Table Of Contents

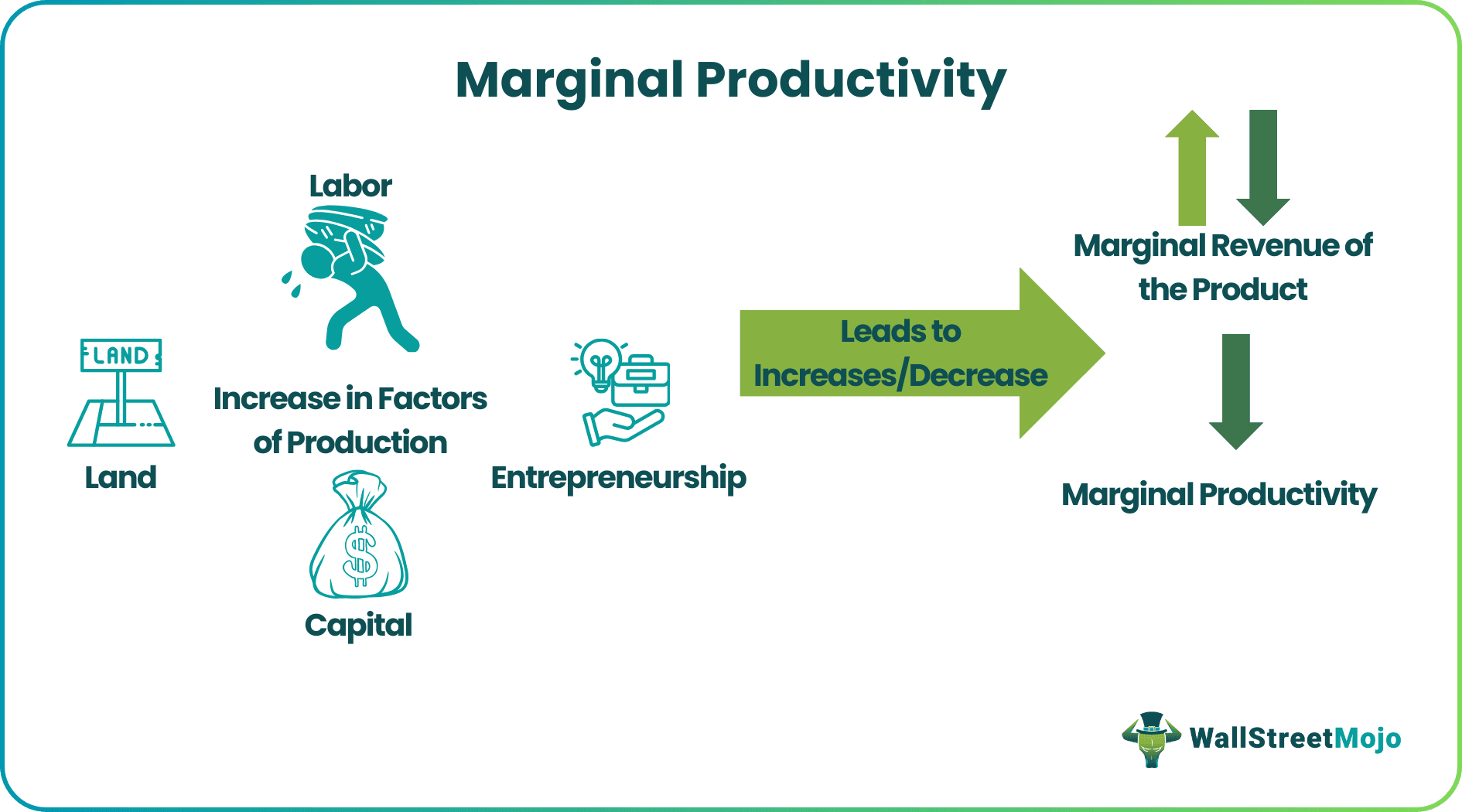

What Is Marginal Productivity?

Marginal productivity determines the net rewards for the factors of production when one-factor input increases. In other words, it is the change in output with the change in addition units of input, other factors remaining constant. It helps the producers and firms to find the prices of the factors like labor, land, capital, and entrepreneurship.

This classical marginal productivity theory depends on the marginal revenue product (MRP). Producers and suppliers use it to analyze their outputs and make better production decisions. It applies to perfect competition with similar products, full factor utilized, and perfect mobility. However, it does not apply to imperfect competition.

