Part of our Financial Calculators guide

What Is A Loan Comparison Calculator?

Loan Comparison Calculator is a tool that can compare the installments paid periodically and further the total interest outgo on loan. Then a decision can be taken as to which loan terms and conditions should be opted for. Interested borrowers can compare up to three loan options collectively and find out which one would be more convenient to pay back.

Loan comparison calculator is designed based on equations that would help users obtain monthly payment and interest amount that they would require paying at regular intervals if they take up a loan. In the process, they can check more than one loan option for the repayment figures, and accordingly decide on their lenders.

Loan Comparison Calculator Explained

A loan comparison calculator can compare loans across tenure, banks, and interest rates, whichever meets the borrower’s requirement. Accordingly, the borrower will take a loan, whether it be less interest outflow, extended or lower installment, etc.

When using this calculator, the interested borrowers need to enter required details so that it calculates the monthly payment and provide an answer to users along with other details. One can put these details one by one for more than one loan options, and then compare the repayments to be made. Based on whatever feels convenient, they may choose one.

Most websites allow users to compare three to four loan options simultaneously. The monthly payment and the interest to be paid has a great impact on the budget one prepares to deal with all other expenses. Hence, knowing the expected amount helps have a budget-friendly repayment schedule.

As soon as the loan amount, the loan term, and the interest rate applicable are all entered, the calculator instantly computes the principal and interest amounts to be repaid to lenders. In hsort, these calculators help users learn about all the costs they will have to bear once they apply and take up a loan, be it personal, commercial, auto, mortgage or student loan.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Formula

The formula for calculation of Loan Comparison is below for a minimum of two loans, and further, if there are more than the same formula can be used:

Loan I Computation

[P * R * (1+R)N]/[(1+R)N-1]

Loan II Computation

[P * R’ * (1+R’)N’]/[(1+R’)N’-1]

Now both loans will be compared,

Wherein,

- P is the loan amount

- R is the rate of interest per annum

- N is the number of periods or frequency wherein the loan amount is to be paid

- R’ is the rate of interest per annum for the second loan

- N’ is the number of periods or frequency wherein the loan amount is to be paid for the second loan

The Loan Comparison Calculator can be used to compare loans across different interest rates and different tenures or even across a different financial institution, which shall aid the borrower to make a decision which shall be fruitful for him, for example, easy installments, lesser cash outflow in the form of interest, or extended installments, etc. as per his requirements.

Loans must be planned; otherwise, one would pay a higher interest rate, and even the installment amount would be huge. Therefore, comparing loans across is essential and then making a decision.

How To Calculate Using Loan Comparison Calculator?

One needs to follow the below steps in order to calculate the monthly installment amounts.

- First of all, determine the loan amount which needs to be borrowed. Banks usually provide more loan amounts to those with a good credit score and less to those with a lower credit score. First, we shall enter the principal amount:

- Multiply the principal by a rate of interest for Loan I.

- Now, we need to compound the same by rate until the loan period for Loan I.

- We now need to discount the above result obtained in step 3 by the following:

- After entering the above formula in excel, we shall obtain installments periodically for Loan I.

- Repeat the same steps from 2 to 4 for Loan II if there are multiple loans.

- Now, one can compare the interest outflow and thus then can make decisions accordingly if it’s solely based on interest outflow.

Examples

Let us consider the following instances to understand the concept better along with checking how the calculation is done:

Example #1

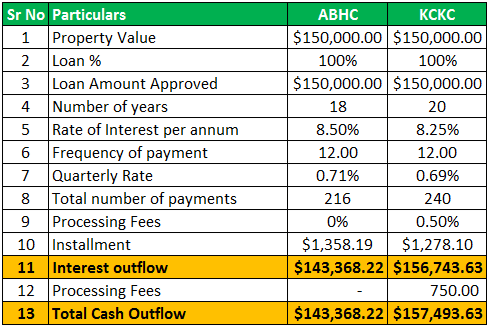

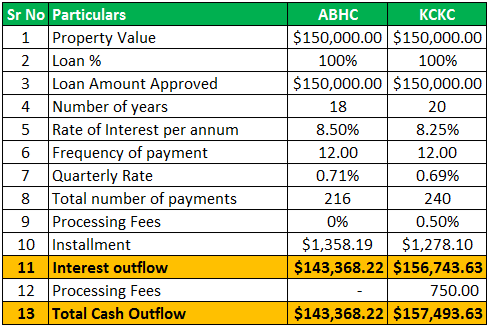

Mr. A is working in a multinational company and is now looking to borrow money to purchase a house. He is currently perplexed about which bank he should borrow the money from. He has two options in hand; one is offered by ABHC bank, which is quoting him an 8.5% fixed rate of interest and the loan period will be 18 years, and another bank, KCKC bank, is charging an 8.25% fixed rate of interest and loan period will be 20 years and also the second bank would charge processing fee at the rate of 0.50% and has to be paid upfront whereas ABHC is charging no processing fees. Both banks are giving facilities to pay installments monthly.

