Table Of Contents

What Is A Mortgage In Principle?

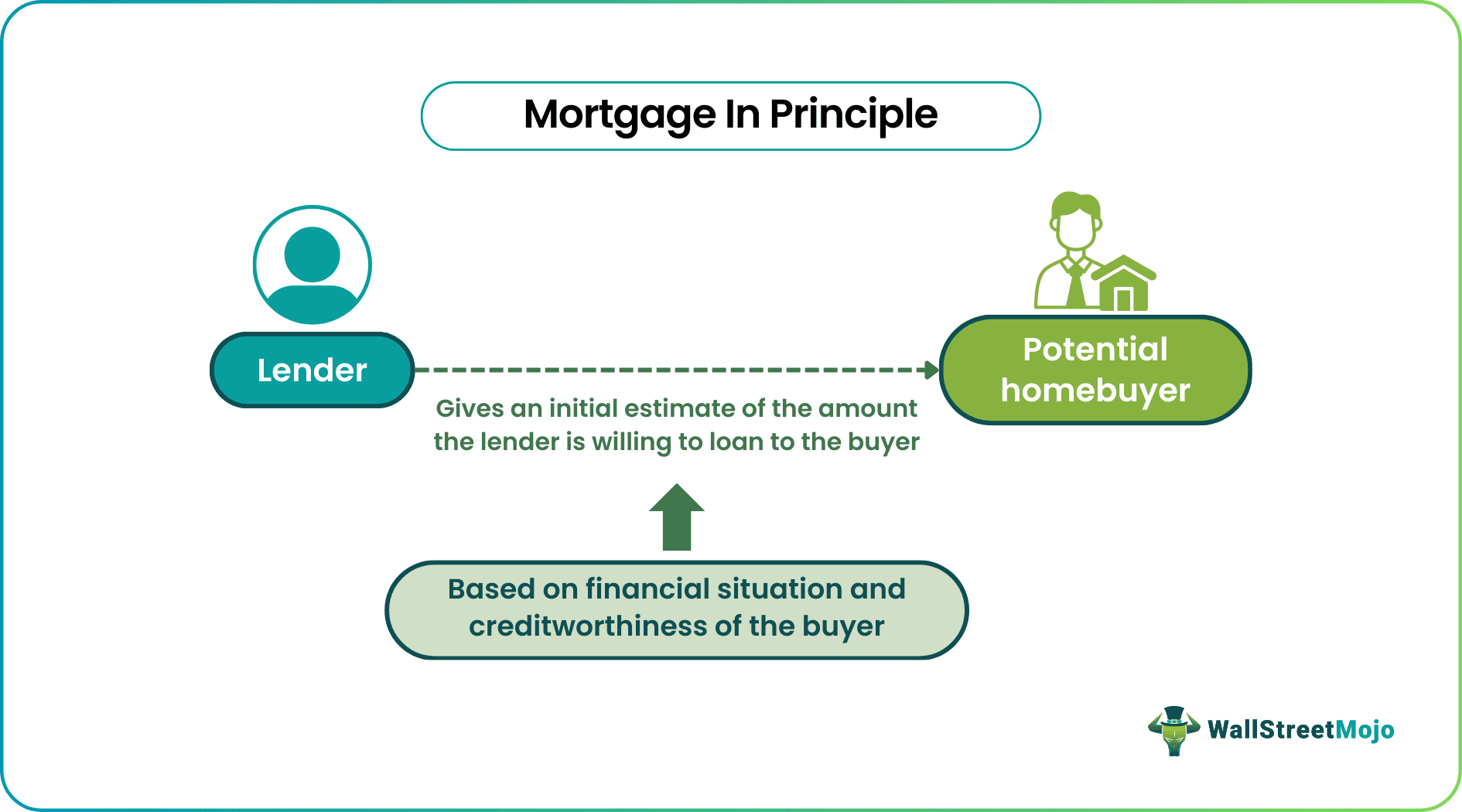

A mortgage in principle (MIP) is an official statement provided by a lender or housing society indicating the amount a person may be eligible to borrow for purchasing a property using it as collateral. It is a useful tool for potential homebuyers, even if they do not own a property.

A MIP demonstrates to sellers that the buyer can afford the property and is genuinely interested in purchasing. While not mandatory, MIP is taken seriously by real estate agents, making the process of finding and closing a property deal faster and more efficient for both buyers and sellers.

