Table Of Contents

Nostro Account Meaning

Nostro Account is the account that a country's bank holds in the bank of another country in the foreign currency. It helps the bank which has the account in the bank of another country by simplifying the exchange and trading process for the foreign currencies.

Through nostro account, the banks of one country keep track of the money flowing or being stored in another country. As a result, they can deal with their finances without getting severely affected by the exchange rate risks. In addition, it helps in facilitating transactions involving foreign currencies.

Table of contents

How Does A Nostro Account Work?

Nostro Account is a bank account that a bank in another country opens to store money in the native currency of the former bank. Nostro is a Latin term, which means ours in English. This account is where a bank of one country saves or deposits our (their) money into a bank of another nation in its native currency. It is similar to any individual depositing a money the banks for saving money for future use.

By depositing and saving money in the nostro account, the banks make sure to have a record of the amount they save in the other currency in some other banks. Doing this help the banks of one country to hedge exchange rate risks to a great extent. In addition, banks can invest in assets using international currencies without any hassle.

As not all banks offer convertible currencies to customers, nostro account must be opened carefully preferably with the one that has this feature available. Banks with convertible currency make it easier for the customers to pay for international deals. However, even if the banks of the other country do not offer this feature, the customers can collaborate with third-parties to get the currencies converted and facilitate the transactions on bank’s behalf.

A bank recognizes the Nostro balance in the account as a debit balance with other banks and hence gets recorded as the bank’s assets on the balance sheet. These accounts are not opened in countries on the restricted list or where there is a minimal amount of foreign exchange transactions happening. It is opened by the bank in those countries where the bank’s physical presence is marginal, and it would not be easy to communicate daily. To avoid this discomfort, a bank opens a Nostro account in another bank in a foreign country in foreign currency for flexibility and smooth operations.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Examples

Let us consider the following instances to understand what is nostro account and how it operates:

Example #1

Suppose Bank A in the USA has to buy euros 1,00,000 from Bank B in the UK. On the settlement date, bank b will transfer euros 1,00,000 to the Nostro account in the UK itself. However, a bank must pay dollars for the transactions. Hence Bank A will transfer the required amount in dollars to the Nostro account of bank b in the united states of America. Thus there is no money exchange from one country to another; however, the transaction is executed smoothly.

Example #2

Suppose an Individual, Mr. A, wants to remit $ 1,00,000 to another person, Mr.B, in the USA. In this case, Mr. A will approach his home bank and ask them to open a Nostro account in the correspondent bank in the USA. Now Mr. A will pay ~65,00,000 ( $1 = rs 65 ) to the domestic bank in the Nostro account of Mr. B, and the home bank will pay the corresponding bank in the USA $1,00,000 into its Vostro account. The correspondent bank will pay $1,00,000 to Mr. B's Account from that account. In this way, there is no movement of funds from one country to another. Still, the transactions go through, and both parties are satisfied. MrB gets his money, and Mr. A pays off its obligations.

Example #3

In July 2023, two Bangladeshi banks have opened nostro accounts with Indian banks to carry out trade transactions hassle-freely. Eastern Bank and Sonali Bank of the former nation opened their accounts with the State Bank of India (SBI) and ICICI bank in India to carry out international trade and pay in rupees.

Opening the nostro accounts with Indian banks seems to be a wise step as India is Bangladesh’s second largest source of imports, accounting for $13.69 billion.

Advantages

It is for the one who takes care of the entire financial framework of the company or government. Below are some of the advantages:

- One can pay the money to a third party in your home currency without any exchange rate risk.

- It is easier to operate since it is a mere transfer of funds from one account to another in the same bank.

- These accounts enable to keep funds in foreign currency.

- It reduces the excessive fluctuation risk in exchange rates since money is directly emitted to the other party without physically being there.

Disadvantages

Though there are multiple merits of having nostro accounts, there are some restrictions that the banks of nations must know of before opening an account at foreign banks. Below are some of the disadvantages. Let us have a look at them:

- A lesser rate of interest as compared to savings or current account.

- It is generally more expensive since it is a facility provided by the home bank to execute foreign exchange transactions smoothly.

- Rigorous regulations and laws were imposed for the operation of the Nostro account by the federal bank;

- It is open to cyberattacks, which can have a huge impact on the bank's cash reserves if hacked.

Nostro Account vs Vostro Account

Nostro and Vostro Accounts are the essential components of the financial system since they help execute large foreign exchange transactions without having any physical presence in other countries. A nostro account for one nation is the vostro for the other. Hence, both the terms are relevant for the same entity, the only thing that differs is how it is seen from the other end. However, for one country, a nostro and a vostro account will always be two different entities. So, let us check the differences between the two:

- Nostro, a Latin word, means ours in English, while Vostro, another Latin term, means yours in English. This implies that for an entity, an account is a nostro type when bank saves “our” money into “your” bank. On the other hand, an account is vostro, if “your” deposits or money saved are in “our” banks.

