Table Of Contents

What Is Normal-Course Issuer Bid (NCIB)?

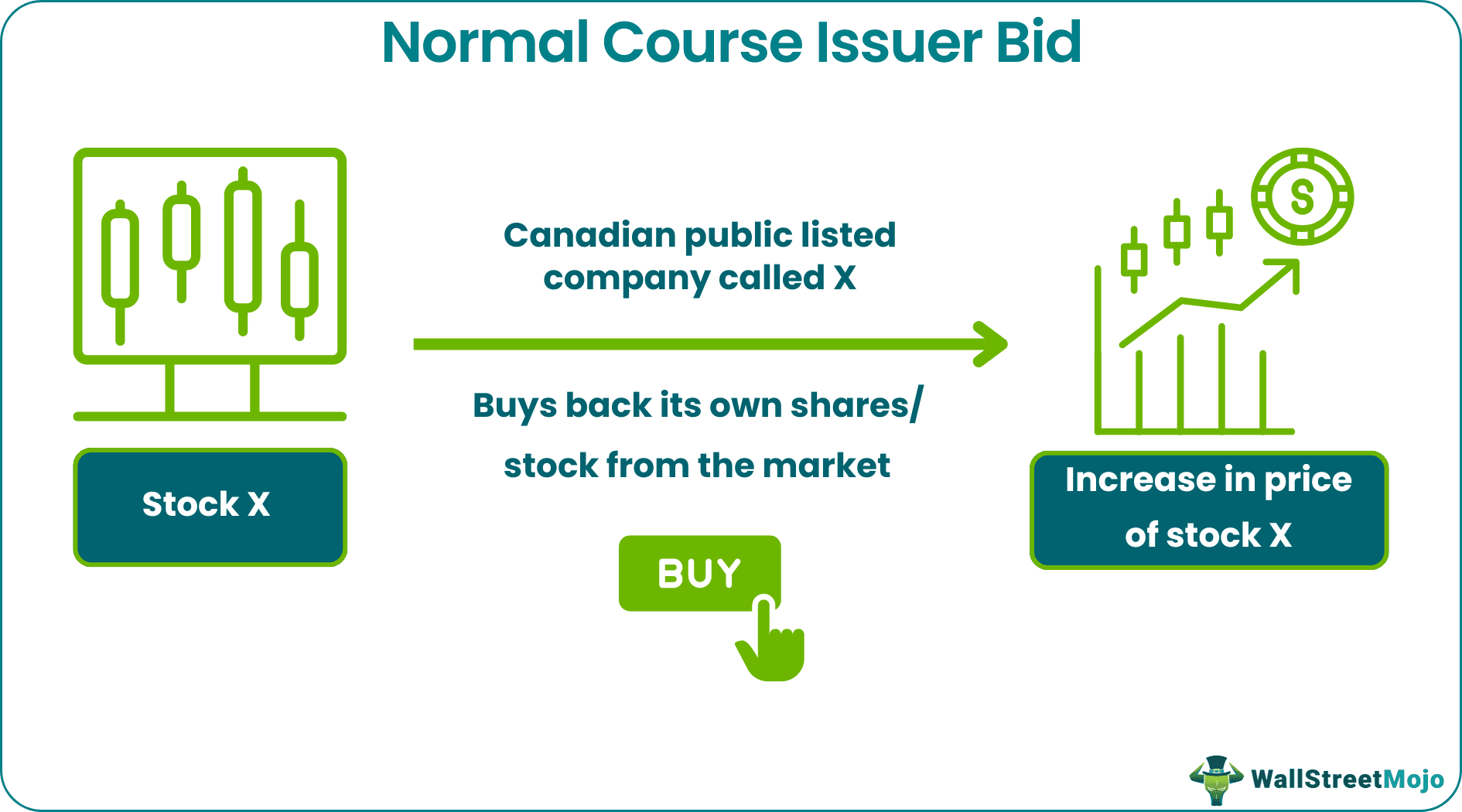

The Normal-Course Issuer Bid (NCIB) is a stock buyback program in Canada wherein publicly-listed companies can repurchase a portion of their own outstanding shares in line with certain marketplace and regulatory restrictions. The goal is often to return value to shareholders by reducing the number of shares in circulation and boosting the company’s stock value.