You must compare the loans and advise where the loan should be taken from, provided he needs to borrow $150,000.

Solution:

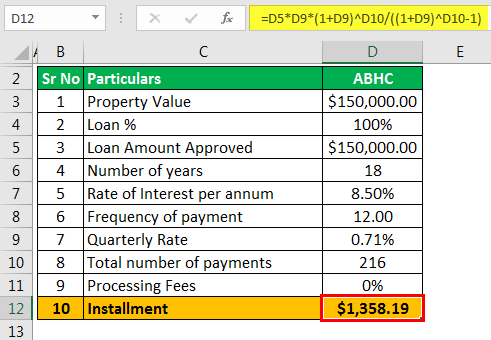

We need to calculate the Installment amount; the loan amount is $150,000.

LOAN I

The number of periods it is required to be paid is 18 years. Still, since here Mr. A is going to pay monthly hence the number of payments that he shall be required to be paid is 18*12, which is 216 equally installments, and lastly, the rate of interest is 8.50% fixed, which shall be calculated monthly which is 8.50%/12 which is 0.71%.

Now we shall use the below formula to calculate the EMI amount.

Monthly Installment = [P * R * (1+R)N]/[(1+R)N-1]

- = [150,000 * 0.71% * (1 + 0.71%)^216 ] / [ (1 + 0.71%)^216 – 1 ]

- = $1,358.19

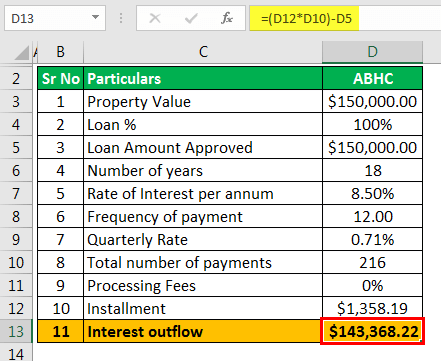

Interest Flow

Interest outflow can be calculated by multiplying the installment amount by several periods and subtracting it from the loan amount.

- = $ 1358.19 * 216- $150,000.00

- =$143,368.22

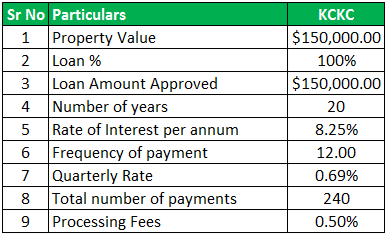

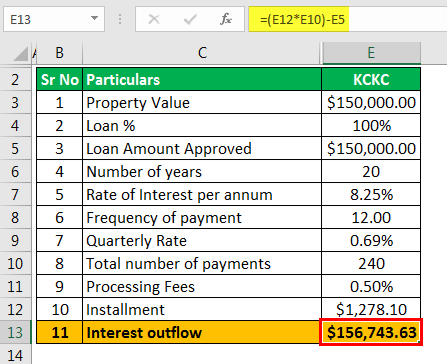

LOAN II

The number of periods it is required to be paid is 20 years. Still, since here Mr. A is going to pay monthly hence the number of payments that he shall be required to be paid is 20*12, which is 240 equally installments, and lastly, the rate of interest is 8.25% fixed, which shall be calculated monthly which is 8.25%/12 which is 0.69%.

Now we shall use the below formula to calculate the EMI amount.

Monthly Installment = [P * R’ * (1+R’)N’]/[(1+R’)N’-1]

- =[150,000 * 0.69% * (1 + 0.69%)^240 ] / [ (1 + 0.69%)^240 – 1 ]

- = $1,278.10

Interest Flow

- = $1278.10 * 240 – $ 150000.00

- = $ 156743.63

Now we can compare both the loans and figure out where the interest flow is more.

Even though at first instance, KCKC offers a lower rate, since it offers higher tenure, the borrower will end up paying more interest, and hence we have here only two options. Mr. A would prefer to take a loan from ABHC bank.

