Table Of Contents

What Is A Negative Pledge?

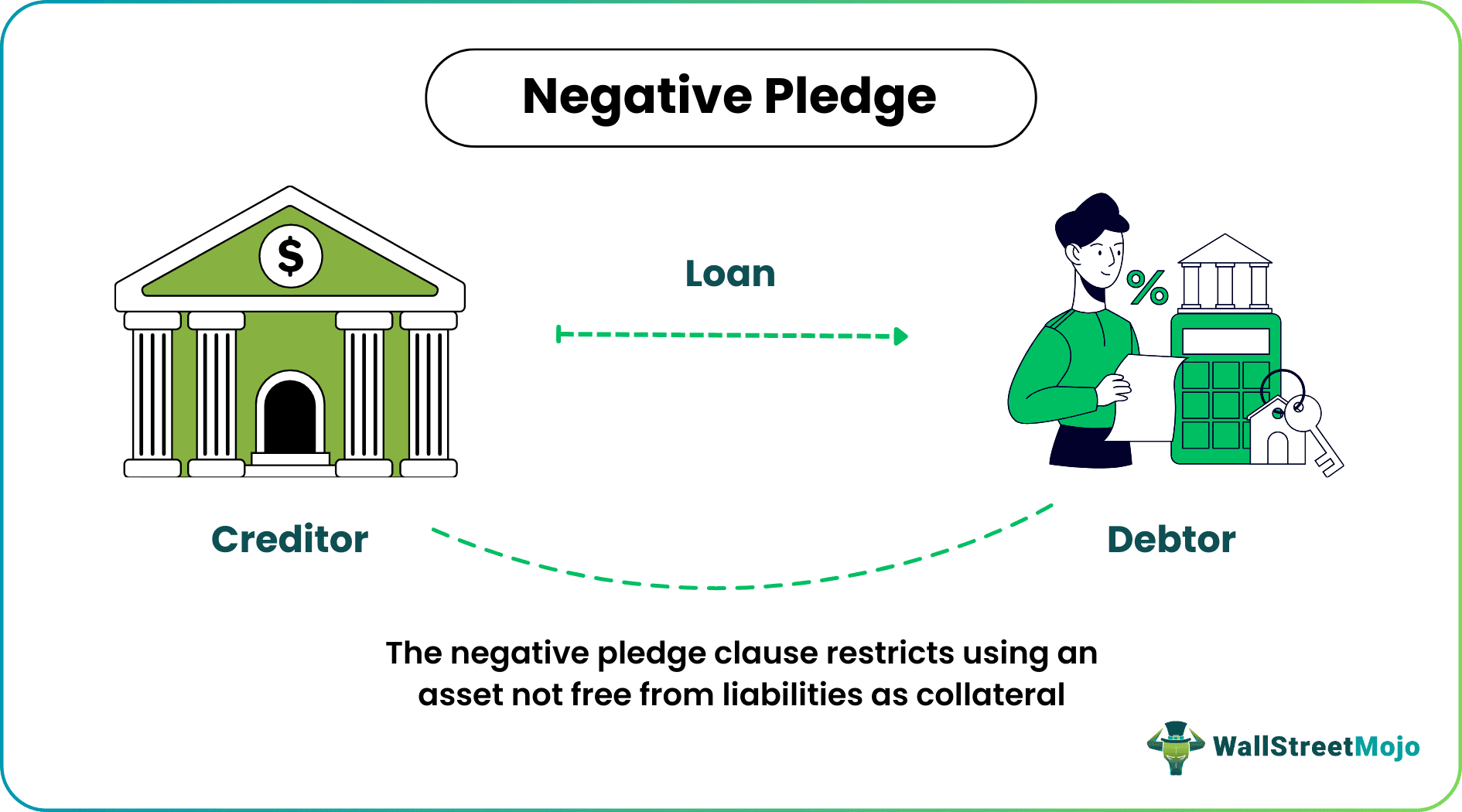

A negative pledge refers to a clause or provision in a contract restricting the debtor from using an asset not free from liabilities as collateral. It also restricts the use of an asset as collateral twice. Thus, it is a type of negative covenant.

To secure debt obligations and reduce disputes, a negative pledge clause can be found in various contracts, including mortgages, bond indentures, and other loan agreements. However, a technical default is not always automatically triggered by breaking the covenant, as the precise consequences of a breach of the negative pledge clause can depend on the specific terms of the agreement.

Key Takeaways

- A negative pledge is a contractual provision in a loan agreement that restricts a borrower from using the same collateral to secure additional loans or financing without the lender's prior consent.

- Its purpose is to provide added security to the lender by ensuring they have a priority claim on the collateral in the event of a default by the borrower.

- It can be recorded in public records to provide evidence of the restriction and to make it legally binding.

- It is not a security but a contractual provision in a loan agreement. It does not represent ownership or a right to receive future income or benefits.

