Table Of Contents

What is the Market Risk Premium Formula?

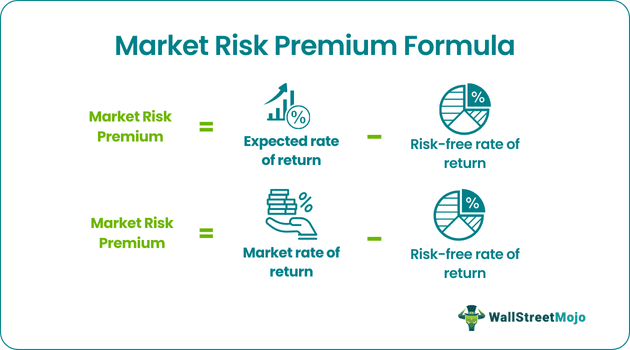

The term “market risk premium” refers to the extra return that an investor expects for holding a risky market portfolio instead of risk-free assets. In the capital asset pricing model (CAPM), the market risk premium represents the slope of the security market line (SML). The formula for market risk premium is derived by deducting the risk-free rate of return from the expected or market rate of return.

Mathematically, it is represented as,

Market risk premium = Expected rate of return – Risk-free rate of return

or

Market risk premium = Market rate of return – Risk-free rate of return

Examples of Market Risk Premium Formula (with Excel Template)

Let’s see some simple to advanced examples of the Market Risk Premium Formula

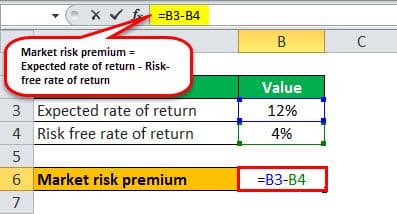

Example #1

Let us take an example of an investor who has invested in a portfolio and expects a rate of return of 12% from it. However, in the last year, government bonds have given a return of 4%. Based on the given information, determine the market risk premium for the investor.

Therefore, the calculation of market risk premium can be done as follows,

- Market risk premium = 12% - 4%

Market risk premium will be-

Based on the given information, the market risk premium for the investor is 8%.

Example #2

Let us take another example where an analyst wants to calculate the market risk premium offered by the benchmark index X&Y 200. The index grew from 780 points to 860 points during the last year, during which the government bonds have given an average 5% return. Based on the given information, determine the market risk premium.

To calculate Market Risk Premium, we will first calculate the Market Rate of Return based on the above-given information.

- Market rate of return = (860/780 – 1) * 100%

- = 10.26%

Therefore, the calculation of market risk premium can be done as follows,

- Market risk premium = 10.26% - 5%

- Market risk premium = 5.26%

Relevance And Use

An analyst or an intended investor needs to understand the concept of market risk premium because it revolves around the relationship between risk and reward. It represents how the returns of an equity market portfolio differ from that of the lower risk treasury bond yields owing to the additional risk that the investor bears. The risk premium covers expected returns and historical returns. The expected market premium usually differs from one investor to another based on risk appetite and investment styles.

On the other hand, the historical market risk premium (based on the market rate of return) is the same for all the investors as the value is based on past results. Further, it forms an integral cog of the CAPM, which has already been mentioned above. In the CAPM, the required rate of return of an asset is calculated as the product of market risk premium and beta plus the risk-free rate of return.