Table Of Contents

What Is A Loan?

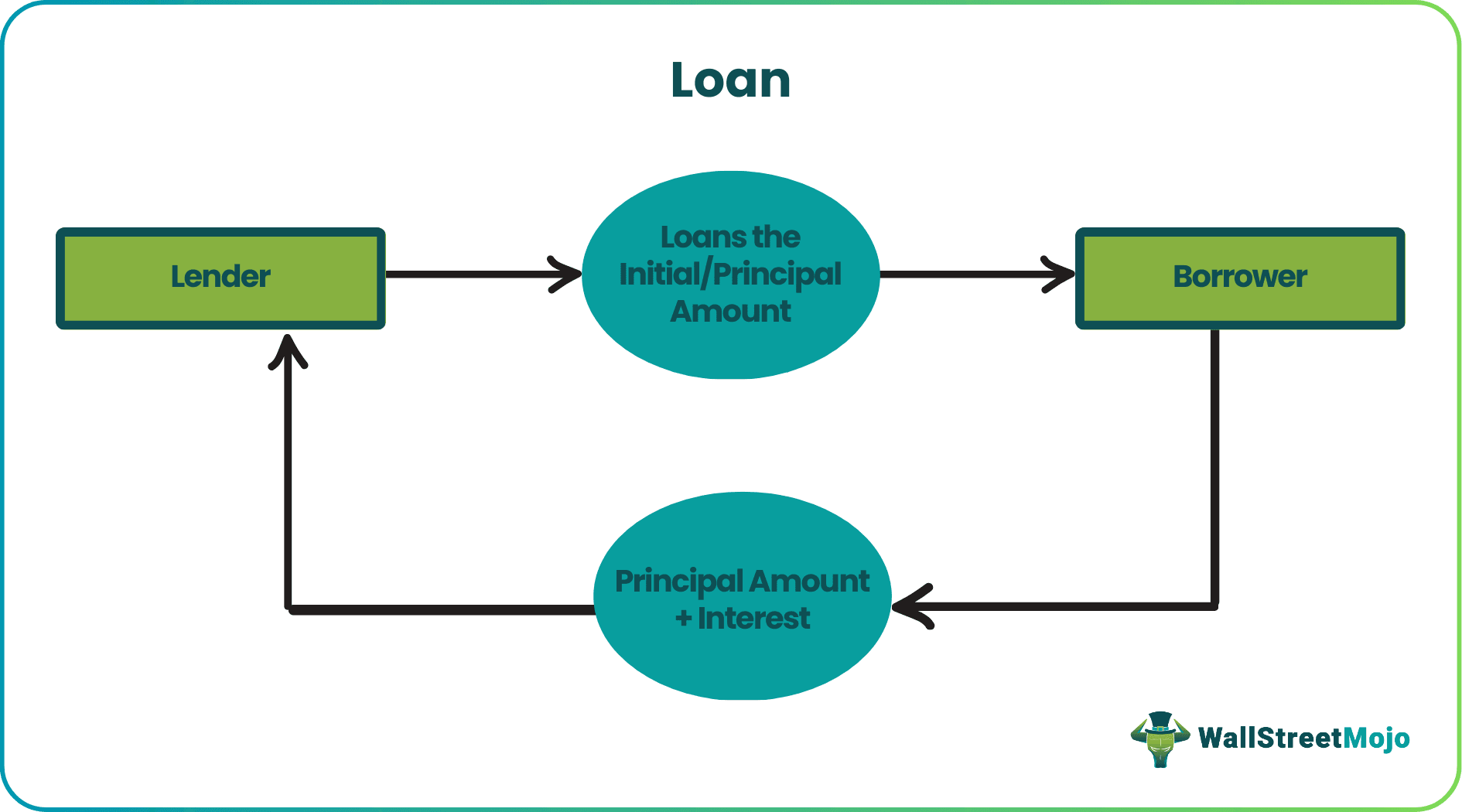

A loan is a vehicle for credit in which a lender will give a sum of money to a borrower or borrowing entity in exchange for future repayment. The borrower has to pay back the initial amount (principal balance) with an additional amount (interest), the rate of which varies in each case.

Sometimes, the borrower has to present collateral to gain the lender's trust. While loans provide essential financial assistance to the borrower for a certain time period, they act as an investment opportunity for the buyer to secure a future set of cash flows for a return.

- A loan is a sum of money a lending entity gives to a borrowing entity which it repays after a specific period, usually with an interest.

- They are a huge part of our financial markets and are availabe in many forms like a secured, unsecured, conventional, open-ended and close-ended loan, etc.

- Loans generate a future set of cash flows that result in return for the lender

- There are a few advantages and disadvantages of lending and borrowing loans.

How Does a Loan Work?

Loans can be given or taken by individuals, institutions, or governments. Typically, a borrower looking for capital (big or small, personal or for finance) seeks out a commercial lender or a family friend who can offer it. The lender will advance an amount of money to the borrower to agree to the lender's terms.

