Table Of Contents

Neobank Meaning

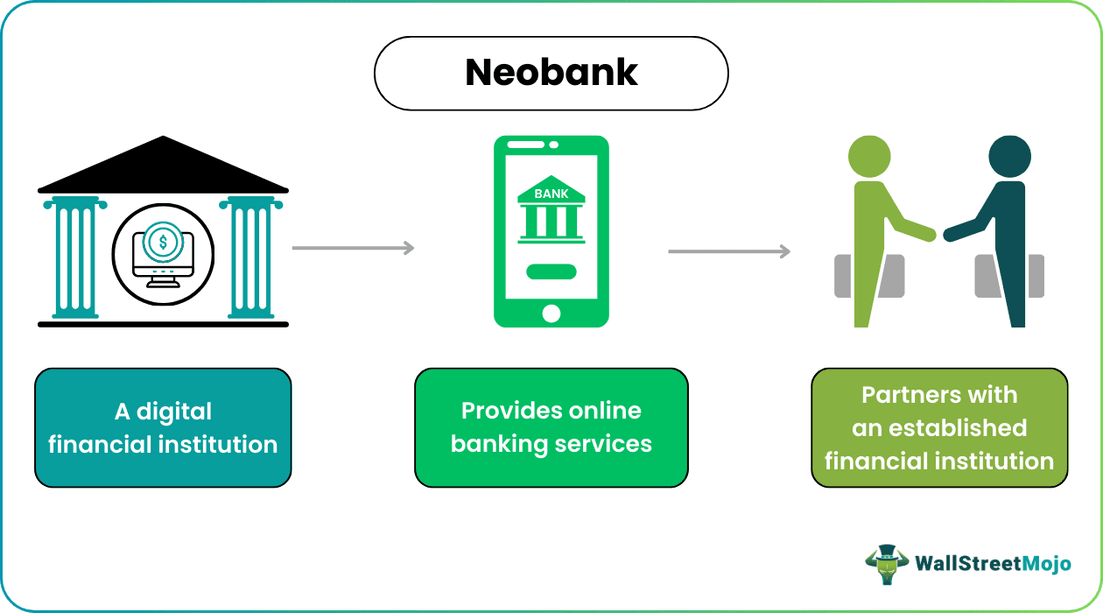

A neobank is a financial institution that operates digitally, without any physical branch locations. These platforms provide online banking services to its customers by partnering with an established banking institution. They aim to simplify and modernize the banking experience by offering convenient, cost-effective, and highly accessible services while ensuring compliance with relevant regulations.

These innovative banking entities provide a range of financial services, including checking and savings accounts, payment processing, and loans, through user-friendly mobile apps and web platforms. They use advanced technology, including artificial intelligence and data analytics, to offer personalized financial solutions and quick, hassle-free transactions.

Table of contents

- Neobank Meaning

- A neobank is a digital financial institution that functions without any physical branch locations. They offer online banking services and ensure regulatory compliance by partnering with an established financial institution.

- They enhance the banking experience for users by using advanced technology. The platforms offer easy accessibility and cost-effective financial services.

- However, the platforms operate online, which may not be suitable for customers who prefer face-to-face interactions for banking.

- Furthermore, they are highly dependent on technology, and users may face technical errors, security issues, and data breaches.

Investors seeking a comprehensive platform may consider Saxo Bank International for a variety of account types and investment options.

Neobank Explained

A neobank is a digital bank that operates entirely in the digital world, with no physical branches. It represents a modern and tech-savvy version of traditional banking. They . Customers can access all their banking services through user-friendly mobile apps or web platforms from the comfort of their smartphones or computers. These digital banks offer a wide range of financial services like checking and savings accounts, payment processing, loans, credit cards, and investment options. Moreover, they focus on a seamless, efficient, and often cost-effective customer experience.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

These financial institutions use advanced technologies like artificial intelligence, data analytics, and automation to enhance the banking experience for their users. For instance, they use AI algorithms to offer personalized financial insights and recommendations to their users. This level of personalization enables customers to manage their finances more effectively, optimize savings, and make more informed investment decisions.

They are also known for their straightforward, transparent fee structures. Many such platforms offer fee-free or low-fee accounts, reducing or eliminating standard charges like monthly maintenance fees, ATM fees, and foreign transaction fees. This fee transparency is appealing to customers who seek to avoid unexpected costs and save money.

Examples

Let us study the following examples to understand this platform:

Example #1

Suppose Amy is a tech-savvy individual who uses the services of a neobank. She downloaded an app on her smartphone, which became her go-to financial tool. The app offered a clever budgeting tool that helped Amy monitor her spending. Whenever she made a purchase, the app rounded up the amount to the nearest dollar and saved the spare change in her savings account. Moreover, Amy could pay her bills, send money to friends, and get a small loan when needed without the hassle of paperwork or visiting a physical bank.

Example #2

PoetrYY Finance, a neobank, started operations. Its goal is to change the way that individuals, small enterprises, and communities with limited access use financial services. PoetrYY Finance utilizes the innovative Banking-as-a-Service (BaaS) technology from Mbanq to provide innovative, safe, and accessible financial solutions. With complete financial services and solutions like debit cards, checking accounts, and peer-to-peer payments, the organization stands out as an icon of financial empowerment.

Conventional banking services are effortlessly incorporated into an easy-to-navigate, mobile-friendly platform that includes modern biometric technology for greater security. PoetrYY Finance uses mobile and digital technology, and its services are oriented toward small and medium-sized businesses, with a focus on underprivileged communities.

