Table Of Contents

Musharakah Meaning

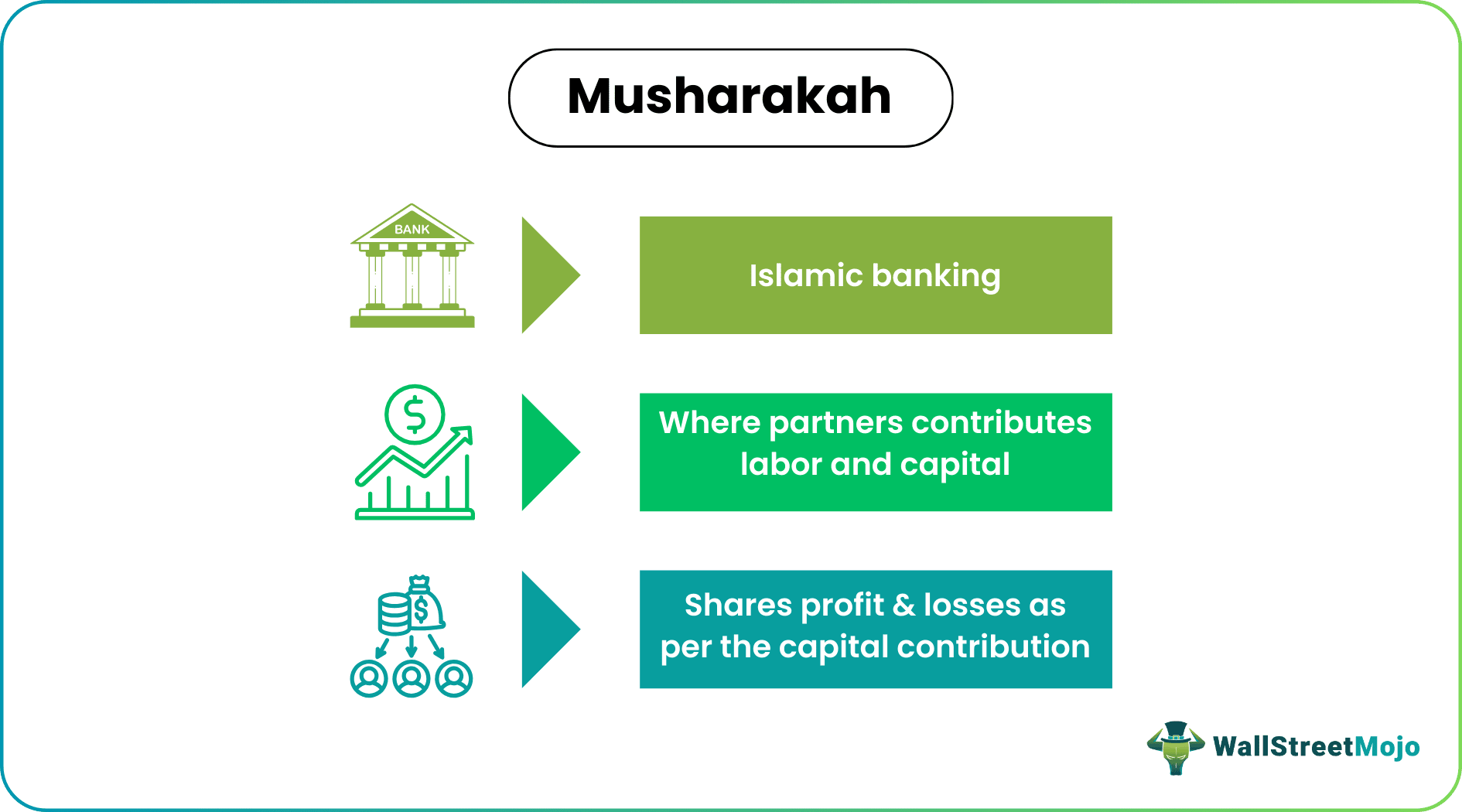

Musharakah refers to a type of Islamic banking where two or more partners contribute their labor or capital to a business to share the profit in a pre-decided ratio and bear the losses as per the share of their contribution. Therefore, the purpose is to promote participants' cooperation, risk-sharing and ethical business practices.

All the partners can participate in the business's management, but it is not mandatory. Musharakah is used for long-term financing, making working with a loan easy due to the absence of interest. Furthermore, it is not legally binding, so any partner can quit the agreement. Moreover, it is based on equity, sharing, and cooperation principles.

Key Takeaways

- Musharakah is a form of Islamic banking in which two or more partners invest their time or money in a company in exchange for a predetermined profit split and a proportional share of the losses.

- It fulfills the primary goal of avoiding interest-based financing by facilitating the division of profit or loss among the business partners according to a specified ratio.

- They are of the following types: Shirkah al-Milk, Ikhtiari, Shirkah al-Aqd, Shirkat-ul-amwal, Shirkat-ul-A'mal, Shirkat-ul-wujooh, Permanent Musharakah, & Diminishing Musharakah.

- These allow every business partner to invest in the business, whereas Murabaha allows only the rab-ul-maal to invest.

How Does Musharakah Work?

Musharakah is an arrangement in Islamic finance where the profits and losses are shared. The word means sharing in Arabic, and its concept is used as a framework of partnership between two or more individuals in a business. Under this method of financing, partners get profits as per their share of investment and share the loss equally occurring in the company. Islamic economists and jurists widely advocate and accept musharakah as the best Islamic financing because it avoids interest-based banking and abides by the shariah law.

Moreover, it is the best financial instrument to invigorate the economy based on Islamic principles. The rate of return does not remain fixed but depends on the profit or loss earned jointly by the joint business venture. Therefore, banks using it usually adopt the floating interest rate, which is based on a firm's rate of return. That component in the musharakah in Islamic banking represents the returns of a lending partner.

