Table Of Contents

What is Lump Sum Payment?

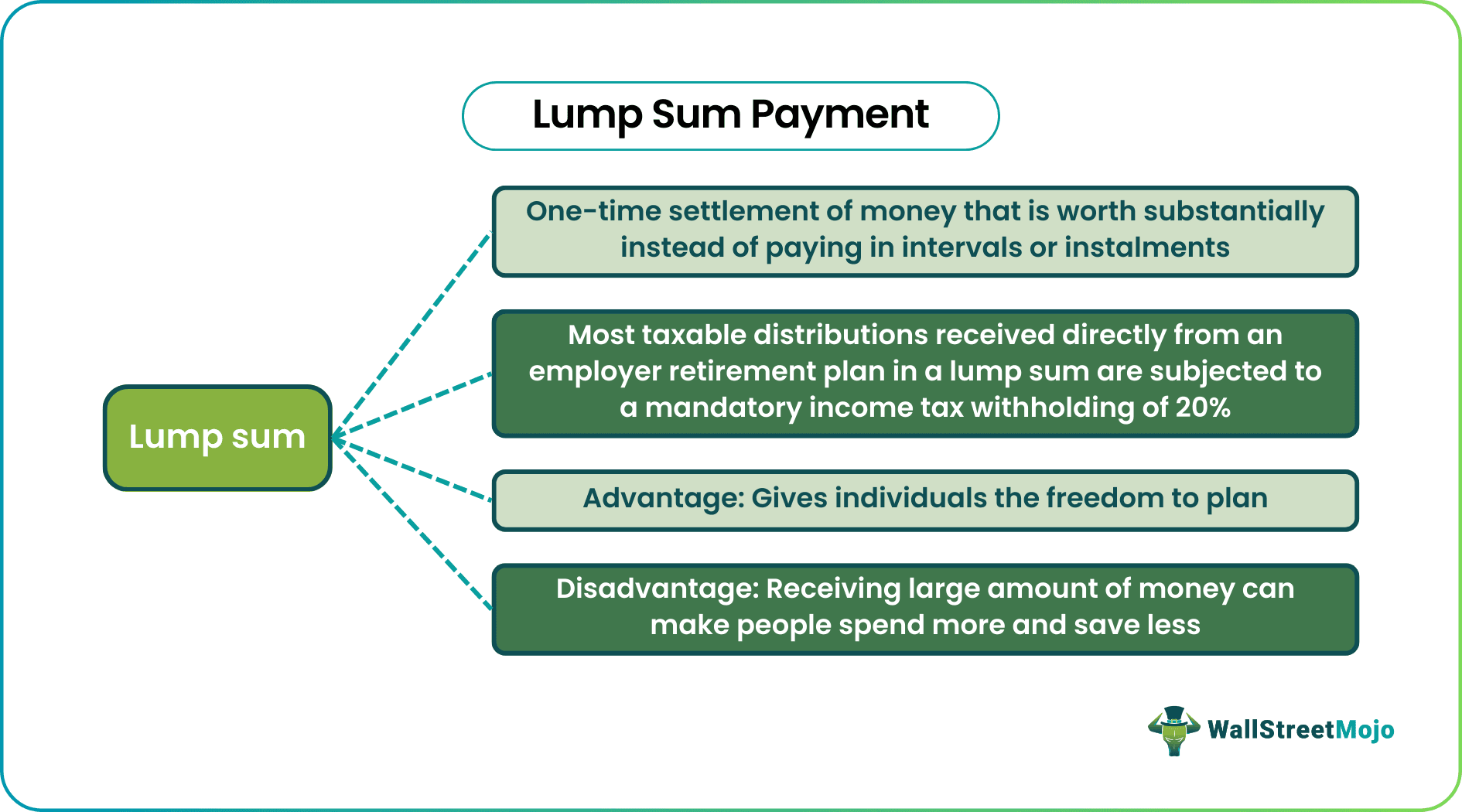

Lump-sum refers to a large amount of money and lump-sum payment is a significant amount of money someone pays in a single payment, unlike making a series of payments over time or in regular intervals. It has advantages and disadvantages and the benefits vary according to different situations.

In a loan or mortgage, paying a large amount of money as a one-time settlement within a few months can save a lot of interest. On the other hand, an individual who has been settled with a lump sum amount will have the freedom to invest when the prices are right.

Table of contents

- What is Lump Sum Payment?