An NCIB sends a positive signal to the market, indicating that the company believes its stock is undervalued. This vote of confidence boosts investor confidence and drives up the stock price. Additionally, since the total number of outstanding shares decreases, future earnings get distributed among a smaller pool that increases the overall Earnings Per Share (EPS).

Table of contents

- What Is Normal-Course Issuer Bid (NCIB)?

- Normal-Course Issuer Bid (NCIB) is a program approved by stock exchanges and other relevant regulatory bodies that allows publicly listed companies to repurchase their own shares from the market over a specified period.

- The term normal course indicates that the company is buying back shares as part of its regular operations rather than for a specific event or purpose.

- NCIBs are conducted under regulatory guidelines to ensure transparency and fairness in the market.

- NCIBs involve ongoing repurchases of a limited percentage of shares over an extended period, while SIBs are a one-time offer with a fixed price and maximum repurchase limit.

How Does Normal-Course Issuer Bid Work?

Normal-Course Issuer Bid (NCIB) is a term used in Canada to describe a company's repurchase of its own stock with the intention of canceling it. The buyback-induced scarcity of the company’s shares in the market makes the company’s shares desirable to investors. The percentage of shares a company is permitted to repurchase typically ranges from 5% to 10%, depending on the specifics of the transaction. This process has various impacts on the company's financial structure and shareholder value.

Let us study how NCIB is administered.

- Application and Approval: A company must file a notice of intention to make a normal-course issuer bid with the stock exchanges on which it is listed. This notice outlines the number of shares it intends to buy and the time frame for the buyback. The stock exchange needs to approve this before the company proceeds with the repurchase.

- Buying Shares: There are two approaches to an NCIB. One is to buy shares from the open market within specified limits to avoid affecting the market. The other approach involves purchasing shares directly from shareholders at a price and date fixed beforehand. If all outstanding shares are bought, the company becomes private.

- Disclosure: If restricted shares are involved, the voting rights of all shares must be clearly outlined in the notice of intention. Failure to provide this information requires stating the reasons for not including it.

- Execution: Once approved, the company can repurchase its stocks and securities as it sees fit during the period communicated or proposed for repurchase. The company can choose not to buy all the shares it is allowed to, which happens more often than not.

- Reasons for NCIB: Typically, companies initiate NCIBs when their publicly traded shares are undervalued. Repurchasing shares decreases the available supply, potentially leading to increased demand and higher stock prices.

- Liquidity and Investor Base: When the stock reaches a desired value, the company can sell some of its shares to expand its investor base, raise capital, and enhance liquidity.

- Seizing Opportunities: An NCIB allows a company to take advantage of discounts on its share prices, providing an opportunity to buy back shares at lower prices.

Overall, an NCIB provides companies with a strategic tool to manage their capital structure, enhance shareholder value, and respond to market conditions. It is a way for companies to signal confidence in their own stock and potentially influence its valuation.

Examples

Let us look at some normal-course issuer bid examples to understand the concept better.

Example #1

Suppose ABC Corporation, a publicly-listed Canadian company, believes its stock is currently undervalued in the market. To take advantage of this, the company initiates a Normal-Course Issuer Bid (NCIB). They plan to repurchase up to 7% of their outstanding shares over the next 12 months. By doing so, ABC Corporation aims to reduce the number of shares in circulation and potentially boost its stock's earnings per share. This move reflects the company's confidence in its own stock and its commitment to enhancing shareholder value. In this way, NCIB can help companies achieve goals that support their operations.

Example #2

The Toronto-Dominion Bank (TD) has received regulatory approval from the Toronto Stock Exchange (TSX) and the Office of the Superintendent of Financial Institutions Canada (OSFI) for its normal-course issuer bid. TD plans to conclude its existing normal-course issuer bid and launch a new bid, aiming to repurchase and cancel up to 90 million of its common shares. The last bid, called the Existing Bid, ended on August 30, 2023, and the New Bid began on August 31, 2023, to either continue until August 30, 2024, or maybe to close at an earlier date chosen by TD.

Around 4.95% of the public float of 1,817,917,586 common shares as of August 21, 2023, were available for repurchase. It was the cap or upper limit, i.e., the maximum number of shares eligible for repurchase under the new bid. Repurchases will be processed through the TSX and other designated exchanges, and the repurchased shares will be canceled.

The repurchase plan underscores TD's commitment to enhance shareholder value and its confidence in its stock.

How To Make?