Hence, here's how the musharakah agreement works:

- Partnership Formation: The partners agree to enter into a Musharakah contract. Each partner contributes capital or assets to the partnership. The contributions can be in the form of cash, property, or expertise.

- Profit and loss Sharing: The partners agree on the distribution of gains and losses. Hence, the distribution is based on the ratio of their respective capital contributions or any other mutually agreed-upon arrangement.

- Decision-making and Management: In this contract, all partners have the right to participate in the management and decision-making process of the business. Significant decisions are typically made by mutual consultation.

- Termination of the Musharakah: Partners can terminate the Musharakah partnership upon fulfilling the business objectives, the expiration of the agreed-upon period, mutual agreement, or any other conditions specified in the partnership agreement.

Types

There are different types of Musharakah in Islamic finance. Here are three common types:

1. Shirkah Al-Milk Or Partnership In Joint Ownership

It relates to shared ownership of a property or asset between more than two persons.

2. Shirkah Al-Aqd Or Contractual Partnership

It means a type of mutual contract leading to a partnership between more than two persons for business-related financing.

They are further divided into three types:

- Shirkat-ul-amwal or contractual partnership

It is the most common form of shirk, which partners use to invest jointly in a commercial project.

- Shirkat-ul-A'mal or liability partnership

It refers offering of services to customers jointly by the partners at specific fees from the customers. Hence, the partners distribute the total costs collected among themselves.

- Shirkat-ul-wujooh or vocational partnership

It is based on the goodwill of partners. Here partners invest their goodwill and not through any capital. As a result, they equally share the profit between themselves.

3. Permanent Musharakah

Under this type of Islamic financing, Islamic banks participating in a project's equity get their share of the profit on a pro-rata basis. Moreover, it goes on for a long time till the partners want it. Therefore, it is suitable for long-term financing of projects having long gestation periods.

4. Diminishing Musharakah

Although it resembles permanent musharakah, Islamic banks' equity in a project progressively decreases until the ownership of the asset transfers to the partner owners. Here the investor bank gets dividends over their equity in the project while the investor keeps purchasing a small part of the asset. As a result, the project progressively reduces the bank's equity to zero, rendering the bank a non-partner in the project.

Examples

Let us learn more about musharakah using a few examples.

Example # 1

Suppose Alice and Bob decide to start a clothing business together. They both contribute an equal $50,000 as capital to establish the business. Moreover, they agree to share the profits and losses equally.

With the $100,000 capital, they lease a retail space, purchase inventory, and set up an online store. Alice takes care of the day-to-day operations, while Bob focuses on marketing and sales.

In the first year, the firm performed well and generated a net profit of $80,000. According to their musharakah agreement, Alice and Bob will distribute the profits equally.

Alice's share: $40,000 (1/2 of $80,000)

Bob's share: $40,000 (1/2 of $80,000)

Therefore, both partners decide to reinvest some of the profits to expand their product range, expressing their satisfaction with the business's success. They contribute their respective shares to the musharakah pool, and the total capital becomes $120,000 (Alice: $60,000, Bob: $60,000).

The firm faced some challenges in the second year, and its net profit decreased to $20,000. Hence, the profits will be distributed equally once again:

Alice's share: $10,000 (1/2 of $20,000)

Bob's share: $10,000 (1/2 of $20,000)

After evaluating the business's performance, both partners decide to continue their partnership for another year, with an equal distribution of profits and losses.

This hypothetical example demonstrates a simple partnership between Alice and Bob, where they contribute equal amounts of capital, share profits, and losses equally, and make joint decisions regarding the business's operations and future.

Example #2

SkyWorld Development Group raised RM50 million on December 8, 2017, through Tranche 1 of their Sukuk Musharakah IMTN Programme.

The business announced that it had formed its first milestone RM1 billion financial plan, consisting of an RM600 million Sukuk Musharakah IMTN plan and an RM400 million Sukuk Murabahah ICP Programme, through a special-purpose financial vehicle called SkyWorld Capital Bhd.

Therefore, this is Malaysia's first structured deal, including unbilled sales, and the first involving low-cost housing. Moreover, this is also the market's first Shariah-compliant securitization of progress billings, allowing SkyWorld to manage project development cash flows better. Datuk Ng Thien Phing, founder and group managing director of SkyWorld, stated that despite being a relatively young and developing company, SkyWorld is always searching for unique funding.

Advantages And Disadvantages

Let us discuss the advantages and disadvantages of musharakah using the table below:

| Advantages | Disadvantages |

|---|---|

| It leads to the exploitation of excess liquidity held with Islamic banks | These are prone to mismanagement by the partners leading to losses. |

| Hence, it leads to higher returns for Islamic banks. | It needs constant supervision while funding a project that increases financing costs. |

| Risks get equally distributed amongst the partners | Here, the profits cannot be guaranteed. |

| Every partner shares the loss equally. | The whole system of financing has been criticized for being ancient. |

| Moreover, it benefits the poor account holder of the bank embarking into this type of banking. | They do not guarantee profit to the partners. |

Musharakah vs Murabaha

Let us discuss the differences between the two using the table below:

| Musharakah | Murabaha |

|---|---|

| Partnership based financing | Sale-based financing |

| Partners share profits and losses | The seller bears the risk of ownership until the sale. |

| Profit-sharing ratio is agreed upon between partners | Markup or profit margin is determined by the seller |

| A loss gets shared with the partners in proportion to the investment in the business. | All the loss gets borne by the rab-ul-maal |

| Suitable for joint ventures and long-term projects | Primarily used for financing assets or goods |

| Risk is shared among partners | Seller bears the risk of ownership until the sale. |

| Partners jointly own the business or project | Here, the buyer becomes the sole owner of the asset |