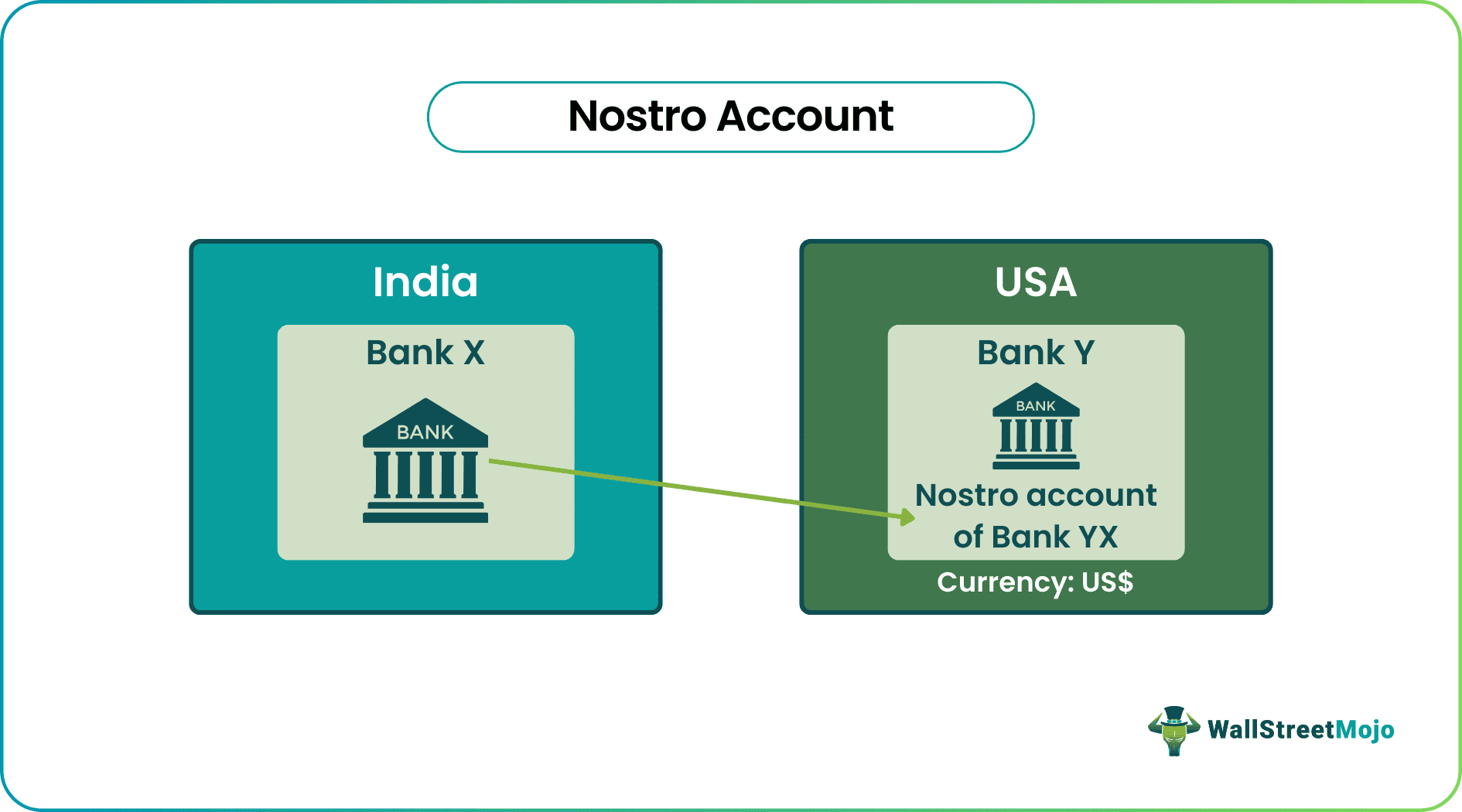

- For example, Bank X in India holds an account with the bank in Y in the USA in their home currency, i.e., Dollars. In this scenario, bank X has opened a Nostro account in another bank Y in a foreign country where there are many foreign exchange transactions periodically. Alternatively, the same is a Vostro account for “our” Bank Y that keeps “your” i.e. Bank X’s money in it.

- Nostro accounts reflecting debit balance fall under cash assets, while vostro accounts with balance in credit become liabilities.

- In nostro accounts, the domestic banks are facilitators, i.e., they maintain the accounts, while for vostro accounts, the foreign banks facilitate transactions and maintain them.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This article has been a guide to Nostro Account & its meaning. Here, we explain its examples, differences with vostro account, advantages, & disadvantages. You can learn more about accounting from the following articles –