Example #2

There are two loan offers for a client per the below details:

| Particulars | Loan I | Loan II |

|---|---|---|

| Rate of Interest | 15% | 18% |

| Compound Frequency | Quarterly | Semi-annually |

| Tenure | 10 years | 8 years |

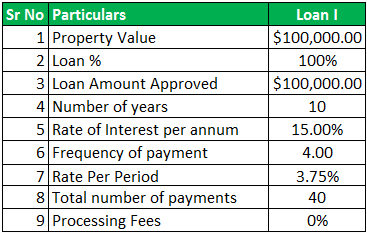

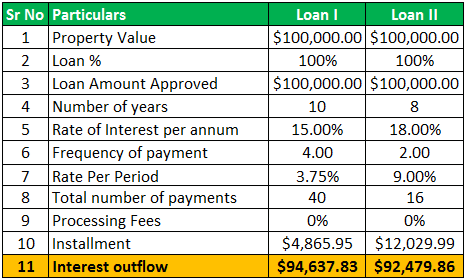

The loan amount is the same, which is $100,000. Based on the given information, you are required to compare the loans and advise the client as to which loan should be preferred, provided the client’s requirement is that the total cash outflow should be lower.

Solution:

We need to calculate the Installment amount; the loan amount is $100,000.

LOAN I

The number of periods it is required to be paid in 10 years, but since here, the borrower is going to pay quarterly; hence the number of payments that he shall be required to be paid is 10*4, which is 40 equal installments, and lastly, the rate of interest is 15.00% fixed which shall be calculated quarterly which is 15%/4 which is 3.75%.

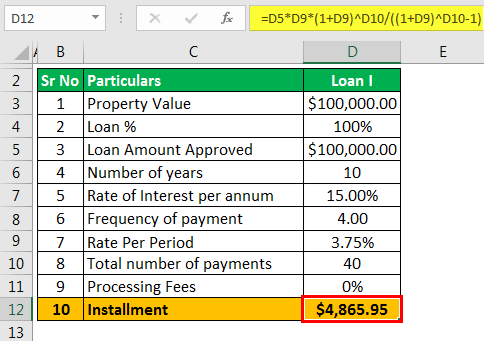

Now we shall use the below formula to calculate the EMI amount.

Monthly Installment = [P * R * (1+R)N]/[(1+R)N-1]

- = [100,000 * 3.75% * (1 + 3.75%)^40 ] / [ (1 + 3.75%)^40 – 1 ]

- = $4,865.95

Interest Flow

Interest outflow can be calculated by multiplying the installment amount by the number of periods and then subtracting it from the loan amount.

- = $4865.95 * 40 – $100000.00

- = $ 94637.83

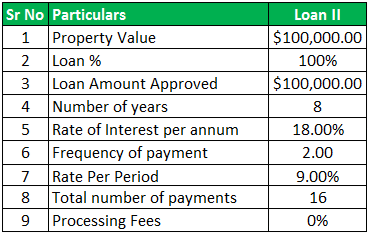

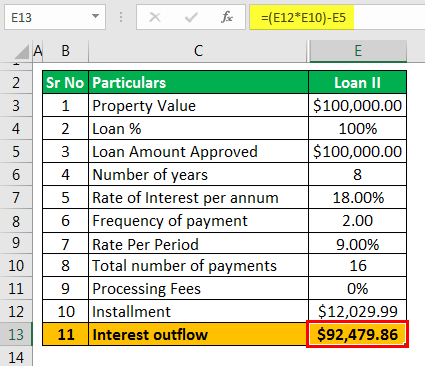

LOAN II

The number of periods it is required to be paid in eight years. Still, since the borrower is going to pay on a semi-annual basis, the number of payments that he shall be required to be paid is 8*2, which is 16 equal installments. Lastly, the interest rate is 18% fixed, which shall be calculated semi-annually at 18%/2, which is 9.00%.

Now we shall use the below formula to calculate the EMI amount.

Monthly Installment = [P * R’ * (1+R’)N’]/[(1+R’)N’-1]

- = [100,000 * 9.00% * (1 + 9.00%)^16 ] / [ (1 + 9.00%)^16 – 1 ]

- = $12,029.99

Interest Flow

- = $ 12029.99 * 16 – $100000.00

- = $ 92479.86

Now we can compare both the loans and figure out where the interest flow is more.

Hence, from above, it can be said that Loan II should be preferred even though the interest rate is high since the total cash outflow is less.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This has been a guide to what is Loan Comparison Calculator. Here, we explain the concept along with its formula, how to calculate using it, and examples. You may also take a look at the following useful articles –