What Is Liquidity Ratio?

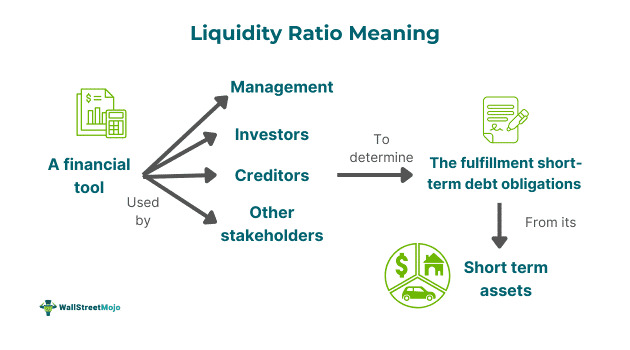

Liquidity ratio refers to a financial measure that gauges a company’s ability to meet its short-term financial obligations, such as creditors, from its available short-term assets without borrowing funds from external sources. The three major metrics for measuring liquidity are current, quick, and cash ratios.

Management, investors, creditors, and other stakeholders are often interested in determining a company’s liquidity position to analyze its creditworthiness and potential to fulfill its current debt commitments. Thus, liquidity ratios ascertain the financial health of the business in the short term, i.e., within 12 months.

Key Takeaways

- The liquidity ratios are the various financial tools used by the management, investors, creditors, lenders, and other stakeholders to determine the competency of a business entity in meeting its current financial commitments from its short-term assets.

- The various measures of liquidity include the current ratio, cash ratio, quick ratio, net working capital ratio, and basic defense ratio.

- These metrics are often used to determine the credit rating and creditworthiness of companies.

- While the standard liquidity ratios are always high, these ratios vary from business to business and industry to industry, and different accounting and reporting standards are used.

Liquidity Ratio Explained

The liquidity ratio refers to a set of financial metrics that helps analysts understand the capacity of a business entity to meet its short-term debt obligations from its short-term assets. The three measures to gauge the liquidity position of a company are the current ratio, quick ratio, and cash ratio. These tools help the creditors, investors, management, and other stakeholders to identify the credibility of the business and, at the same time, analyze its efficiency to meet its working capital requirements.

Some of the significant factors that shape the liquidity positions of the companies are:

- Company Size and Structure: While a small business entity may struggle to maintain its liquidity due to limited cash and high working capital needs, large firms may have strong liquidity due to established earning sources.

- Business Cycle: Firms at different stages of the business cycle have varying working capital requirements, which influence their ratios.

- Industry Standards: Every industry has different working capital needs and, therefore, has to maintain cash flows accordingly.

Types

The short-term financial potential of a firm can be analyzed through the following prominent metrics, each stated with the formula of liquidity ratios:

#1 – Quick Ratio or Acid Test Ratio:

The acid test ratio gauges the capacity of a firm to immediately pay off its current obligations from the readily available cash and equivalents. It is evaluated as follows:

Quick Ratio = Quick Assets / Current Liabilities

Where

Quick Assets = Current Assets – Inventory – Prepaid Expenses

Here, both inventory and prepaid expenses are excluded from the current assets. Since inventories cannot be quickly turned into cash, and prepaid expenses are already paid, they cannot be retrieved into cash. 1:1 forms a favorable acid test ratio, below which a business is assumed to face difficulty in settling its short-term liabilities from its cash and cash-like assets.

#2 – Current Ratio:

It is the most widely used liquidity metric, determining the ability of the business to settle its current financial obligations using its current assets. It also provides a sufficient margin of safety for the possible losses on immediate liquidation of these short-term assets.

The formula is:

Current Ratio = Current Assets / Current Liabilities

Where,

Current Assets = Cash-in-hand + Cash-at-Bank + Sundry Debtors + Receivables + Inventories + Disposable Investments + Loans and Advances + Advance Tax; and

Current Liabilities = Short-term Loans + Creditors + Bank Overdraft + Outstanding expenses + Cash Credit + Dividend Payable + Provision for Taxation

While an ideal ratio is assumed to be 2:1, it may vary from business to business and industry to industry.

