Table Of Contents

Loan To Value Ratio Meaning

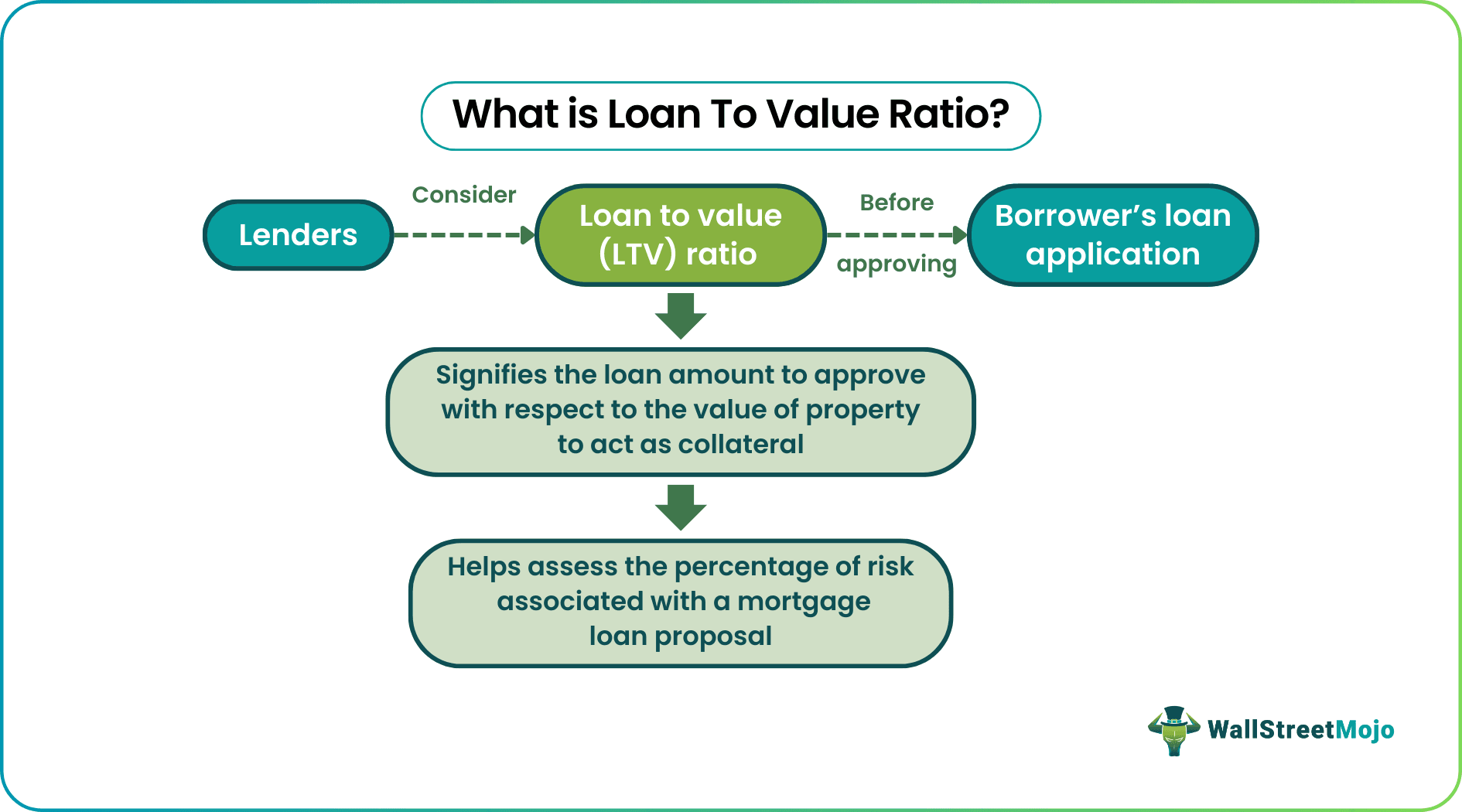

The Loan to Value (LTV) ratio is a risk assessment tool for lenders, signifying the extent of risk they would be at if they approve a loan amount to seekers with respect to the property's value, which acts as collateral. The lenders or creditors consider this ratio before approving any mortgage loan application. If the ratio is good to go, the loan seekers receive approval.

A higher LTV would mean a higher risk involved with the mortgage loan deal. In such a scenario, the lenders ask loan seekers to buy mortgage insurance against the approval to mitigate this risk associated with the same.

Table of contents

- Loan To Value Ratio Meaning

- Loan to Value ratio refers to the relationship between the loan amount and the property's value acting as collateral in the deal.

- The higher the LTV ratio, the higher the risk for lenders approving a mortgage loan.

- The LTV ratio allowed varies from lender to lender.

- Based on the LTV ratio, a lender approves or disapproves the loan application or allows a specific amount as a loan, with the rest being paid by borrowers' from their pocket as a down payment.