- A lump sum is the settlement of large amounts at one time, unlike the installment scheme, which is paid monthly or regularly.

- There are several advantages to receiving settlements at one time. The person on the receiving end can enjoy a large sum, while those who are giving the money risk losing. For example, paying a lump sum contract price in house construction will prevent unnecessary price increases.

- A mandatory income tax withholding of 20% is required on most taxable distributions received directly from an employer's retirement plan in a lump payment, even if they plan to roll the taxable amount over within 60 days.

Lump-Sum Payment Explained

The lump-sum payment provides a sum of money in one single transaction. One-time payment simplifies the payment process. It gives the receiver the freedom to plan and take necessary actions to achieve their goals. A large number of payments have their advantages in various fields. For example, lump-sum contract payment in case of house purchases can save a significant amount in cost growth of projects. They can also reduce the price rise in materials purchased for the construction. Moreover, paying a mortgage as early as possible in a single settlement saves money through interest. This is because the entire amount is paid upfront; a single payment is usually less expensive than paying in installments.

However, receiving large sums of money as a one-time settlement has disadvantages too. For example, investors who invest large sums of money in a highly volatile asset may lose their savings. At the same time, investors who invest monthly in SIPs (Systematic investment plans) can save themselves from market volatilities. Similarly, a pensioner who receives a pension in a one-time settlement may spend it sooner and have little money remaining with them. Lump-sum tax payment is another scenario where paying a large amount of money can negatively impact. On the other hand, paying taxes regularly without default can save the individual from burning a hole in their pocket.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Example

Danny invests $50000 in the stock market for the long term. The amount will be kept for fifteen years with an interest rate of 11%.

It is noteworthy that investments work on the compounding effect. Whether the returns are lump-sum, the invested amount gathers higher interest when kept for longer periods (compounding effect). Here the invested amount is $500000 at a rate of 11% for fifteen years, which will give an estimated return of $18, 92,295 and the total value of the investment that Danny will get at the end of the investment are $23, 92,295. Had he opted for a monthly payment of $239.2495, he would have smaller amounts of the money. For example, if the investment returns were in the form of monthly payments, the rate would have been $199357 every month for a year (if opted for). This is a simple process and easy to calculate. However, there is an online lump-sum payment calculator through which individuals can find answers.

How is Lump Sum Payment Taxed?

An individual born after January 2nd, 1936, can select tax methods on the distribution if they receive a lump-sum payment from a qualified retirement plan or annuity.

A lump-sum distribution here is the distribution or payment within one tax year of a participant's plan's entire balance from all of the employer's qualified plans of one kind. This could be a pension, profit-sharing, or bonus plan in stocks. Moreover, it is an amount that one pays in the following circumstances:

- The death of the plan participant

- The participant reaches the age of 59.5.

- If the participant is an employee and leaves the service.

- A self-employed individual after the participant becomes permanently fully disabled.

Taxes differ from place to place along with the rates, and given below are a few pointers for the same.

Most taxable distributions received directly from an employer retirement plan in a lump sum are subject to a mandatory income tax withholding of 20%. Even if they expect to roll over the taxable amount within 60 days,

Another case to consider is the Net Appreciation (unrealized). For example, suppose the lump-sum payment includes employer securities, and the payer reported an amount for net unrealized appreciation (NUA) in employer securities (such as Distributions from Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, and Other Investments). In that case, the NUA is generally is not taxed until individuals sell the securities. But, individuals can choose to include the NUA in their income in the year of stake distribution.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Beginners who are yet to get accustomed to the market highs and lows can opt for SIP. Regular payments can reduce the risk of market volatility. On the other hand, a seasoned investor can invest huge amounts in taking advantage of the low prices of the stock.

Pension income is calculated on factors based on age, mortality, and the Internal Revenue Service's minimum present value segment rates to determine the current value of the pension income. Higher interest rates can imply a smaller amount. One can use a lump sum payment calculator to arrive at the value.

The net unrealized appreciation (NUA) is generally not subject to lump-sum payment tax until individuals sell the securities. If the distribution includes employer securities and the payer reported an amount for NUA in employer securities in Form 1099-R, which provides for pension, annuities, etc.

Recommended Articles

This has been a guide to what is a lump-sum payment and its meaning. We discuss how is lump-sum payment is calculated with examples, taxes and its advantages. You can learn more about it from the following articles –