The distinctions between equity REITs and mortgage REITs list are:

Table of Contents

What Are Mortgage REITs (mREITS)?

Mortgage REITs are investment vehicles that invest in mortgages, both originated and purchased, mortgage-backed securities, and other similar assets. Investors in these Real Estate Investment Trusts (REITs) earn through the interest payments made on these mortgages. mREITs are vital in facilitating the much-needed liquidity in the real estate market. The best mortgage REITs listed on stock exchanges can be found online.

They are listed on major exchanges such as NASDAQ and NYSE. Compared to more stable equity REITs, these investments provide a greater dividend yield, particularly when interest rates are rising. While there are various advantages, such as diversification, protected funds, and no need for house maintenance, there are also disadvantages, like prepayment and credit risk.

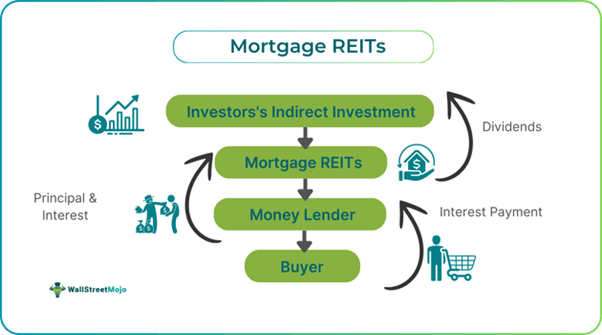

Key Takeaways

- Mortgage REITs are mortgage Real Estate Investment Trusts that invest in mortgage-backed securities and mortgages, both purchased and originated.

- They earn their profits through the interest payments made by borrowers.

- They provide the much-needed cash flow to the real estate industry and an opportunity for investors to be exposed to the real estate industry.

- It lets investors diversify their portfolios and protect their funds, and they are not required to maintain a physical piece of real estate.

- However, investors must still consider significant risks. The most common ones are credit risk, interest rate risk, prepayment risk, and rollover risk.

How Does Mortgage REITs Work?

Mortgage REITs, or mREITs, are investments that facilitate cash flow or funding into the real estate industry by purchasing or originating mortgages or mortgage-backed securities. They are a subcategory of the traditional Real Estate Investment Trust (REIT), which places the majority of impetus on real estate investment and financing.

In the United States of America, 1.4 million houses are built each year with the help of these investments. The mortgage REITs list also includes multiple commercial real estate. They provide loans to develop, reposition, own income-producing real estate, or acquire it.

These investment trusts earn their profits through means different than other forms of earning in the real estate industry. These investments typically earn returns through the interest payments made on the mortgage. Some funds are also earned through servicing and loan origination fees.

The funding for these investment trusts comes from various sources. They can source funding from repurchase agreements, preferred equity, credit facilities, long-term debt, and structured financing.

Investments provide various advantages to investors, such as diversification of their portfolios, protection of funds from the IRS, and no need to maintain a property physically. However, there are also severe risks to consider before investing.

A few of the most significant and common risks in these investments are interest rate risk, credit risk, prepayment risk, and rollover risk. Investors must perform their due diligence before stepping into these investments. Despite decent returns, there are critical downsides also to consider.

How To Invest?

Before deciding the mortgage REITs ETF that fits an investor’s criteria, there are a few points to keep in mind. They are:

- Since these investment options are listed on the stock market, they can be purchased like stocks. Investors can also purchase them or invest through mutual funds or ETFs. Therefore, the first step is to open a brokerage account.

- Investors can open a brokerage account after providing basic information such as income, investing experience, occupation, valid ID, and social security number.

- Use the brokerage app or website to review different options available regarding mREITs. Hence, it might be a brilliant idea to register and open a brokerage account with a broker that allows access to screening and analysis within their application or website.

- At this juncture, investors must consider the level of risks the REIT carries. They must also consider the brokerage fee and other fees related to investing in the particular mREIT.

- Once the investment has been made, investors must monitor the progress or decline at regular intervals.

Examples

Now that the theoretical aspects of mortgage REITs ETF are out of the way, it is time to explore the concept's practical applicability through the examples below.

Example #1

According to his wealth manager, Mr Das, as an investor, had too much exposure to equity and cryptocurrencies. Therefore, they decided to invest in mREITs to diversify their portfolio and increase their exposure to real estate as well. The idea was to balance out the risk from the highly volatile industries to which his money was exposed.

They invested in mREIT through mutual funds. In five years, Mr Das made regular returns through the interest received on mortgage payments made by customers securing mortgage loans.

Example #2

Blackstone Inc. and KKR & Co. are among the leading mREITs in America and perhaps the world. In 2024, they struggled to stay afloat as interest rates were significantly higher, and the dwindling demand for purchasing properties drove property values down.

However, spokespersons of BXMT said that over 92% of their loan portfolios are considered to be performing. In fact, the trust has experienced near-record levels of liquidities arising from collection. According to their earning reports, they collected in excess of $1 billion in repayments in the first quarter of 2024 alone.

Benefits

A few of the most prominent benefits of investing in the best mortgage REITs are:

- Private capital purchases residential mortgages and RMS, providing much-needed liquidity in the real estate market.

- mREITs are a significant source of funding for businesses and homeowners alike.

- These investments are an excellent way to diversify an investor’s portfolio as they balance out the volatility of stocks or crypto and beat the fixed returns of some low-risk debt instruments.

- IRS directs REITs to disburse 90% of their income to shareholders. Therefore, their funds are secured.

- Since investors do not physically purchase the property, they can be free of worry as no physical maintenance is required.

Risks

Despite all the advantages, mortgage REITs have their share of risks as well. A few of the most common ones are:

- Mortgage and MBS interest rates tend to fluctuate with the market's push and pull. Therefore, the value of these mREITs may vary based on these fluctuations.

- If a federal agency does not back a mortgage, the credit risk is exponentially high if the borrower defaults on repaying the loan.

- Since investors earn through interest payments from borrowers, if the investors decide to refinance their loans to a better mortgage, they may be forced to reinvest elsewhere.

- Since short-term debt is generally less costly than long-term ones, mREITs tend to fund their residential mortgages or MBS (Long-term) with them. However, this creates rollover risk, where these REITs must secure funding at fantastic rates to roll loans over as they mature.

Equity REITs Vs Mortgage REITs (in points or as a table)

| Basis | Equity REITs | Mortgage REITs |

|---|---|---|

| 1. Definition | They invest in physical properties like apartments, malls, or commercial buildings. | These trusts invest in mortgage-backed securities or mortgage loans and earn through the interest payments. |

| 2. Time Frame | Usually, it offers a long-term potential for growth through property appreciation. | Its prime focus remains to generate income through interest payments. They are also sensitive to short-term rate changes. |

| 3. Source of Revenue | They generate income through selling properties and leasing. However, the significant income comes in through rent. | mREITs earn from the interest payments made in securities or mortgage loans. |

| 4. Returns | Equity REITs tend to provide moderate dividend yields. However, the potential for capital appreciation is significant. | Usually, mREITs give higher dividend yields as their income is generated through interest payments. |

| 5. Risk Exposure | They are adversely affected by fluctuations in the property market, property values, and occupancy rates. | mREITs are extremely sensitive to the financial health of the credit markets and interest rate changes. |

Frequently Asked Questions (FAQs)

1

How do mortgage REITs make money?

2

Are mortgage REITs a good investment?

3