Negative Pledge Explained

Negative pledge covenants are an important consideration in borrowing and lending. The rise of fraudulent activities has led to the development of various remedies, including the use of collateral or security for loans. However, lending based on collateral assurance predates using negative pledge covenants, as lenders have sought security for their loans for many centuries.

Negative pledge covenants serve a different purpose: to prevent the borrower from pledging the same assets to multiple creditors, thereby diluting the security for the original creditor.

Many people use the same collateral to borrow multiple debts. Thus, even if the asset used as collateral is worth $100,000, borrowers could borrow the significant amount they wanted using it. So, who will have the major claim to the asset if the borrower becomes bankrupt? Is it the lender who lent first? Or the lender who lent the most? Or should it be divided equally, if not proportionately? Such questions paved the way for covenants of equal coverage.

This clause is a legal option used to secure the debt owed to a creditor. It typically prohibits the borrower from pledging the same assets as collateral for additional loans or encumbering the property without the lender's knowledge, which helps to protect the lender's security. If the borrower defaults or becomes bankrupt, the lender may be able to seize the collateral as a means of repayment. However, the precise terms of this clause and the legal process for enforcement can vary depending on jurisdiction and the specific terms of the agreement.

Added to this, strict adherence to the clauses is mandatory. If the borrower attempts a breach of covenants, it involuntarily leads to a technical default, and the property will be seized. The borrower will face legal actions and might even be marked unfit for credit. Consequently, they will not be able to borrow anymore. It can happen even if the borrower makes regular and timely interest payments towards the loan.

Examples of Negative Pledge

Let's look into some of the examples to understand the concept better:

Example #1

Rachel purchases a house by taking a loan from HiMoney Bank. The bank inserts a negative pledge clause on the mortgage contract clearly stating the following:

- The house cannot be sold without prior information to the bank.

- She cannot borrow another loan without prior intimation to the bank.

- Rachel cannot encumber the house.

- The house cannot be used as collateral for other loans, credit, or activities.

These are restrictive covenants prohibiting Rachel from doing certain activities. Hence, they are negative pledge clause examples.

Example #2

The U.S. Federal Reserve has been increasing interest rates in its battle against inflation. Higher interest rates discourage borrowing and, thus, spending. However, as interest rates keep climbing, it proves dangerous for the economy, especially small businesses.

The interest rates for small business loans are expected to reach 9% by the end of 2022. It can hamper expansionistic activities. But another issue is the tightened lending standards which have led to a breach in debt covenants specifically based on certain lending requirements, such as financial ratios. Negative pledge issues, too, can arise if the situation grows severe. It could lead to default, further exposing small businesses.

Applications

The applications are usually found in the following areas:

- Banking – For any loan offered with collateral.

- Real estate – For mortgages with the property itself as the collateral.

- Bond indentures – For companies to not take up future debt that would hamper their ability to pay back to the existing bondholders.

Advantages And Disadvantages

Let's discuss the pros and cons of a negative pledge covenant.

Advantages

- Improved security for lenders: Negative pledge clauses provide added security by prohibiting borrowers from pledging the same collateral to secure other loans.

- Priority claim on collateral: Lenders with a negative pledge clause have a priority claim on the collateral in the event of a default by the borrower.

- Increased confidence in loan agreements: Including a negative pledge clause can increase confidence in the loan agreement and make it more attractive to potential lenders.

- Clarity on collateral ownership: Negative pledge clauses provide clear ownership of the collateral, reducing the potential for disputes.

- Improved credit rating: A negative pledge can improve the borrower's credit rating by demonstrating a willingness to provide additional security for loans.

Disadvantages

- Limited flexibility for the borrower: It restricts the borrower's ability to pledge additional collateral for securing new loans.

- Increases borrowing costs: Negative pledge provisions can make borrowing more expensive for the borrower.

- Complex legal structure: Negotiating and implementing a negative pledge clause can be complex and time-consuming.

- May not be enforceable: In some jurisdictions, negative pledge clauses may not be legally enforceable, undermining their effectiveness.

- Potential for disputes: Negative pledge clauses can lead to disputes between the borrower and lenders if there is an ambiguity or clarity in the language used.

Frequently Asked Questions (FAQs)

No, a negative pledge is not a security. It is a contractual provision in a loan agreement that restricts a borrower from pledging the same collateral to secure other loans without the lender's prior consent. It provides added security for the lender by giving them a priority claim on the collateral in the event of a default. On the other hand, security is a financial instrument, such as stocks, bonds, or options.

Yes, it can be recorded in public records to provide evidence of the restriction on the use of collateral and to make it legally binding. It can be done by filing a document, such as a UCC-1 financing statement, with the relevant government office or registry, such as the Secretary of State in the United States.

A negative pledge on real estate refers to a provision in a loan agreement or a mortgage contract that restricts a borrower from using the same property as collateral for securing additional loans or financing without the lender's prior consent. It typically requires the borrower to sign a document that acknowledges the restriction and makes it legally binding.