Table of contents

- What is a Mortgage in Principle?

- A mortgage in principle (MIP) is an estimation document provided by a lender or broker to a potential buyer, indicating the amount of money they can borrow to purchase a property.

- It benefits buyers even if they do not own a home and is a valuable tool for property search and affordability assessment.

- MIP can be obtained by visiting a real estate broker, requesting the lender to provide it, approaching a housing society, or using an online calculator.

- It represents the maximum loan amount offered to a borrower when they apply for a mortgage, while a mortgage offer signifies the lender's acceptance of their application.

Mortgage In Principle Explained

A mortgage in principle, is a statement from a lender to a potential homebuyer, estimating the loan amount they can obtain for a mortgage. It assures the seller that the buyer is financially capable and serious about purchasing the property. However, MIP does not guarantee a mortgage loan. It helps buyers determine a realistic price range, preventing them from applying for loans beyond their means.

The validity period of a mortgage in principle (MIP) can vary depending on the lender's policy. Typically, an MIP is valid for around 60 to 90 days. During this time, the potential homebuyer can use the MIP to search for properties and confidently make offers, knowing the approximate amount they can borrow. If the MIP expires before a home purchase, the individual may need to reapply or update their financial information to obtain a new MIP.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

How To Get It?

In order to get a mortgage in principle, several methods are available. One can approach a property broker, directly request the lender to provide it, or ask the housing society to prepare it. Additionally, many lenders and brokers offer the option to apply for the MIP through their websites, such as NatWest mortgage in principle, Halifax mortgage in principle, or HSBC mortgage in principle. It is essential to obtain the MIP before starting the process of searching for a home to buy. This initial step helps determine one's eligibility and the mortgage limit, providing a clearer picture of the affordability and available options for buying a home.

Examples

Let us use a few examples to understand the topic:

Example # 1

Consider Alex, who dreams of owning a home in New York. To begin the home-buying process, he seeks a mortgage in principle from the nearest broker. Following the broker's advice, he visits the lender's home branch and submits the necessary documents. After a soft credit check, the lender provides Alex with an estimated mortgage amount he can borrow. With the MIP in hand, Alex gains confidence in his budget and affordability, allowing him to search for the most suitable property.

Example # 2

Now, consider Noah, who already has a property acquired through a mortgage loan. Eager to buy another property in California's suburbs, Noah initiates the MIP process with a lender. However, the lender performs a hard credit score check, considering Noah's previous mortgage record. Consequently, the lender offers a lower estimate for the second mortgage, indicating potential limitations in Noah's eligibility for a sufficient loan amount. Realizing the constraints, Noah decides to suspend his search for a second property, acknowledging that obtaining another mortgage may be challenging.

Mortgage In Principle vs Mortgage Offer

Let us understand the difference between the MIP & mortgage offer using the table below:

| Mortgage in Principle | Mortgage offer |

|---|---|

| MIP indicates the amount of loan that can be offered for one applying for a mortgage loan. | Mortgage offer means that the lender has accepted the to entertain mortgage loan application. |

| Does not guarantee a mortgage to the applicant. | It means that an applicant’s details and finances have been fully reviewed and found to be eligible for the offer. |

| One of the first steps in getting a mortgage loan. | Mortgage offer also means that if an individual now accepts the terms and conditions of the lender, then they will be sanctioned the loan. |

| MIP may or may not affect the credit score of an individual. | It affects the credit score of individual applicants. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

No, a mortgage in principle (MIP) does not include the deposit. Based on the applicant's financial information, it is an initial estimate of the amount a lender may be willing to offer for a mortgage. The deposit is the amount of money the buyer needs to contribute upfront when purchasing a property, separate from the mortgage amount.

Yes, the lender or the applicant can withdraw a mortgage in principle (MIP). It is not a binding agreement, and either party can decide not to proceed with the mortgage application. The MIP may no longer be valid if there are significant changes in the applicant's financial situation.

A mortgage in principle (MIP) and an agreement in principle (AIP) are different terms. But they are used interchangeably to refer to the same concept. Both represent an initial assessment by a lender to estimate the amount they may be willing to lend to a potential borrower. It helps applicants understand their borrowing capacity and makes the property search process more focused.

Recommended Articles

This has been a guide to what is Mortgage in Principle. Here, we explain how to get it, and explain its examples, and comparison with mortgage. You can learn more about it from the following articles -