#3 – Absolute Liquidity Ratio or Cash Ratio:

On the third number comes the cash ratio, which ascertains the total liquidity position of the company. Thus, it evaluates, if all the current liabilities become due at the present moment, then whether the firm will be able to pay all of it from its most liquid assets, including cash-in-hand, cash-at-bank, marketable securities, and other current investments. It is computed as:

Cash Ratio = (Cash-In-Hand + Cash-At-Bank + Marketable Securities + Current Investments)/Current Liabilities

An acceptable absolute liquidity ratio is between 0.5 and 1; however, in the real business scenario, companies may not have a significant cash reserve as required for an ideal cash ratio.

#4 – Net Working Capital Ratio:

The net working capital ratio is a critical metric to determine whether a business has sufficient availability of short-term assets to meet its short-term debts. It is determined as

Net Working Capital Ratio = Current Assets – Current Liabilities.

This ratio should always be positive; indeed, a higher NWC assures creditors that their bills will be paid off on time.

#5 – Basic Defense Ratio:

The basic defense ratio is a financial measure for gauging the time (in days) for which a firm can survive on its current assets to meet its various cash expenses and doesn’t need to seek external capital for this purpose. It is calculated as:

Basic Defense Ratio = (Cash + Receivables + Marketable Securities)/[(Operating expenses +Interest + Taxes)/365]

A higher basic defense ratio ensures a stronger liquidity position for the business.

Examples

The understanding of financial ratios is often complete with examples. Therefore, given below are some of the practical implications of such ratios in the real business scenario:

Example #1

Given below is the critical financial information extracted from the financial statements of ABC Pharmaceuticals for the year ending on December 31, 2024:

| Particulars | Amount (In $) |

| Cash-In-Hand | 10,700 |

| Cash-At-Bank | 19,200 |

| Accounts Receivables | 15,460 |

| Marketable Securities | 7,610 |

| Inventory | 42,190 |

| Current Investments | 4,585 |

| Prepaid Expenses | 290 |

| Other Current Assets | 2,215 |

| Total Current Assets | 1,02,250 |

| Accounts Payable | 13,670 |

| Outstanding Taxes | 2,145 |

| Outstanding Expenses | 7,990 |

| Deferred Revenue | 8,100 |

| Dividend Payable | 15,820 |

| Short-Term Loans | 2,105 |

| Other Outstanding Expenses | 450 |

| Total Current Liabilities | 50,280 |

If the operating expenses during the year were $20,750, $10,540, and $210, and $210 was paid in taxes and interest, respectively, to determine the company’s liquidity position.

Solution:

- Current Ratio = Current Assets/Current Liability = $1,02,250/$50,280 = 2.03

- Quick Ratio = (Current Assets – Inventory – Prepaid Expenses)/Current Liability = ($1,02,250 – 42,190 – $290) / $50,280 = 1.19

- Absolute liquidity ratio = (Cash-In-Hand + Cash-At-Bank + Marketable Securities + Current Investments)/Current Liabilities = ($10,700 + $19,200 + $7,610 + $2,215) / $50,280 = 0.79

- Net Working Capital Ratio = Current Assets – Current Liabilities = $1,02,250 – $50,280 = 51,970

- Basic Defense Interval = (Cash-In-Hand + Cash-At-Bank + Receivables + Marketable Securities)/[(Operating expenses +Interest + Taxes)/365] = ($10,700 + $19,200 + $15,460 + $7,610)/[($20,750 + $10,540 + $210)/365] = $52,970/($84,470/365) = 228.89

According to the above metrics, the company has maintained fairly good liquidity. It is even capable of meeting most of its current liabilities immediately, securing a cash ratio of 0.79. Further, a high NWC ratio shows that the firm will have sufficient cash left even if it pays off all its current liabilities. The basic defense interval indicates that the company can meet its cash expenses for almost 228 days without seeking any external funds.

Example #2

The S&P Global Ratings of US firms examined the overall liquidity scenario of these companies’ accounting liquidity ratios. It found that cash positions dropped for the first time in a year. The median cash and equivalents ratio of investment-grade firms fell to 21.48% of total liabilities from 22.6% in the previous quarter, thus elevating the concerns of paying off short-term debts. The debt costs of companies eventually surged with a historical rise in the benchmark interest rates set by the US Federal Reserve.