In addition to the loan amount, there will be a set of terms including any fees, interest, and the structure of interest. i.e, if the interest is paid a little each month, it is known as amortization. Or if it is paid before the principal balance is paid at the end, it is an interest-only loan).

The lending documents and contract will outline all terms before disbursing any money. Usually, though not always, lenders will have some type of asset as collateral for the money they are lending out. For homeowners, exploring the cheapest way to get equity out of the house, such as a home equity loan, is a common approach to accessing funds for major financial needs. This is to mitigate any risk that the borrower defaults and leaves the lender with no money and no way to get it back. Both the lender and the borrower must agree to all the terms.

Example

Here is an example:

Let's consider a real estate investment company trying to buy an apartment building for 100 million dollars. First, they would need to apply for a loan from a bank (or any other lending entity). Their application will include information about the business owners, the business itself, and the opportunity. Then, the lender will likely underwrite the deal themselves. They would go out to the property and assess its (and the company's) creditworthiness.

The lender will offer a loan for a certain percentage of the property (called the loan to value ratio). The interest rate on an apartment community is usually based on prevailing interest rates (LIBOR for now) plus a spread or return on top of the market interest rate. In this case, the loan will be for 200bps (basis points that are 1/100 of 1 percentage, so 2%) plus LIBOR. The LIBOR at the time of this writing is 0.13 but changes drastically based on economic factors.

So, in this case, the interest rate is currently 2.13%. Another fee the lender requires is an application fee of $1,000 and an origination fee of 1 point (a whole percent) of the lending amount. The lender has told the company that they will issue out a sum of $65,000,000, which would be a 65% LTV ratio, so the origination fee will be $650,000.

The final terms are that it is an IO loan, meaning the company pays the only interest during the hold and then the principal balance in totality at the end of the term. As real estate investors, the borrowers can simply pay off the money when they sell the asset at the end of the hold period. It frees up their capital so that they can either give it back to investors or invest it into a property to improve the asset during the hold period, which is a huge benefit to leverage.

Types of Loans

There are endless variations and structures to loans, just like there are for mergers and acquisitions. A few big types are secured, unsecured, conventional, open-ended, and close-ended.

Secured loan:

A secured loan often has collateral like in the case of a car loan (they can repossess the car if you do not make the payments).

Unsecured loan:

An unsecured loan has no recourse besides legal action for the lender to get their money back (this would be like consumer credit card debt where the lender does not have anything in return for the credit card in the wallet, and they cannot put a lien on the person's house to mitigate the risk of nonpayment).

Conventional loan:

A conventional loan is a common type of mortgage plan for homeowners that the government does not insure, subsidize or guarantee. Other lending types that assist homebuyers in the form of lower down payments, lower rates, or insurances would be FHA and VA loans.

Open-ended loans:

Open-ended loans do not have any prepayment penalties, whereas close-ended ones do. Typically one can pay back an open-ended loan early with no problem (such as getting a 30-year loan for the apartment building in the example above but selling the asset in 10 years).

Close-ended loans:

Close-ended loans will have a large fee, such as a percentage point or two if a person pays early or outside the agreed-upon time frame for payments.

Advantages

- One of the biggest advantages of loaning is leverage. Loans allow one to maximize the return one can get for the same amount of money.

- The money does not have to be repayable for the agreed duration of time

- A person can use the money for entrepreneurial purposes, and they do not have to share their profits with the lender

- It allows a borrower to pay back the debt with flexibility and does not have to face on-demand repayments

- There are many different types of borrowing options to choose from that may fit the borrower's specific needs

Disadvantages

- One has to pay back at a rate that stays steady while the value of the asset may drop dramatically. For example, during the Global Financial Crisis, the values of properties dropped dramatically. But people had to repay money based on an extremely inflated principal balance. This can lead to foreclosure and huge financial losses.

- The credit rating and availability of collateral affects the lender's decision to give money

- One would certainly have to pay more than they initially borrowed. For those in particularly distressed situations, the accrued interest grows into a huge sum.

Frequently Asked Questions (FAQs)

Loans are sums of money credited to a borrower who has to repay it in a specific period, usually with an additional amount called interest. Its types and interest rates can vary according to different situations.

It can affect a person's credit score if they are due to be paid for a long time. Similarly, the number of times they have borrowed money also affects their credit rating. This will make it harder for the person to obtain a new loan without paying back the existing ones. On the other hand, a prompt person who pays back the sum or interest regularly can improve their credit rating.

Income is strictly the money that a person earns. Since loans are not earned and are repayable, they are not classified as income. They, therefore are also not taxable.

Recommended Articles

This has been a guide to Loan & its definition. Learn how loans work, the types, advantages, and disadvantages along with an example. You can learn more about the form the following articles –