Table of contents

- What Is Marginal Productivity?

- Marginal productivity refers to the net input made to total production by producing an additional output unit. Inputs include land, labor, capital, technology, and entrepreneurship.

- Economists also refer to it as the classical theory of distribution. In the 19 century, economists J.B Clark, Leon Walras, Enrico Barone, David Ricardo, and Alfred Marshall also worked on it.

- The three types of factor pricing theory include marginal physical productivity, marginal revenue productivity, and value of marginal productivity.

- In the marginal productivity curve, the overall productivity decreases as the number of inputs increases, shifting the MRP curve from left to right.

Marginal Productivity Explained

Marginal productivity theory meaning implies the net addition made to the total production by producing an additional output unit. It analyzes the effect of increasing inputs on the prices of the factors of production. It is also known as marginal physical productivity or pricing theory. Here, the producer increases any factor (capital or labor) until it reaches the marginal cost, assuming other factors to be constant. However, if it exceeds the marginal revenue, overall productivity declines.

Three types of factor pricing theory include marginal physical productivity, marginal revenue productivity, and value of marginal productivity. German economist, T.H. Von Thunen, put forth this classical theory in 1826. Later, neo-classical economists like John Bates Clark, Walras, Philip Henry Wicksteed, David Ricardo, and Alfred Marshall also worked to develop this theory. According to them, the early factor inputs provide a surplus to the firm. In simple terms, it follows the law of variable proportion. But, in the later stage, it gives declining returns due to a massive increase in factor units.

In the early stages, total revenue rises when the producer increases the one-factor unit while the rest remains constant. After some time, the marginal revenue diminishes with every input increase. Finally, it reaches a point where it equals the marginal cost. It leads to diminishing marginal productivity.

Since the marginal cost equals marginal revenue, the price of the factor remains the same as the industry. Now, the firm goes for closer substitutes to maximize profits. They replace the expensive factors with cheaper ones. For example, replacing labor with effective and cheap machines. If the firm employs more factors, it will make huge losses.

However, this theory has certain assumptions like perfect competition, mobility, and most factor usage. As a result, many economists criticize the unrealistic assumptions of this classical theory of distribution.

Formula

Here is the marginal productivity formula to calculate changes in production:

Marginal Productivity (MPn) = TPn - (TPn-1)

where TPn = Total factor productivity by "n" units of factor

TPn-1 = Total productivity by "n-1" units of factor.

One can use the following formula too to calculate it:

MP = ΔY / ΔX

Where ΔY is the change in output quantity resulting from input change. Y does not include external costs and benefits.

ΔX is the one-unit change in the firm's input use,

Based on types, there are two more formulas for this classical theory:

Marginal revenue productivity (MRP) = MPP * MR

where MPP = Marginal physical productivity

MR = Marginal revenue

Value of Marginal Productivity (VMP) = MPP * AR

where MPP = Marginal physical productivity

AR = Average Revenue

Curve

The tabular column given below represents the marginal productivity graph of labor:

| Units of Labor | Wage Rate ($) | Marginal Revenue Product |

| 14 | 45 | 60 |

| 15 | 45 | 55 |

| 17 | 45 | 50 |

| 18 | 45 | 45 |

| 20 | 45 | 40 |

In the given table, as per the marginal productivity theory, the producer increases the labor units gradually. During the initial stages, the wage rate of labor is $45. As the producer increases the number of laborers, the overall labor productivity decreases. At one point, the wage rate becomes equal to the marginal productivity of labor. If the firm continues to hire labor, it might make huge losses.

The below marginal productivity graph shows the graphical representation of the marginal productivity graph:

In the marginal productivity graph, OQ is the number of factor units employed by the producer. In contrast, OP is the price paid to the factor. Therefore, the MRP curve declines as the producer hire more factor units (OQ2). If this continues, the firm will have a negative MRP curve.

At this point, the entrepreneur reduces the number of factor units to OQ1. In contrast, as the price of the factor increases to OP1, the additional productivity is the highest (i.e., CQ). Therefore, the producer needs to hire the right unit of the factor of production to achieve maximum productivity as close as possible to the factor price.

Assumptions

The value of marginal productivity attempts to explain how to factor prices are determined in the competitive market. There are some important assumptions made in it, which are as follows:

- Perfect competition assumes that the market is perfectly competitive for inputs and outputs, which signifies that the firms cannot decide the prices independently. They are the price takers.