Making a Normal-Course Issuer Bid (NCIB) involves several key steps. Here is a general outline of the process:

- Board Approval: The board of directors of the publicly listed company must approve the decision to initiate an NCIB. This involves determining the number of shares the company intends to repurchase and setting a budget for the buyback.

- Notice of Intention: Companies prepare a Notice of Intention, which is required to initiate NCIB for publicly-traded companies, following the guidelines in Section 6 of the policy. The board of directors must specify the number of shares to be acquired. However, if the company does not intend (immediately) to purchase securities, the Notice of Intention is not necessary. If companies do not meet the listing requirements, the relevant exchange(s) will not approve the notice even after the purchases are completed. The NCIB process should not extend beyond one year from the start of purchases.

- Exchange Approval: Companies are required to submit the Notice of Intention to the appropriate stock exchange(s) for approval. The exchange will review the notice to ensure it complies with the exchange's regulations and policies.

- News Release: Once the exchange approves the Notice of Intention, companies must inform the public and shareholders about the company's intention to execute the NCIB through a press release. The news release should include key details like the number of shares to be repurchased, the reasons for the buyback, and the intended start and end dates.

- Disclosure to Shareholders: Companies must send out clear communications to shareholders about the NCIB through company reports and disclosures. Sharing information about the progress, rationale, and potential impact on the company's financials and stock value is crucial.

- Amendment: If needed, companies must make amendments to the notice. A company can adjust the number of shares to be purchased within the policy's prescribed limits. If the NCIB is significant or large enough, it might alter the stock ownership dynamics. If such changes occur, third parties may enter the picture and bring ownership-related challenges. To prevent this, amendments are needed to potentially allow the company to regain or retain a controlling interest in its stock ownership.

By following the steps listed above, companies ensure compliance with regulations, ascertain effective communication with shareholders, and oversee the proper execution of the NCIB.

NCIB Renewal

The renewal of a Normal-Course Issuer Bid (NCIB) allows a publicly listed company to extend or continue its share repurchase program beyond its initial term. This process involves the company submitting a new Notice of Intention to the relevant regulatory authorities, such as the stock exchange where the company is listed. The renewal allows the company to continue repurchasing its own shares within the regulatory guidelines for an additional period. It is a strategic decision made by the company's board of directors based on factors like market conditions, the company's financial position, and its long-term goals.

Normal-Course Issuer Bid vs Substantial Issuer Bid

The differences between normal-course issue bid and substantial issuer bid are enumerated in the table below.

| Aspects | Normal-Course Issuer Bid (NCIB) | Substantial Issuer Bid (SIB) |

|---|---|---|

| Scope | NCIB involves a company repurchasing a portion of its outstanding shares over an extended period, often up to a year. | SIB involves a company making a one-time offer to repurchase a significant number of its shares directly from shareholders and distribute excess funds among them. The SIB repurchase quantum is typically over and above the limit permitted under NCIB. |

| Percentage Limit | The repurchases in an NCIB are usually limited to a certain percentage of the company's outstanding shares, commonly ranging from 5% to 10%. The specific percentage depends on regulatory guidelines and stock exchange rules. | There is no fixed percentage limit in an SIB. Instead, the company states the maximum number of shares it intends to repurchase. |

Frequently Asked Questions (FAQs)

NCIB is good or bad depending on the company's financial health, strategic goals, market conditions, and the effectiveness of its implementation. It is important for companies to carefully evaluate their motivations, financial position, and potential impact on shareholder value before proceeding with an NCIB.

Normal-Course Issuer Bid on the TSX is a regulated program that allows companies to buy back their own shares from the market. This can be done to enhance shareholder value, signal confidence in the company's stock, and adjust the company's capital structure. It is important for companies to follow the TSX's rules and regulations when executing an NCIB to ensure transparency and fairness in the market.

To participate in a Normal-Course Issuer Bid (NCIB), individuals do not directly “join” like they would if it were an investment. An NCIB is initiated by a company, not individuals. If an investor owns shares in a company conducting an NCIB, their ownership might be affected as the company buys back its own shares from the market. This could potentially increase the value of the investor’s shares due to reduced supply. Investors do not actively join; instead, the value of their shares might benefit from the buyback.

Recommended Articles

This article has been a guide to what is Normal-Course Issuer Bid (NCIB). Here, we compare it with substantial issuer bid, explain its examples, and how to make it. You may also find some useful articles here -