Also, the liquidity position of speculative-grade companies deteriorated, with a fall in the median cash ratio to 30.21% from 33.77% by the end of 2023. Despite this fall, the cash position for both investment-grade and speculative-grade firms remained higher than their recent lows. Notably, in the investment-grade category, there has been an improvement in cash ratios in 7 out of 11 sectors, such as finance, information technology, healthcare, consumer staples, real estate, energy, and utilities. Information technology increased by 6.70% points, while real estate rose by 5.31% points.

On the speculative-grade side, however, the real estate sector was the only one to improve in its liquidity position. The communications services and materials industries experienced the most significant drops in median cash ratios, with a nose dive of 12.64% and 6.89% points, respectively. The aggregate results broadly reflect the differing impacts of present economic conditions on different sectors and credit ratings as companies adapt to these high interest rates and economic uncertainties.

Advantages And Disadvantages

Advantages

- It helps to mirror the company’s short-term financial health.

- These values are easy to determine even for an individual with a non-mathematical background using the information available on the company’s financial statements.

- It is widely used to compare the efficiency of different companies in managing their working capital within the same industry or the change in a firm’s liquidity position over different accounting periods.

- It helps investors find a suitable investment prospect with a strong management team. It also helps creditors and other stakeholders identify a business entity’s creditworthiness.

- Further, such an analysis facilitates management’s improvement of the company’s liquidity and current financial position while optimally fulfilling its working capital requirements.

Disadvantages

- The absolute liquidity ratios are somewhat unrealistic in the real-world scenario since firms cannot maintain a high amount of cash for business operations.

- Due to human evaluation and analysis, such metrics can be used to manipulate the company’s actual financial position.

- The values of optimal ratios change from company to company and industry to industry. Firms using different accounting and reporting standards and policies can make it difficult to compare businesses’ liquidity positions.

- While emphasizing the current liquidity position, these metrics need to describe the company’s finances fully.

Liquidity Ratio vs Current Ratio vs Solvency Ratio

While the current ratio is a sub-category of the liquidity ratio, the solvency ratio is an entirely different type of financial metric used in ratio analysis. Let us now figure out the critical dissimilarities between the three:

| Basis | Liquidity Ratio | Current Ratio | Solvency Ratio |

| Definition | It is a group of short-term financial metrics that facilitate the analysis of a company’s efficiency in paying off its current financial commitments from its current assets without the need for any external funding. | It is a liquidity ratio that ascertains whether a firm is capable of meeting all its short-term obligations from its current assets within a year. | It is a type of financial measure that discovers a business’s ability to pay off all its long-term financial debts from its cash flows. |

| Purpose | Analyze the company’s short-term financial health while determining its credit rating and credibility. | Determine the company’s liquidity position within 12 months. | Gauge the firm’s long-term financial well-being by understanding its potential to meet long-term obligations. |

| Types | Current ratio, cash ratio, and quick ratio | Debt-to-equity ratio, equity ratio, debt-to-assets ratio, and interest coverage ratio. | |

| Components | Short-term assets and short-term obligations | Current assets and current liabilities | Various components of income statement and balance sheet |

| Outlook | Short-term | Short-term | Long-term |

| Used By | Management, creditors, equity investors, employees, and other stakeholders | Management, creditors, equity investors, employees, and other stakeholders | Management, bond investors, banks, and other lending institutions |

Frequently Asked Questions (FAQs)

How to improve liquidity ratio?

The liquidity ratio of a company can be increased over the period by:

- Improving the payment cycle;

- Converting the short-term debts into long-term loans;

- Reducing the operating expenses through negotiation and consideration of alternatives;

- Opting for a line of credit; and

- Disposing of unnecessary assets.

Is a higher or lower liquidity ratio better?

The higher the liquidity ratio, the better it is for a company’s creditworthiness and credit rating among the investors, creditors, and other stakeholders.

What is a good liquidity ratio for a bank?

A bank expects the firms to maintain a liquidity ratio of more than 2, while some may even consider a ratio above 1 given the other favorable metrics.

Can liquidity ratio be negative?

While a liquidity ratio cannot be negative, a ratio below 1 indicates that the business entity is incapable of fulfilling its working capital requirements, raising liquidity concerns.