procedures involve:

Gathering;

Identifying;

Categorizing;

Summarizing, and

Documenting those transactions in the company's books of accounts.

Recommended Articles

This article is a guide to The Objectives of Financial Accounting and its Definition. Here we discuss the top 11 objectives along with detailed explanations. You can learn more about it from the following articles –