For efficient cross-border payments, many individuals and businesses use the Wise Money Transfer UK or Wise Money Transfer US services for transparent and low-cost transfers.

Benefits

Some benefits of neobank technology are:

- These platforms are easily accessible through user-friendly mobile apps or web platforms. They allow customers to manage their finances from anywhere with an internet connection.

- Many such platforms have transparent fee structures that often waive standard charges like monthly maintenance fees, ATM fees, and foreign transaction fees. This fee transparency helps users save money and avoid unexpected costs.

- They usually excel in processing times for transactions and payments. Money transfers and bill payments are executed quickly, enabling users to move funds rapidly and manage their financial affairs more efficiently.

- The neobank platforms utilize data analytics and artificial intelligence to provide personalized financial insights and recommendations to users. These insights can include budgeting suggestions, investment options, and savings strategies tailored to individual financial goals, helping users make informed decisions about their money.

- They often introduce innovative tools and features such as goal-setting, early salary access, expense tracking, and easy integration with financial apps and services. These features allow users to set and track goals and save more effectively.

Risks

The risks associated with neobank platforms are:

- They operate exclusively online, implying they lack physical branch locations. This can be a drawback for customers who prefer in-person interactions for services like cash deposits, face-to-face consultations, or dispute resolution.

- The platforms are often startups. They may lack the extensive regulatory history and trust associated with established banks. Ensuring the safety of deposits and compliance with financial regulations can be a concern.

- They rely heavily on technology, which makes them vulnerable to technical glitches, outages, or cyberattacks. Users might face difficulties accessing their accounts or conducting transactions during such disruptions. Data breaches and cybersecurity issues are also some significant concerns.

- Many neobank technologies are startups or relatively small in scale, and their long-term sustainability may be uncertain. Some may struggle to secure funding or achieve profitability, which could affect their ability to provide consistent and reliable services to customers.

Neobank vs Digital Bank

The differences between the two are as follows:

Neobank

- They are highly technology-driven and often prioritize user-friendly mobile apps and online platforms.

- These services are known for their customer-centric approach, offering streamlined, user-friendly interfaces and innovative features. They prioritize convenience and often introduce unique tools like budgeting apps and savings options.

- They offer transparent fee structures, with reduced or eliminated standard banking fees like monthly maintenance charges and foreign transaction fees. This can make them more cost-effective for users.

Digital Bank

- Digital banks are traditional banks that provide online and mobile banking services in addition to their physical branches. They offer a broader range of financial products and services.

- The banks combine traditional banking services with digital offerings. They maintain physical branches for in-person transactions and consultations while offering online and mobile access to accounts and services.

- Customers of digital banks have the flexibility to choose between digital and in-person banking. They can access a network of physical branches and ATMs when needed while enjoying the convenience of online banking.

Neobank vs Challenger Bank

The differences between the two are as follows:

Neobank

- They are typically tech-centric startups that provide banking services through mobile apps or web platforms.

- They may not have a banking license themselves and rely on partnering with established banks for regulatory compliance and deposit insurance.

- The platforms cater to specific niches or segments of the market, like small businesses, freelancers, or individuals seeking innovative and personalized financial solutions.

Challenger Bank

- Challenger banks are innovative, tech-savvy financial institutions that challenge traditional banks by providing a range of digital banking services. They often have banking licenses and operate independently without the need for partnering with established banks.

- The banks aim to provide a wide variety of financial products and services, including savings and checking accounts, loans, credit cards, and investment options.

- These banks have their banking licenses and regulatory infrastructure. They are subject to the same regulations as traditional banks, which can provide users with more confidence in their services.

Neobank vs Traditional Bank

The differences between the two are as follows:

Neobank

- They prioritize technology and innovation and use advanced tools like artificial intelligence and data analytics to deliver personalized financial solutions and user-friendly interfaces.

- The platforms usually offer a narrower range of financial products. They do not offer services like mortgages or investment options.

Traditional Bank

- Traditional banks have physical branch locations, offering in-person services for activities like cash deposits, withdrawals, and consultations. This can be advantageous for users who prefer face-to-face interactions.

- These banks provide a wide range of financial products and services, including savings and checking accounts, loans, mortgages, credit cards, wealth management, and investment options.

- They offer a hybrid model, combining in-person and digital services. Customers can choose between online and physical branch banking , providing flexibility.

Want a smarter way to bank on the go? Revolut offers a user-friendly app with global access, crypto and stock trading, and innovative budgeting tools—all in one powerful platform.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. How do neobanks make money?

These platforms generate revenue through various means, primarily due to their tech-savvy and agile approach. They earn income through interchange fees when customers use their debit or credit cards for transactions where the merchants cover these fees. Moreover, they accrue interest income by investing customer deposits in safe, interest-bearing assets. Additionally, offering loans and charging interest on them is another revenue source. Furthermore, premium or subscription-based services, with enhanced features for a fee, attract users willing to pay for extra benefits.

2. Can neobanks lend money?

Yes, these platforms can lend money. The neobanks, like traditional banks, can offer loans and credit services to their customers. They evaluate loan applications and, if approved, disburse funds to borrowers. They charge interest on the borrowed amount. These loans can take various forms, including personal loans, business loans, and credit lines, and the terms and conditions may vary.

3. Are neobanks regulated?

Yes, neobanks are subject to financial regulations and oversight. They often partner with traditional banks to access the necessary regulatory infrastructure. The banks themselves are not exempt from compliance. They must adhere to anti-money laundering and know your customer regulations to prevent fraud and illicit activities.