Table of Contents

What Are Loan Products?

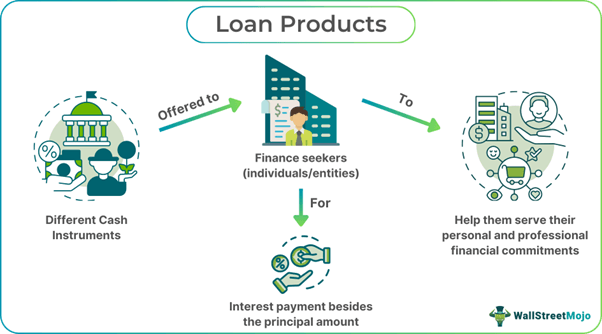

Loan Products refer to different financial instruments that lenders provide to businesses or individuals in exchange for regular interest payments. When in need, these options give finance seekers access to funds on a credit basis for personal purchases, business purposes and investments.

It encompasses several credit options, including personal loans, home and mortgage loan products, commercial loan products, etc. These products help individuals or entities buy a home, fund business operations, purchase cars, fulfill personal needs and medical expenses. It consists of repaying the principal amount alongside the interest for a fixed duration.

Key Takeaways

- Loan products represent financial instruments provided to businesses or individuals for credit-based funds for personal purchases, business purposes,

- and investments in exchange for repayments in the form of regular interest besides the existing principal amount.

- They are of 5 types: secured loans, unsecured loans, auto loans, small business loans, and revolving credit loans.

- Banks consider loan purpose, interest rate, repayment duration, charges, credit score, flexibility, and eligibility criteria before approving a loan application.

- Their importance lies in providing funds for significant expenses, stimulating economic growth, consolidating high-interest debts,

- supporting business competition, financing large projects and managing cash flow effectively.

Loan Products Explained

Loan products are accessible under a financial contract between a lender and borrower, where the former offers to provide money to loan seekers, with the latter guaranteeing the repayment of the principal amount along with the interest applicable within the loan duration. Loans are granted to only those with good credit scores and eligibility with respect to income level and credit history. Such loans help in meeting all consumer needs right from house purchase to financing education. Moreover, they serve as economic enablers as they address liquidity constraints over time.

When a borrower applies for a loan, they receive principal or lump sum and then repay it in equal monthly installments or as fixed by the bank until the loan term is over. The repayment schedule differs from product to product. Personal loans have a tenure of 1-5 years, while mortgage loans are often provided with a tenure of more than 10 years.

These products make funds accessible for purchases, business expansion or operations and empower governments to take up various social projects in partnership with companies. They also lead to the fostering of trust between lenders and borrowers. However, these loans could spiral out of control and create more debt if not managed well.

As such, these products of loans significantly affect the financial landscape by impacting investment behavior and consumer spending. These financial products form major revenue streams through interest for credit unions, non-banking financial institutions and banks. However, only responsible lending practices yield positive results, maintaining economic stability and financial inclusion and opening gates to underprivileged sections for easy access to monetary funding.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

There are five main types of loan products in the banking sector, which include the following:

#1 - Secured Loans

These options need collateral or security to safeguard the borrowed funds. This alternative is meant for situations where lenders need a guarantee for repayment. In case of non-payment, they use the property kept as collateral to recover the loan amount. Such options are further divided into:

- Home loans for construction or buying houses.

- Gold loans, where gold is used as collateral.

- Loans against property, which provide loans against real estate.

#2 - Unsecured Loans

These have no requirements for collateral, and lenders depend on creditworthiness to approve the loan application. Some of the categories these options are classified into are as follows:

- Personal loans are utilized for personal needs and expenses.

- Business loans help in conducting business operations or expanding the same.

- Education loans are applied for to finance higher education requirements.

#3 - Auto Loans

These are directed at buying vehicles, acting as collateral security itself. These are specific-purpose loans, which are utilized for what is taken. For example, an auto or car loan cannot be used to finance any other activity or property. It must be utilized for buying or maintaining a car. As an alternative to ownership-based financing, a car leasing business provides greater flexibility by allowing individuals to use vehicles without large upfront costs or long-term financial commitments.

#4 - Small Business Loans

These products are created to facilitate small enterprises with capital or operational expenses. These products offer everything from equipment to project financing per the customers’ requirements.

#5 - Credit Loans

Such loans are sanctioned to borrowers as revolving credit for spending within a fixed limit and then repaid over time with a higher interest rate.

Factors to Consider with Different Types of Loan Products

Multiple factors need consideration when an individual or entity has to choose which product would be the best for them to access. Let us have a look at a few of them below:

- Loan purpose: Knowing the requirement that makes an individual or business seek a loan from the bank helps choose the right product.

- Interest rates: This helps compare various products, helping borrowers select the best loans with lower interest per their needs and capacity.

- Loan duration: People and businesses also consider the duration of loan terms to check on the repayment requirements. While the long-term means more interest, short-term loans are available at low interest rates.

- Additional charges: One must minutely study these charges to learn about the overall effect of these on any loan. This, in turn, helps one make better loan-taking decisions with respect to the whole amount they would be liable to pay against the loan.

- Credit scores: Applicants' credit scores are checked thoroughly to allow loans to borrowers having a higher credit score.

- Flexibility: The next factor is how flexible the repayment terms are. Suppose one can repay the loan earlier than the fixed term. In that case, it helps manage loans effectively as the borrowers can decide on repaying the amount per their current financial situation.

- Eligibility criteria: These criteria include the assessment of borrowers’ profiles in terms of their income levels, creditworthiness and employment history. Hence, they must apply for the loans only if they fulfill these criteria and meet the lenders' standards.

Examples

Let us take the help of a few examples to understand the topic.

Example #1

An online article published on November 22, 2024, discusses the introduction of tailored vehicle loans by the State Bank of India (SBI) for Uber fleet partners. The new initiative tries to offer hassle-free loan disbursement, including low-cost and customized financing solutions to support the industry's growth. Such a strategic partnership between the brands will benefit from extensive financial services networks and Uber’s technology, which would facilitate the fleet partners to widen their presence and operations impactfully. The report added that the collaboration aligns with Uber’s vision of boosting the Indian ride-sharing ecosystem as a significant contributor.

Example #2

Let us assume that a financial institution called BrightLand Bank is located in Old York City and provides different loan products customized to its customers’ needs. Alex, a young businessman, seeks a business loan of $50,000 to widen his coffee chain. Hence, he applied for a loan at BrightLand, which sanctions the loan at an 8% yearly rate of interest repayable over seven years.

On the contrary, Remily, a housewife, also applies and obtains a mortgage loan of $200,000 at a 5% fixed rate for her dream home. BrightLand bank distributes personally tailored finance to both individuals at a 13% rate. They approve both their applications based on their credit scores and repayment history.

This shows how the banks offer different loan products, both business/commercial and personal loans, at different rates and conditions.

Importance

Let us check how these loan products are important for entities and individuals:

- They help businesses and individuals access finances for major expenditures, such as managing emergencies, expanding businesses and purchasing real estate for household or commercial use.

- They increase the overall liquidity in the market to support competing businesses simultaneously, stimulating the economy during the process.

- Loans could consolidate debts with high interest and make payments with lower interest, enhancing financial stability.

- It ensures responsible lending as the borrower's loan purpose impacts lenders' decisions on setting proper interest rates and approving the loan.

- Loans are vital for meeting emergency funds for home improvement, medical emergencies, vehicle repairs and building long-term assets.

- They permit businesses to fund large investment projects and growth strategies while handling cash flow efficiently.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.