- Profit maximization – It assumes that the ultimate aim of the firms is to earn profits. So they will continue to hire more factors till they are able to earn additional income from each extra unit.

- Homogeneous inputs – It assumes that all inputs can be interchanged, which means that the inputs during production are all homogeneous.

- Full employment – According to the theory, all the factors of the inputs are fully employed. This means that all the resources are fully used in the economy to their optimum capacity and there is no involuntary unemployment.

- Diminishing marginal returns – It assumes that as extra units of a particular input are employed, it eventually decreases the marginal productivity of the fator, provided all other inputs are held constant.

- No change in technology – The technology in the production process is assumed to be fixed. This makes the analysis simple.

- Rationality in decisions – It assumes that both individuals and firms make decisions in a very rational way, and they seek to maximise profits based on the information that is available.

Examples

Let us look at the value of marginal productivity examples to understand it better:

Example #1

Let us assume Stevie is the owner of the Grains and Sons Co. In a few months, their product demand has increased massively. So, Stevie decides to hire more land to increase its production. Stevie used to pay $2.6 million for 2000 square feet of land. At this point, the productivity margin was the highest. So, later on, Stevie hired more acres of land.

This decision resulted in increased units of labor and land. But the overall productivity declined drastically. In addition, the firm's profits had also decreased due to the decision. As a result, he reduced the number of factor units to equal the price of each factor unit.

Example #2

In New Zealand, Hastings District Council and Hawke's Bay Regional Council conducted a meeting on August 9, 2022. The main idea of this meeting was to discuss the impact of soil on additional productivity. Soil scientist Keith Vincent discussed how land and climate had enhanced Hawke's Bay's land. In addition, certain land management techniques have increased productivity.

The above examples explain clearly how the theory acts and is used for analysis in different situations.

Criticisms

The concept of marginal productivity is subject to certain criticisms that state how it fails to capture many complex situations of the real-world market. Let us look at them in detail.

- Imperfect competition – As per the theory, the market is perfectly competitive. However, in the real world, it is not the case. Every market is imperfect upto a certain extent where the firms can exercise their own power to a certain level, giving them the chance to influence prices.

- Factor analysis – In this case, the theory focusses on the marginal productivity of factors in isolation. But in reality, they are dependent on each other. For instance, investment in technology will uplift the productivity of labor. Thus, the theory is not true in this case.

- Technological change – Technological change in inevitable. It cannot remain constant, as assumed in the theory.

- Input may be heterogeneous – The theory assumes that each type of input is homogeneous. However there may be variation among the inputs, like each labor may be different in terms of skill, wage, productivity, etc.

- Full employment – This assumption does not apply in the real world because there may be umemployment and resources may remain underutilised leading to difference in factors.

- Non-market factors ignored- The non-market factors like labor unions, wages, are ignored but they influence factor prices.

- Uncertainty – It does not consider the situations of uncertainty in the dynamic and continuously changing economic world. These uncertainties often affect the market prices either positively or negatively.

But inspite of all the criticisms, the concept of marginal productivity acts as an important and valuable tool that helps in understanding the relation between prices and productivity in the markets.

Marginal Productivity Vs Total Productivity Relationship

Economists can explain the relationship in 3 phases. They are the following:

- Marginal product rises when the quantity of variable input increases as the total product rises at an increasing rate.

- As firms employ greater quantities of variable inputs, the total product rises at a diminishing rate. In this case, the marginal product starts to fall.

- When the total product reaches its maximum, it starts to fall, the marginal product becomes zero, and it further becomes negative.

Frequently Asked Questions (FAQs)

According to this law, increasing a factor unit decreases productivity margin after a certain point. Therefore, producers use this law when they want to increase production and profitability.

Yes, the factor pricing curve can turn negative if the producer keeps increasing the factors. If the number rises to the extent that marginal cost exceeds marginal revenue.

When one additional unit increase in capital leads to an increase in the overall output, it is known as the marginal productivity of capital.

Various reasons decrease a firm's overall productivity. The primary reason includes excess units of factors that lead to an increase in the marginal cost. Similarly, the firm's profits decrease as they pay an extra marginal rate to the factor units.

Recommended Articles

This article has been a guide to what is Marginal Productivity. We explain its formula and the curve along with examples, assumptions and criticisms. You can learn more about it from the following articles -