Table of Contents

Macroprudential Policy Definition

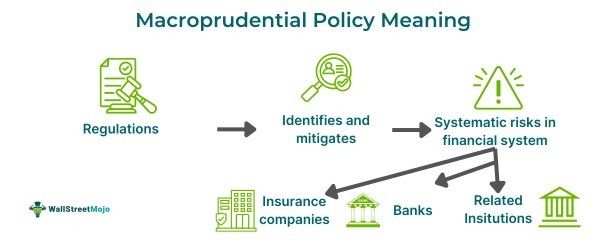

Macroprudential policy is a framework that provides guidelines and prudential tools to reduce systematic financial risk. These regulations interact with similar public policies and include targeted rules introduced to control instability in the financial system. They limit disturbances in the delivery of key financial services.

It seeks to find solutions to the limitation of macroprudential policy, which focuses on the sound functioning of individual financial institutions. Macroprudential focus helps in establishing sound financial supervision and regulation through a systematic approach (identify and mitigate risks). Along with the monetary policies, it helps with countercyclical management by looking into price and financial stability.

Key Takeaways

- Macroprudential policy is a regulatory framework that targets the reduction of systematic financial risks. This is done to ensure table delivery of financial services in an economy.

- It goes beyond the traditional micro-prudential policy measures of regulating individual institutions. Instead, it focuses on the identification and mitigation of risks across the system.

- Key aspects of the policy include framing of regulation with accountability, power to make recommendations, customization according to unique problems etc.

- They are to be enacted along with other policies, and their instruments include capital-based instruments, liquidity-based instruments and asset-side instruments.

Macroprudential Policy Explained

Macroprudential policies are provisions that are established to identify and mitigate systematic risks. They were introduced as a result of micro-prudential failures or the traditional approach. Microprudential failures involved the regulation of financial institutions only as it believed the sound functioning of individual institutions guaranteed a stable system. Failed to recognize that institutions individually can be responsible for other institutions and the market as a whole.

Macroprudential regulations complement microprudential policies by adapting traditional tools to oppose growing risks in the system. The policies are hence designed to identify and mitigate risks in the system. They expose sources of risks such as real estate value decline and increased tie-up of credit to real estate collaterals. The risks can be generalized as credit, market and liquidity risks.

The policies specifically aim to address systematic risks under time and cross-sectional dimensions. The time dimension involves the cumulative mechanism that operates between the real economy and the financial system within the system. Cross-sectional dimensions deal with the risk distribution in the system at a particular point in time.

Macroprudential policy frameworks are not foolproof, and each economy has to develop one that fits its requirements. The first challenge faced by the planners would be the sector's dynamic evolution. The next challenge would be maintaining the continuous risks, such as inflation, that follow a crisis. The third challenge would be coordination among various policies.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Key Aspects

The key aspects of this policymaking are given as follows:

- It limits the build-up of systematic financial risk.

- It detects and addresses systematic risk and interacts with other policies to do so.

- It is not a substitute for a strong micro-prudential and policies that focus on macroeconomics.

- The analytical methods used, instrument choices and institutional arrangements are to be framed after considering the prevailing local conditions.

- All potential sources of systematic risks shall be monitored comprehensively. This shall include models, assessments, supervisory data, quantitative indicators, qualitative information etc. It shall also consider domestic macroprudential provisions on other country's financial stability (and vice versa).

- It shall encompass providers of liquidity, maturity and credit irrespective of their legal form. It shall also include financial market infrastructures and other systemically important institutions.

- Instruments used to target systematic risks shall be under macroprudential authority's direct control.

- It shall be bestowed with the power of recommending changes.

- It shall have clear mandates and objectives with adequate powers and accountability.

- It shall have powers to collect, report, regulate and activate instruments under its control.

- Central banks shall have prominent roles in the policy-making process. Similarly, a body shall be in place to ensure consistency.

Instruments

Instruments of the macroprudential policy framework can be categorized as capital-based instruments, liquidity-based instruments and asset-side instruments.

#1 - Capital Based Instruments

1. countercyclical capital buffers

They measure the aggregate credit cycles.

2. dynamic provisions

They measure bank-specific credit growth aspects and the specific provisions with both current and historical averages).

3. sectoral capital requirements

They measure the quantity and prices of various credit aggregates. These macroprudential policy tools include loans and stocks on a sectoral basis. Interbank credits are a part of it. They also measure sectoral concentrations and distributions across and within sectors. Furthermore, they also measure real estate prices of old, new, commercial and residential properties.

#2 - Liquidity Based Instruments

1. countercyclical liquidity requirements

Potential indicators include LCR, NSFR, LIBOR-OIS spreads, leading spreads and loan deposit ratios. It also includes long-term assets, loans to long-term funding, and liquid assets to short-term liabilities or total assets.

2. Hair cuts and margins in the markets

The potential indicators include haircuts and margins, liquidity premia, market depth measures, bid-ask spreads, shadow banking leverage and valuations.

#3 - Asset Side Instruments

LTVs and DTIs

They are loan-to-value (LTV) and debt-to-income (DTI) tools. Potential indicators include:

- Price to rent ratios.

- Underwriting standards.

- Real estate prices of commercial and residential, new and old, developed properties.

They also include indicators of cash-out financing and household vulnerabilities.

Examples

Example #1

Let us look at a hypothetical example of country A, which is facing a credit crunch. The country is perplexed by the losses its banks and lenders have suffered. This has led to the curtailment of credits to firms and households. The problem affects the overall economy. Since there is no availability of credit, the economic activity has come down. This was attributed to issues pertaining to banking institutions. The country, hence decides to implement macroprudential policy tools that would focus on the overall system. Additionally, since macroprudential and monetary policies can help stabilize the economy, the country decides to implement both simultaneously. The system may restrict banks from indulging in certain activities to ensure economic growth and financial system stability.

Example #2

European central bank and the journal of financial stability are set to organize the sixth annual macroprudential research and policy conference. the date set if on 21st November 2024. The conference aims to bring academics, market participants and cental bankers together to discuss and present research on financial stability. macro finance topics of the central bank interests will also be out forward.

Importance

Given below are some of the points that describe the importance of these policies;

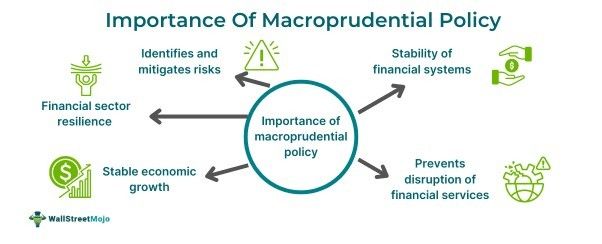

- They ensure the stability of the financial systems through the regulation of indicators of system risks.

- They work to prevent disruptions in the provision of important financial services and credit flow.

- It helps in implementing the necessary steps for stable economic growth.

- It identifies and mitigates risks to ensure systematic stability.

- It enhances the resilience of the finance sector and restricts the build-up of risks.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.