Loan To Value Ratio Explained

Loan to Value ratio indicates the relationship between the loan amount and the property value that acts as a security/collateral for the mortgage. This helps lenders determine the risk level associated with approving a particular loan application. Lenders give home seekers two alternatives to purchasing a house as it is a basic requirement.

Firstly, when they check the ratio and find out the amount is risky, they only agree to approve lending a specific amount. In such a scenario, a person agrees to receive the approved amount as per the LTV and pays the rest from their own pockets as a down payment for the property they buy, be it a house or a car. The same property becomes collateral against that mortgage loan.

Secondly, the mortgage loan providers may ask borrowers to sign a mortgage insurance contract to mitigate some risk in the event of default. This insurance deal is referred to as private mortgage insurance (PMI).

The LTV ratio marks the risk percentage for the lenders in case the borrowers fail to repay. For example, when the loan amount is half the value of the collateral, the risk is as high as 50% as the lending institutions have no guarantee of getting their payment in full if borrowers default. Likewise, the higher the LTV ratio, the more the risk.

Regarding the loan to value ratio for refinance, 80% or less is considered ideal.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Formula

The loan to value ratio formula used for calculation is:

Loan to Value Ratio= Mortgage Amount / Appraised Value of the Property

Calculation Examples

Let us consider the following examples to see how to calculate loan to value ratio:

Example 1

Suppose Mr. X wants to buy a home worth $400,000 (the appraised value in the market). However, the bank uses the loan to value ratio calculator and tells him they could only give him 80% of the amount and the rest he needs to share from his pocket. Thus, it approves a mortgage loan of $180,000. On the other hand, the borrower has to pay the $40,000 from their pocket to purchase the home. Thus, here, the LTV ratio is 80%.

Example 2

Now, let us have another example with the different appraised values of the property and purchase price. This example shows how the appraised value for the property might differ for different banks.

| In US $ | Bank A | Bank B |

| Purchase Price | 360,000 | 330,000 |

| Down Payment | 80,000 | 70,000 |

| Appraised Value of Property | 400,000 | 350,000 |

Here, a difference is noticed between the appraised value of a property and the purchase price.

But, first, let us calculate the mortgage amount.

| In US $ | Bank A | Bank B |

| Purchase Price | 360,000 | 330,000 |

| (-) Down Payment | (80,000) | (70,000) |

| Mortgage Amount | 280,000 | 260,000 |

As the purchase price is lesser than the appraised value of a property, let us consider the purchase price for calculating an LTV ratio.

For Bank A

LTV would be = (280,000/360,000) = 77.78%.

For Bank B

LTV would be = (260,000/330,000) = 78.79%.

In this case, we can see that the LTV of Bank B is slightly more than Bank A.

LTV Ratio & Interest Rates

Lenders go for risk-based pricing, which signifies selling mortgage loans with high risks at a higher interest rate. As a result, loan seekers with poor or average credit scores are offered loans at significantly higher interest rates, while those with good credit have to make lower interest payments. Therefore, a loan deal with a higher LTV ratio will be offered at a higher interest rate and vice-versa.

Variations

Variations are quite common in LTV ratios, given where the loan comes from. While one LTV ratio might fit the requirements of one lender, the same might not be up to the mark for another. For example, the Federal Housing Administration (FHA), which allows mortgage loans to low-to-moderate income groups, approves loan applications with LTV of up to 96.5%, with the borrowers having to pay the insurance premium in exchange.

On the other hand, the US Department of Veteran Affairs (VA) and the US Department of Agriculture (USDA), which allow loans to former and current military professionals and rural residents, allow loans with an LTV ratio of up to 100%. Here, though the PMI is not required, the lenders might have some additional costs for borrowers to pay.

Importance

The LTV ratio helps compare the loan's size and the collateral's size. With the help of this ratio, the lenders understand what loan amount to approve so that the borrowers can repay easily. Hence, they allow that specific loan amount and make borrowers pay the rest from their pocket as a down payment. In short, the LTV helps lenders to evaluate the loan proposal of the mortgage loan seekers.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

The LTV is a ratio of the loan amount concerning the total value of a particular asset. Banks or lenders commonly use it to determine the amount of loan already given on a specific investment or the margin to be maintained before issuing money to ensure protection in the event of default.

An LTV of 80% or less is considered ideal. However, lenders might approve security-backed mortgage loans with an LTV of more than 80% while asking them to pay an insurance premium to safeguard the amount or mitigate the risk involved.

The LTV ratio reduces if borrowers choose to pay a major portion as a down payment, thereby reducing the amount they require as a loan.

Recommended Articles

This is a guide to what is the Loan to Value Ratio and its meaning. Here we explain its importance, variations, formula, and examples with calculations. You can learn more from the following articles -